Overview of banks and Internet banking systems

Habravchane, as the most technically savvy part of the world's population, undoubtedly loves to use modern technologies, in particular, Internet banking systems. Because it is convenient, it greatly saves time and money, it is a good step forward into the digital future, and it’s generally great to have complete control over your money from your computer. But not all banks and their Internet banking systems (hereinafter IB) are good, moreover, in my opinion, it is absolutely impossible to use many. In this article - an overview of some of the banks and IS systems popular in Russia, we will try to find out what is better and what is better not to use.

Will be considered: Raiffeisen, VTB24, Bank St. Petersburg, Bank Avangard, Promsvyazbank.

So let's go.

I actively used all these banks, some I continue now. All conclusions in the article are based on personal feelings and feedback from other users from the Internet, tried to remember everything, and write down as accurately and objectively as possible, but there may be mistakes and inaccuracies, so excuse me.

The factors that are interesting to me were taken into account, although I think most of the users, as well as ratings of banks and information security.

')

A few words about ratings. There are official ratings of banks, we will not consider them, because they are mainly based on data that is understandable only to specialists, and I am not a financier, but a simple user. And there is also a wonderful site banki.ru , on which are held: People's rating of banks and Rating of Internet banks . These ratings are compiled by the same simple users who need from the bank in general the same as me, and we will take them into account.

What the article does not have is information about contributions, since I do not use them.

A little about the benefits of information security - suddenly someone does not know. First, IB allows you to conveniently pay for most services. Personally, he completely saved me from going to Sberbank with queues and boors behind glass; from the use of payment terminals with their unscrupulous commissions, forever missing checks, slowly proceeding funds, and the inability to return the money if threw a check, and the payment did not come.

I regularly pay with the help of IB: landline phone, cell phones, Internet, rent, electricity, SIP, traffic police fines, taxes, and much less regular payments. I pay all this without commission, and it is very convenient - in order not to drive in the details of each new one, it’s enough to create a template in the IB once.

Secondly, it is convenient to look at the costs of statements.

Thirdly, it is safe. In order not to keep all the money on a card, from which, as you know, they can easily be led away, you can throw it through the IB to your current account, and keep a small amount on the card to go shopping. Or, just before a major purchase from a laptop, right in front of the cash register, transfer the required amount to the card and pay immediately.

Well, there are many more minor amenities, such as a transparent and convenient repayment of the loan, assistance in maintaining home bookkeeping, etc.

Now the specifics of the banks.

Low positions in the rating - customers have a lot of claims against the bank.

pros

Developed network of offices and ATMs. In St. Petersburg, ATMs and branches are almost at every step, in terms of convenience, location and accessibility - definitely among the leaders.

Developed network of offices and ATMs. In St. Petersburg, ATMs and branches are almost at every step, in terms of convenience, location and accessibility - definitely among the leaders.

Good credit cards "My conditions" and "Mobile bonus" - return for purchases up to 5%.

The ability to instantly replenish Yandex.Money, albeit with a commission of 1.5%

Minuses

Big mess and bureaucracy in the bank. Feels very much.

Big mess and bureaucracy in the bank. Feels very much.

It is not recommended to deposit money through cash-in ATMs. VTB24 saves on them, and quite often there are complaints that the ATM bills the bills, but it isn’t credited to the account, and people wait for this money for many days before they figure it out and return it, and understand it before long. There have been cases that did not return. So, if you make money - only through the cashier.

There are many offices, but they almost always have a sea of people, you have to wait for your turn, just like in Sberbank.

Service is not up to par - a little better than sber. Incompetent and unwelcoming employees are not uncommon.

Calling is not easy - you have to wait a long time.

IB Telebank

Telebank is probably the most functional and clever of all information security.

SMS informing costs from 100 to 300 rubles per year, depending on the number of SMS.

Security is provided through variable code maps.

pros

Good, user-friendly interface. The design was made by the studio of Artemy Lebedev, I like it, quite comfortable, but it will seem to many too heaped up and overloaded. It works fast.

Quite a large selection of service providers for payment.

You can create regular and deferred payments.

Transfers within the account and within the bank are instant.

You can set up notifications about any actions in the IB by email.

There are regular payments

Another telebank has two unique features:

1. Multicard, i.e. one card is tied to 3 accounts, ruble, dollar and euro - in theory it’s very convenient, you don’t need to make 3 cards for each account, one is enough - if a transaction is in rubles - it is withdrawn from a ruble account, if in dollars - from a dollar account. True, I heard that in reality it does not work as it should, and there are problems with choosing the right currency, unfortunately I don’t remember the details.

2. The ability to link a card of a third-party bank and transfer money from it to an account with VTB24 online. For this take 0.5%. This binding opens up a lot of opportunities. For example, you can instantly replenish your account with VTB24. Or some people cash out credit cards this way, falling into the grace period and do not pay interest (not all banks allow it). And with the help of this binding with a minimum of effort you can earn a lot of money from the air, but this is a topic for a separate article.

Minuses

Recently, VTB24 made an absurd thing in terms of security - they allowed only numbers to be used as a password. They also have login numbers, it is not hard to guess how quickly such a combination of login-password can be hacked. True then thought better of it, and introduced additional. security level - now you can log in only by entering the code from the card. It may have become safer, but I personally find it inconvenient to scrape this card every time just to see the bill or statement, it is very inconvenient. Insanity in general is.

Abon. Telebank system fee - 300r. in year. All other banks reviewed here are free of charge.

VTB24 is probably the only bank in the country that charges for transfers within the bank made through Telebank - 0.1% of the amount (min. 5 rubles, max. 1,500 rubles). In my opinion, this is treachery. External transfers are also not the cheapest - 0.3% of the amount (min. 15 rubles, max. 1500 rubles).

The system is damp, server errors often pour in, and at the most usual operations, or even do not allow to log in.

The statements are not sufficiently informative.

Overall impression

VTB24 is not the best choice, but if you mostly use cash withdrawals at an ATM, or the unique capabilities of a telebank, it will do.

Let's start with the cons

The most common misconception about Russian Raiffeisen is that it is an Austrian bank. Maybe among the shareholders and there is an Austrian riff, and the name converges, and appearance, but in fact there is little in common. Here, for example, if you withdraw cash from a Raiffeisen card at a riff ATM abroad, a commission will be charged, as if withdrawing from another bank. For example, Unicredit or Citibank does not charge a fee for withdrawing from its ATMs in any country in the world.

Riff rating is extremely low. The main complaints are the increased difficulty of getting your money back in case of problems. If any problem occurs, then it will be solved for a long time, if the maximum period for solving the problem is determined, then often it is solved only at the end of this period. I did not manage to pay a mobile phone a couple of times - the status “Error of operation” hung in the IB. 1000r was written off from the account, but was not received on the phone. They returned both times on the very last day of the maximum consideration period (45 or 60 days). And if the transfer for a large amount is frozen, I have to sit for 2 months without this money.

And if God forbid you have stolen money from a card, from an ATM, in a store or online store, judging by the reviews, it will be very, very difficult to return from a riff, to make chargeback. There were cases when the stolen money was returned only through the courts. And because of the bad security system of the riff (about it below), it is easy to steal money from the account.

Separately, it is necessary to say about the dial to the support service. This is just a song. If a card was stolen from you and you need to block it urgently, or some simplest question, then almost always it will look like this: Call - music plays for a long time, advertising goes, finally girl 1 picks up the phone - “Hello, can I help you?” You tell your problem for a long time, she listens attentively, does not interrupt, and then it turns out that the whole function of this girl is to switch clients between cities. Finding out where you're from, switches. Further, even longer waiting - the girl number 2 picks up the phone, again you tell everything from and to, again it does not interrupt, but it turns out that the function of this girl is just to switch between departments, your story is not interesting to her again. Switches to 3rd employee. It’s quite indecent to have a long wait, and someone already a little capable picks up the phone. It was never possible for me to get through a trivial issue in less than 15 minutes, and during that time you can take a lot of things with a stolen card.

pros

A large network of branches and ATMs in St. Petersburg, beautiful offices

Polite staff, no queues

Many good quality cash machines with cash-in. Such a number of cash-ins in St. Petersburg probably no one else has - they stand in every Okay supermarket, in every office and almost all of the clock.

At an ATM, you can change the currency, or throw dollars into a ruble card, which will immediately be converted into rubles. True, the course is bad, in connection it is different and better. But in the connection will be converted to day 2.

The ability to replenish Yandex.Money without commission, though not instantly, 1-2 days

Support 3D-secure technology.

IB Raiffeisen connect

The most common misconception about Raiffeisen connect is that it is an internet banking system :)

Big minus - stagnation. Of course, via a connection, you can make transactions, transfers, pay for the phone, look at the statement, but as it is called by the people, this is a remote interface to the accountant, and not a full-fledged information security. Only payment for services is immediately carried out, the transaction operator does everything manually during business hours, and you can only submit an application through a connection. This is terribly uncomfortable. For example, it is necessary to exchange rubles for euros. You go in a connection, you order an exchange. If ordered in the evening, only tomorrow rubles will be withdrawn from the ruble account, and only the day after tomorrow they will come to the euro account. And if today is Friday at 17:00, the money will come only on Tuesday. The same for all other operations. The minimum credit card payment must also be made a few days before the deadline, otherwise you take off from the grace period and end up with interest. I would not be surprised if the blocking of the card from the IB does not happen immediately either.

External payment can easily go 2-3 days.

It is impossible to transfer money from the card account to the current one, and it is also impossible to forbid the card to be banned. It turns out that if there is money on the account, then all of them can be withdrawn, or you can pay for the purchase, including on the Internet. This is a big security breach. Usually, a large amount is stored on the current account, or deposit, and on the card they keep a small amount, necessary for everyday expenses, and periodically replenish it through IB.

The set of service providers is very meager.

Security is weak. All operations are protected only by EDS, there are no cards with codes, i.e. it is enough to settle for an intelligent trojan, and you can withdraw all the money from the account.

Horse tariffs.

SMS informing - unscrupulous 720p per year, and there is little sense from it - text messages often come with a delay of 2, 5, 10, 60 minutes, but they may not come at all.

Ruble transfer to an external bank: 1.5% min. 50 rubles max. 1500 rubles, and it seems to me that quite recently there was at least 150 rubles.

For issuing cash in their cash desks, the bank also takes a commission.

The exchange rate is not the best.

When paying with a ruble Visa card abroad - 2% of the amount is removed and converted at the best exchange rate. Mastercard is cheaper, but still unprofitable because of the course, and some hidden commissions are being made, I could not find out which ones.

Extract extremely non-informative. For example, it is not visible even from whom the transfer came, only the purpose of the payment is visible.

You cannot remotely open a contribution.

pros

Nice interface

The ability to import statements in CSV, QIF

The presence of the feedback form, though instead of making a full-fledged ticket system via the SSL channel, this form simply sends a request, and the answer comes to an unsafe email. And not earlier than in a day, even on trivial matters.

Weak security has one plus: convenience - no need to scrub the code for payments, everything is done in a few mouse clicks.

The general impression is that you can only use it if cash-in ATMs are often needed, instant operations are not needed, and it’s not scary that a computer is hacked and money stolen. But it is better to choose another bank.

In short: in my opinion - this is the best choice. It occupies the second place in the national rating, although most recently it has been at the first for a long time. Now on the first some little-known bank.

Avant-garde is of medium size, somewhere in the 50th place in the rating of the largest banks in Russia. As a result, it is devoid of many of the problems inherent in fat banks - bureaucracy, sluggishness, inattention to the client. And endowed with many advantages, such as a real working individual approach to the client, the ability to directly contact the high management and get a qualified answer to your problem, a quick support service, etc.

Offices in the classical sense at the Avant-garde is not enough. Instead, they are something like a cash register and a rack with one operator somewhere in the supermarket. But for me personally, this was not a problem, because I never saw any queues, and the staff is very competent and works quickly. And in general, it is better this way than in the crowded beautiful VTB24 office with incompetent employees.

pros

Best phone support I've ever seen. No music, no expectations, no switching between specialists. All my calls were like this: 2 beeps, the specialist picks up the phone and quickly and efficiently answers all my questions. The level of training of employees of TP is imho on the head of most other banks. The truth should be noted that I called not often.

Giant plus bank for the fact that he has long and regularly communicates with users on the forum of a third-party site. It looks like this: a forum has been created on the forum, in which 2 high-ranking bank employees are constantly present and provide qualified answers. You can for example find out the news before the official announcement from the first mouth. Or speed up the solution of a non-standard question. Well-established and open dialogue with the client is very convenient and modern.

No less a big plus for the bank for the tariff policy. Visa electron card is free of charge, Visa classic and Mastercard are free if there is a relatively small turnover (84000 rubles per year), IB is free, external ruble transfers are 10p per transfer, SMS notification is free. Such is communism.

The presence of almost unique services - non-express express cards. It looks like this: for example, it took urgently to get a card, and there is no time to wait 5-7 business days until it is made, or to pay 3000 for an emergency to some banks (and an emergency issue is 1 working day, or at least a few hours ), you can go to the avant-garde. In 5 minutes, they will open an account there, make an access to the information security, give a flash drive with certificates, and cards with variable codes, and immediately issue an electronically valuable non-named visa for which you can even pay online. It's all free.

SMS informing works flawlessly - the check has not yet come out, and SMS has already arrived. I did not see delays even once, even abroad.

Paying with a ruble card abroad is not as profitable as in the PSB, but enough so as not to sweat about it. Removed at the rate of the bank + 0.75%. And in the statement everything is absolutely transparently visible, all courses, all commissions.

Avant-garde is the only bank represented here that issues chip cards. In countries such as Germany, England, paying with a chipless card is a real problem, they are not accepted almost anywhere. Moreover, chip cards are safer and it is much easier for the client to challenge transactions with them than with magnetic ones. In general, the future of chip cards.

The lack of ATMs is compensated by a certain number of round-the-clock cash desks. Receiving cash in them without a commission, by pin-code or passport.

Contribution and cash withdrawal without commissions in operating cash desks and branches. And you can get money from an account to which the card is not issued, also without commissions. It is useful if you need, for example, to buy euros at a good exchange rate - he contributed rubles, exchanged for euros in IB, took off.

Free statements of transactions with printing, account statements. For example, bailiffs take such information as proof of payment of the fine with a bang. In many banks this is a paid service, as far as I know.

Grace cards with a grace period of 200 days are a unique service.

There is a program “Bring a friend”, give buns for new customers on your recommendation. For example, for the 5 clients listed give a 16GB flash drive. (so if you liked the article, well in a personal)

Support 3D-secure technology.

Minuses

Few ATMs. True, I always pay with a card and I rarely take money off, and there is a 24-hour ticket desk in front of the house, so the minus is insignificant for me.

Who has thought of making variable code maps so thin - I don't know. They show through with a good flashlight so that all the hidden codes are visible, an unscrupulous bank employee or courier in theory can enlighten and rewrite them all. By the way, the PSB also shine through but not so much, while the VTB24 practically does not.

Due to the fact that the bank is not large, all sorts of monsters like Aeroflot do not want to cooperate with it with their bonus miles, i.e. no co-branded cards. This is a serious minus, which many (and me included) stops us from actively using avant-garde cards. But just a few days ago, some kind of cashback card is issued with good conditions, until I know the details, we will look.

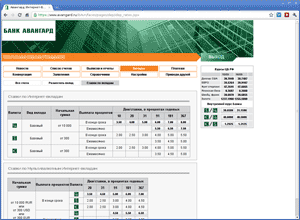

IB vanguard

The information security is on the 4th place in the rating, but the place is more due to the fact that until recently it didn’t work in Linux and Mac without a Vain EDS, it has already been fixed. Most negative reviews were due to this.

pros

The most informative IB. It is not distinguished by its beauty and modernity, but it is convenient to use, all the necessary information is where it should be.

The most adequate security system. At the entrance to the IB, only the login-password is checked, all transactions within the account (conversion, transfer from card to account, etc.) - to choose, EDS or code from the card, i.e. Do not want - do not scrape the code. All transactions on withdrawal of funds from the account (including mobile payment) - only through a code from the card. Thus, without a code from a card, it is impossible to steal money, but at the same time it does not cause inconvenience.

The most informative account statement. You can see literally everything. If the incoming payment - can be seen from whom the transfer, processing time accurate to a second. If the outgoing payment - you can see at what stage it is, whether it is stuck on the currency control, or left, how much it got under control, how much is executed, the name of the operator. If payment by card - you can see separately what amount was blocked and what was withdrawn, time to seconds If a currency transaction on the card shows how much it was charged in the currency, at what rate. If there was a double conversion, everything is also visible. And everything coincides with the official rates up to a penny, which is not true, for example, about Raiffeisen or Promsvyazbank.

The exchange rate is good.

It develops quite quickly, new features are being introduced, the wishes of users are taken into account.

You can open a deposit through IB

Large selection of service providers

Instant transfers within the account, within the bank, conversion.

External transfers fly very fast. In 9 ordered, in 11 already arrived.

There is an iphone version

Payment templates can be signed by EDS, and without removing the signature you can not change them. This ensures that if your password is stolen, without EDS they will not be able to quietly change the pattern.

— , .. . 20000, 5000 10000. 5000 , 5000 , .

. , , CVV , — . , .

Minuses

( )

, . , , .. .

,

, , (PSB-retail) 1- -.

pros

. ( + 0.6% ). . ( ) - , , . .

, , .

, , — , .

5.

. , , 1-2

Minuses

, , - - 1 , .

— , , , , .

, , .

PSB-retail

— 9 , 18 .

PSB-retail , , , , .

( - : 20). — .

.

.

— , . , , .

— , .

, ..

Minuses

, . , .

.

. , , . — .

.

.

— .

: , . . . - . , .

, . , .

pros

, . - - .

, .

— .

Minuses

— , , .

, .

.

— 360 .

, , .

.

. 9 , 11 .

.

.

— 0 , , .

.

.

, , -, 4 .

Minuses

, . .

, .

, , . , . — .

.

: , -, , , . — .

:

1.

2.

3. -

, , , , .

, , - , , , ..

Will be considered: Raiffeisen, VTB24, Bank St. Petersburg, Bank Avangard, Promsvyazbank.

So let's go.

I actively used all these banks, some I continue now. All conclusions in the article are based on personal feelings and feedback from other users from the Internet, tried to remember everything, and write down as accurately and objectively as possible, but there may be mistakes and inaccuracies, so excuse me.

The factors that are interesting to me were taken into account, although I think most of the users, as well as ratings of banks and information security.

')

A few words about ratings. There are official ratings of banks, we will not consider them, because they are mainly based on data that is understandable only to specialists, and I am not a financier, but a simple user. And there is also a wonderful site banki.ru , on which are held: People's rating of banks and Rating of Internet banks . These ratings are compiled by the same simple users who need from the bank in general the same as me, and we will take them into account.

What the article does not have is information about contributions, since I do not use them.

A little about the benefits of information security - suddenly someone does not know. First, IB allows you to conveniently pay for most services. Personally, he completely saved me from going to Sberbank with queues and boors behind glass; from the use of payment terminals with their unscrupulous commissions, forever missing checks, slowly proceeding funds, and the inability to return the money if threw a check, and the payment did not come.

I regularly pay with the help of IB: landline phone, cell phones, Internet, rent, electricity, SIP, traffic police fines, taxes, and much less regular payments. I pay all this without commission, and it is very convenient - in order not to drive in the details of each new one, it’s enough to create a template in the IB once.

Secondly, it is convenient to look at the costs of statements.

Thirdly, it is safe. In order not to keep all the money on a card, from which, as you know, they can easily be led away, you can throw it through the IB to your current account, and keep a small amount on the card to go shopping. Or, just before a major purchase from a laptop, right in front of the cash register, transfer the required amount to the card and pay immediately.

Well, there are many more minor amenities, such as a transparent and convenient repayment of the loan, assistance in maintaining home bookkeeping, etc.

Now the specifics of the banks.

VTB 24

Low positions in the rating - customers have a lot of claims against the bank.

pros

Developed network of offices and ATMs. In St. Petersburg, ATMs and branches are almost at every step, in terms of convenience, location and accessibility - definitely among the leaders. Good credit cards "My conditions" and "Mobile bonus" - return for purchases up to 5%. The ability to instantly replenish Yandex.Money, albeit with a commission of 1.5%Minuses

Big mess and bureaucracy in the bank. Feels very much. It is not recommended to deposit money through cash-in ATMs. VTB24 saves on them, and quite often there are complaints that the ATM bills the bills, but it isn’t credited to the account, and people wait for this money for many days before they figure it out and return it, and understand it before long. There have been cases that did not return. So, if you make money - only through the cashier. There are many offices, but they almost always have a sea of people, you have to wait for your turn, just like in Sberbank. Service is not up to par - a little better than sber. Incompetent and unwelcoming employees are not uncommon. Calling is not easy - you have to wait a long time.IB Telebank

Telebank is probably the most functional and clever of all information security.

SMS informing costs from 100 to 300 rubles per year, depending on the number of SMS.

Security is provided through variable code maps.

pros

Good, user-friendly interface. The design was made by the studio of Artemy Lebedev, I like it, quite comfortable, but it will seem to many too heaped up and overloaded. It works fast. Quite a large selection of service providers for payment. You can create regular and deferred payments. Transfers within the account and within the bank are instant. You can set up notifications about any actions in the IB by email. There are regular paymentsAnother telebank has two unique features:

1. Multicard, i.e. one card is tied to 3 accounts, ruble, dollar and euro - in theory it’s very convenient, you don’t need to make 3 cards for each account, one is enough - if a transaction is in rubles - it is withdrawn from a ruble account, if in dollars - from a dollar account. True, I heard that in reality it does not work as it should, and there are problems with choosing the right currency, unfortunately I don’t remember the details. 2. The ability to link a card of a third-party bank and transfer money from it to an account with VTB24 online. For this take 0.5%. This binding opens up a lot of opportunities. For example, you can instantly replenish your account with VTB24. Or some people cash out credit cards this way, falling into the grace period and do not pay interest (not all banks allow it). And with the help of this binding with a minimum of effort you can earn a lot of money from the air, but this is a topic for a separate article.Minuses

Recently, VTB24 made an absurd thing in terms of security - they allowed only numbers to be used as a password. They also have login numbers, it is not hard to guess how quickly such a combination of login-password can be hacked. True then thought better of it, and introduced additional. security level - now you can log in only by entering the code from the card. It may have become safer, but I personally find it inconvenient to scrape this card every time just to see the bill or statement, it is very inconvenient. Insanity in general is. Abon. Telebank system fee - 300r. in year. All other banks reviewed here are free of charge. VTB24 is probably the only bank in the country that charges for transfers within the bank made through Telebank - 0.1% of the amount (min. 5 rubles, max. 1,500 rubles). In my opinion, this is treachery. External transfers are also not the cheapest - 0.3% of the amount (min. 15 rubles, max. 1500 rubles). The system is damp, server errors often pour in, and at the most usual operations, or even do not allow to log in. The statements are not sufficiently informative.Overall impression

VTB24 is not the best choice, but if you mostly use cash withdrawals at an ATM, or the unique capabilities of a telebank, it will do.

Raiffeisen Bank

Let's start with the cons

The most common misconception about Russian Raiffeisen is that it is an Austrian bank. Maybe among the shareholders and there is an Austrian riff, and the name converges, and appearance, but in fact there is little in common. Here, for example, if you withdraw cash from a Raiffeisen card at a riff ATM abroad, a commission will be charged, as if withdrawing from another bank. For example, Unicredit or Citibank does not charge a fee for withdrawing from its ATMs in any country in the world. Riff rating is extremely low. The main complaints are the increased difficulty of getting your money back in case of problems. If any problem occurs, then it will be solved for a long time, if the maximum period for solving the problem is determined, then often it is solved only at the end of this period. I did not manage to pay a mobile phone a couple of times - the status “Error of operation” hung in the IB. 1000r was written off from the account, but was not received on the phone. They returned both times on the very last day of the maximum consideration period (45 or 60 days). And if the transfer for a large amount is frozen, I have to sit for 2 months without this money.And if God forbid you have stolen money from a card, from an ATM, in a store or online store, judging by the reviews, it will be very, very difficult to return from a riff, to make chargeback. There were cases when the stolen money was returned only through the courts. And because of the bad security system of the riff (about it below), it is easy to steal money from the account.

Separately, it is necessary to say about the dial to the support service. This is just a song. If a card was stolen from you and you need to block it urgently, or some simplest question, then almost always it will look like this: Call - music plays for a long time, advertising goes, finally girl 1 picks up the phone - “Hello, can I help you?” You tell your problem for a long time, she listens attentively, does not interrupt, and then it turns out that the whole function of this girl is to switch clients between cities. Finding out where you're from, switches. Further, even longer waiting - the girl number 2 picks up the phone, again you tell everything from and to, again it does not interrupt, but it turns out that the function of this girl is just to switch between departments, your story is not interesting to her again. Switches to 3rd employee. It’s quite indecent to have a long wait, and someone already a little capable picks up the phone. It was never possible for me to get through a trivial issue in less than 15 minutes, and during that time you can take a lot of things with a stolen card.pros

A large network of branches and ATMs in St. Petersburg, beautiful offices Polite staff, no queues Many good quality cash machines with cash-in. Such a number of cash-ins in St. Petersburg probably no one else has - they stand in every Okay supermarket, in every office and almost all of the clock. At an ATM, you can change the currency, or throw dollars into a ruble card, which will immediately be converted into rubles. True, the course is bad, in connection it is different and better. But in the connection will be converted to day 2. The ability to replenish Yandex.Money without commission, though not instantly, 1-2 days Support 3D-secure technology.IB Raiffeisen connect

The most common misconception about Raiffeisen connect is that it is an internet banking system :)

Big minus - stagnation. Of course, via a connection, you can make transactions, transfers, pay for the phone, look at the statement, but as it is called by the people, this is a remote interface to the accountant, and not a full-fledged information security. Only payment for services is immediately carried out, the transaction operator does everything manually during business hours, and you can only submit an application through a connection. This is terribly uncomfortable. For example, it is necessary to exchange rubles for euros. You go in a connection, you order an exchange. If ordered in the evening, only tomorrow rubles will be withdrawn from the ruble account, and only the day after tomorrow they will come to the euro account. And if today is Friday at 17:00, the money will come only on Tuesday. The same for all other operations. The minimum credit card payment must also be made a few days before the deadline, otherwise you take off from the grace period and end up with interest. I would not be surprised if the blocking of the card from the IB does not happen immediately either. External payment can easily go 2-3 days. It is impossible to transfer money from the card account to the current one, and it is also impossible to forbid the card to be banned. It turns out that if there is money on the account, then all of them can be withdrawn, or you can pay for the purchase, including on the Internet. This is a big security breach. Usually, a large amount is stored on the current account, or deposit, and on the card they keep a small amount, necessary for everyday expenses, and periodically replenish it through IB. The set of service providers is very meager. Security is weak. All operations are protected only by EDS, there are no cards with codes, i.e. it is enough to settle for an intelligent trojan, and you can withdraw all the money from the account. Horse tariffs.SMS informing - unscrupulous 720p per year, and there is little sense from it - text messages often come with a delay of 2, 5, 10, 60 minutes, but they may not come at all.

Ruble transfer to an external bank: 1.5% min. 50 rubles max. 1500 rubles, and it seems to me that quite recently there was at least 150 rubles. For issuing cash in their cash desks, the bank also takes a commission. The exchange rate is not the best. When paying with a ruble Visa card abroad - 2% of the amount is removed and converted at the best exchange rate. Mastercard is cheaper, but still unprofitable because of the course, and some hidden commissions are being made, I could not find out which ones. Extract extremely non-informative. For example, it is not visible even from whom the transfer came, only the purpose of the payment is visible. You cannot remotely open a contribution.pros

Nice interface The ability to import statements in CSV, QIF The presence of the feedback form, though instead of making a full-fledged ticket system via the SSL channel, this form simply sends a request, and the answer comes to an unsafe email. And not earlier than in a day, even on trivial matters. Weak security has one plus: convenience - no need to scrub the code for payments, everything is done in a few mouse clicks.The general impression is that you can only use it if cash-in ATMs are often needed, instant operations are not needed, and it’s not scary that a computer is hacked and money stolen. But it is better to choose another bank.

Bank Avangard

In short: in my opinion - this is the best choice. It occupies the second place in the national rating, although most recently it has been at the first for a long time. Now on the first some little-known bank.

Avant-garde is of medium size, somewhere in the 50th place in the rating of the largest banks in Russia. As a result, it is devoid of many of the problems inherent in fat banks - bureaucracy, sluggishness, inattention to the client. And endowed with many advantages, such as a real working individual approach to the client, the ability to directly contact the high management and get a qualified answer to your problem, a quick support service, etc.

Offices in the classical sense at the Avant-garde is not enough. Instead, they are something like a cash register and a rack with one operator somewhere in the supermarket. But for me personally, this was not a problem, because I never saw any queues, and the staff is very competent and works quickly. And in general, it is better this way than in the crowded beautiful VTB24 office with incompetent employees.

pros

Best phone support I've ever seen. No music, no expectations, no switching between specialists. All my calls were like this: 2 beeps, the specialist picks up the phone and quickly and efficiently answers all my questions. The level of training of employees of TP is imho on the head of most other banks. The truth should be noted that I called not often. Giant plus bank for the fact that he has long and regularly communicates with users on the forum of a third-party site. It looks like this: a forum has been created on the forum, in which 2 high-ranking bank employees are constantly present and provide qualified answers. You can for example find out the news before the official announcement from the first mouth. Or speed up the solution of a non-standard question. Well-established and open dialogue with the client is very convenient and modern. No less a big plus for the bank for the tariff policy. Visa electron card is free of charge, Visa classic and Mastercard are free if there is a relatively small turnover (84000 rubles per year), IB is free, external ruble transfers are 10p per transfer, SMS notification is free. Such is communism. The presence of almost unique services - non-express express cards. It looks like this: for example, it took urgently to get a card, and there is no time to wait 5-7 business days until it is made, or to pay 3000 for an emergency to some banks (and an emergency issue is 1 working day, or at least a few hours ), you can go to the avant-garde. In 5 minutes, they will open an account there, make an access to the information security, give a flash drive with certificates, and cards with variable codes, and immediately issue an electronically valuable non-named visa for which you can even pay online. It's all free. SMS informing works flawlessly - the check has not yet come out, and SMS has already arrived. I did not see delays even once, even abroad. Paying with a ruble card abroad is not as profitable as in the PSB, but enough so as not to sweat about it. Removed at the rate of the bank + 0.75%. And in the statement everything is absolutely transparently visible, all courses, all commissions. Avant-garde is the only bank represented here that issues chip cards. In countries such as Germany, England, paying with a chipless card is a real problem, they are not accepted almost anywhere. Moreover, chip cards are safer and it is much easier for the client to challenge transactions with them than with magnetic ones. In general, the future of chip cards. The lack of ATMs is compensated by a certain number of round-the-clock cash desks. Receiving cash in them without a commission, by pin-code or passport. Contribution and cash withdrawal without commissions in operating cash desks and branches. And you can get money from an account to which the card is not issued, also without commissions. It is useful if you need, for example, to buy euros at a good exchange rate - he contributed rubles, exchanged for euros in IB, took off. Free statements of transactions with printing, account statements. For example, bailiffs take such information as proof of payment of the fine with a bang. In many banks this is a paid service, as far as I know. Grace cards with a grace period of 200 days are a unique service. There is a program “Bring a friend”, give buns for new customers on your recommendation. For example, for the 5 clients listed give a 16GB flash drive. Support 3D-secure technology.Minuses

Few ATMs. True, I always pay with a card and I rarely take money off, and there is a 24-hour ticket desk in front of the house, so the minus is insignificant for me. Who has thought of making variable code maps so thin - I don't know. They show through with a good flashlight so that all the hidden codes are visible, an unscrupulous bank employee or courier in theory can enlighten and rewrite them all. By the way, the PSB also shine through but not so much, while the VTB24 practically does not. Due to the fact that the bank is not large, all sorts of monsters like Aeroflot do not want to cooperate with it with their bonus miles, i.e. no co-branded cards. This is a serious minus, which many (and me included) stops us from actively using avant-garde cards. But just a few days ago, some kind of cashback card is issued with good conditions, until I know the details, we will look.IB vanguard

The information security is on the 4th place in the rating, but the place is more due to the fact that until recently it didn’t work in Linux and Mac without a Vain EDS, it has already been fixed. Most negative reviews were due to this.

pros

The most informative IB. It is not distinguished by its beauty and modernity, but it is convenient to use, all the necessary information is where it should be. The most adequate security system. At the entrance to the IB, only the login-password is checked, all transactions within the account (conversion, transfer from card to account, etc.) - to choose, EDS or code from the card, i.e. Do not want - do not scrape the code. All transactions on withdrawal of funds from the account (including mobile payment) - only through a code from the card. Thus, without a code from a card, it is impossible to steal money, but at the same time it does not cause inconvenience. The most informative account statement. You can see literally everything. If the incoming payment - can be seen from whom the transfer, processing time accurate to a second. If the outgoing payment - you can see at what stage it is, whether it is stuck on the currency control, or left, how much it got under control, how much is executed, the name of the operator. If payment by card - you can see separately what amount was blocked and what was withdrawn, time to seconds If a currency transaction on the card shows how much it was charged in the currency, at what rate. If there was a double conversion, everything is also visible. And everything coincides with the official rates up to a penny, which is not true, for example, about Raiffeisen or Promsvyazbank. The exchange rate is good. It develops quite quickly, new features are being introduced, the wishes of users are taken into account. You can open a deposit through IB Large selection of service providers Instant transfers within the account, within the bank, conversion. External transfers fly very fast. In 9 ordered, in 11 already arrived. There is an iphone version Payment templates can be signed by EDS, and without removing the signature you can not change them. This ensures that if your password is stolen, without EDS they will not be able to quietly change the pattern. — , .. . 20000, 5000 10000. 5000 , 5000 , . . , , CVV , — . , .Minuses

( ) , . , , .. . ,, , (PSB-retail) 1- -.

pros

. ( + 0.6% ). . ( ) - , , . . , , . , , — , . 5. . , , 1-2Minuses

, , - - 1 , . — , , , , . , , .PSB-retail

— 9 , 18 .

PSB-retail , , , , . ( - : 20). — . . . — , . , , . — , . , ..Minuses

, . , . . . , , . — . . . — .: , . . . - . , .

-

, . , .

pros

, . - - . , . — .Minuses

— , , ., .

.

— 360 .

, , . . . 9 , 11 . . . — 0 , , . . . , , -, 4 .Minuses

, . . , . , , . , . — . .: , -, , , . — .

findings

:

1.

2.

3. -

, , , , .

, , - , , , ..

Source: https://habr.com/ru/post/98112/

All Articles