Destroy in 9 seconds. How an unknown algorithm destroyed IPO BATS

BATS Global Markets owns two electronic exchanges on which shares and options are traded. These exchanges operate on the principle of electronic communication networks (ECN).

BATS stands for Better Alternative Trading System, which means “Best Alternative Trading System”. The company is a platform that competes with other exchanges, primarily the NYSE and NASDAQ trading systems. The exchange platform BATS was launched in January 2006. At the moment it is the third largest stock exchange in the United States, its turnover is 12% of the total turnover of the country. Two years after its founding, BATS Global Markets became self-sufficient. About three hundred broker-dealer offices from different countries of the world are currently cooperating with this exchange. Over time, such giants as Bank of America, Merrill Lynch, Citi, Credit Suisse, Deutsche Bank and others have become co-owners of the company. The main difference of BATS from other sites is the creation of favorable conditions for trading: very low commissions compared to other exchanges. The BATS exchange platform is a kind of discounter for traders, such as the WalMart store in the USA. However, BATS ambitions are impressive. The exchange plans to create alternative listings and conduct an IPO.

From the very beginning of its founding, BATS was not focused on ordinary stock trading, but on providing services to large high-frequency traders, its electronic platforms were optimized for trading using robots. This choice is not surprising, since BATS founder Dave Cumings is the owner of Tradebot Systems, which accounts for about 5% of the daily turnover of the entire US stock market on certain days. BATS’s current first person, Joe Rutterman, also comes from this company.

May 6, 2010 from the US stock market for 20 minutes evaporated 862 billion dollars. The Dow Jones index hit a thousand points (the largest drop in history), trading was stopped, the financial life of the entire planet in the literal sense of the word was in limbo.

')

They found the culprit almost immediately: an enraged Commission on US Exchanges and Securities (SEC) jabbed a finger at HFT - computerized trading algorithms, which nowadays provide over 70% of the exchange turnover.

But after a “thorough investigation”, the anger changed to mercy: the lightning-fast depreciation of the stock market was officially blamed on the annoying mistake that the modest and unknown futures broker Waddell & Reed made in trading. The “crime” committed by W & R was the sale of 75,000 contracts for futures E-mini S & P. The volume, of course, is not the smallest, but even close is not sufficient to affect the market at least seriously, and all the more so to completely collapse it.

W & R initially vigorously denied any guilt, and then somehow pobmyak, popritih and dived back to where from where for a few moments a whimsical fate drew: into the crowd of other unknown and obscure stock market participants. The meticulous financial journalists for a long time after that were gossiping, trying to find out the size of the “compensation” that W & R received in exchange for agreeing to play the role of a general scapegoat.

As for the true culprit of the market collapse - HFT, then it was still a little patted on the sidelines of Congress and the Senate, intimidating with almost a legal ban, and also betrayed to public oblivion.

Why betrayed is clear: the main figures of high-frequency trading in America are Goldman Sachs, Morgan Stanley and a dozen of the largest banks - they provide 70% of the daily exchange turnover.

For almost two years no one remembered HFT, and the events of March 6, 2010 were preserved in collective memory as an annoying technical error or someone's mistake. And recently, on March 23, 2012, an event occurred that clearly demonstrated: “technical error” quietly evolved into a weapon of such destructive power that it seemed to be borrowed from the arsenals of the fantastic “Star Wars” of the future.

The event in question did not have a textural effect (lightning collapse of the market by a thousand points is a completely different calico!), Therefore only narrow professionals of the exchange trading noticed it. And in vain the public paid him so little attention! By far-reaching consequences and potential, the incident of March 23, 2012 is an order of magnitude better than the HFT pranks two years ago.

This is a failed attempt by the American company BATS Global Markets to hold an IPO. Attempts to bring the shares to the stock exchange continued exactly ... 9 seconds, during which the company's securities literally depreciated to almost zero, trading on them was suspended, and after some time, the company embarrassedly announced its complete refusal to go to the stock exchange in the foreseeable future.

The BATS IPO killed the computer hft algorithm launched from the terminals of an unidentified trader. when traders were able to start trading “from the street”, they saw on their monitors a quote of 4 cents as a starting deal - rather than $ 16–18, as the placement organizers had planned

The blame, like two years earlier, was officially laid on the “software failure”, but the accident of the SEC and all the structures involved in the drama was found to be a casual witness who not only recorded the incident down to a millisecond, but also analyzed each of the 567 exchange transactions made 9 seconds with BATS securities. From the analysis it appeared that there was no “software failure” at all, and the collapse of the IPO was the result of the work of a hidden malignant computer algorithm running from the terminals of an unidentified company that has direct access to the NASDAQ electronic exchange. The algorithm that purposefully carried out the clear task set for him: to destroy the IPO BATS!

I did not accidentally say that the potential of the incident is an order of magnitude greater than the HFT pranks of two years ago. In Fat Finger, I showed readers how high-frequency trading can cause total confusion on stock exchanges already due to the nature of their own trading algorithms. Thus, the collapse on May 6, 2010 was caused by a simple disconnection of several key HFT terminals, as a result of which the market lost the lion’s share of its usual liquidity and trivially fell into the abyss of the imbalance between supply and demand. At least it seemed so then.

The BATS IPO incident demonstrated that, in addition to passive “disconnecting”, HFT algorithms can still “turn on” and act at the right time and place in such a way that any security can be destroyed in seconds! In other words, technological monsters broke out of Pandora’s box and turned into a deadly weapon, perfect for future cyberwar!

Why did I suddenly start talking about cyber war? Who knows how many IPOs are held in America every year by unknown companies? One more, one less ... The fact of the matter is that BATS is not at all an ordinary business in itself, but what is there to be modest about! - the third largest stock exchange in the United States!

Surprised? Everyone knows about the NYSE, NASDAQ is on everyone’s lips, but BATS? What is BATS? Where did she come from? I think when readers get acquainted with the file of this company, they will be able to appreciate the exchange sabotage against the company on March 23.

Paradise for HFT

So, BATS Global Markets was established in 2005 by David Cummings in Kansas City, Missouri. BATS stands for Better Alternative Trading System ("Improved Alternative Trading System") - the name that speaks for itself. BATS is the so-called electronic communication network (ECN) of the second generation, that is, a platform for exchange trading, an alternative to the system NYSE and NASDAQ.

BATS created high-frequency trading players to meet their own needs, in particular for the qualitative reduction of commission fees, which, when interacting with the system exchanges and taking into account the enormous volume of transactions, are cast in very heavy amounts.

High-frequency traders not only create liquidity in the market, but also represent a favorite “cash” cow on exchange platforms, as they regularly provide them with high yields in the form of commission fees.

Creating BATS in 2005, traders set themselves an obvious task: to get out of control of the system exchanges and transfer operations to their own platform, more convenient for high-frequency trading. The main investors of BATS were Lehman Brothers, Getco, Wedbush, Lime and Deutsche Bank.

The names are all sonorous - what are only the late Leman brothers worth! - however, and the combined sad stigma: losers! Of course, in the context of the financial elite of the planet, it’s difficult to talk about failure in principle, but the lack of genuine favorites — companies that really determine global financial policy — is striking.

When BATS shares were listed on the stock exchange, Citibank, Credit Suisse, Morgan Stanley and JPMorgan joined the main underwriters, but even in the extended list the list lacks at least one name, which in itself completely outweighs the rest: Goldman Sachs.

This detail is a trifle, only information for thought, which, nevertheless, will help the reader to more objectively evaluate subsequent events.

The rate of high-frequency traders on the “separatist” was fully justified: on January 27, 2006, BATS opened to implement “high-speed, high-volume, anonymous algorithmic trading” and thanks to dumping commissions, in just a few months, pulled over 10% of America's total stock exchange volume (more than 50 million transactions daily )! More than 270 broker-dealer offices were traded on BATS, not only from the USA, but also from Europe and Asia.

Two years after the opening, BATS Global Markets, which had already managed three sites (two for shares and one for options), made a net profit.

The company's management model also crystallized: founding father David Cummings modestly resigned as CEO and chairman of the board, handing over the reins to his former executive director Joe Rutterman. And he headed the private investment firm Tradebot Systems, which developed shopping complexes and algorithms, and then transferred to licensed use of BATS.

The purely commercial success of the alternative exchange platform for high-frequency trading ultimately predetermined the decision of the founding fathers to make the company public. The highlight of the BATS IPO was that the underwriters decided to send the company’s shares to a large navigation through its own trading platform! Not through the traditional NYSE and NASDAQ, but through its BZX Exchange and BYX Exchange3.

The grounds for the decision were weighty. Firstly, BATS, in the event of a successful IPO, obtained full control over its own securities, at least avoiding hypothetical manipulations and dirty tricks from its direct competitors and fierce rivals - the NYSE and NASDAQ. Secondly, BATS securities were provided with the maximum possible liquidity, since, according to SEC statistics, trades on BZX are available for traders 99.94% of the total time, and BYX - 99.998%.

These figures are also indicative in the sense that the BATS sites have historically demonstrated exceptional reliability. In addition, before placing its shares on the stock exchange, the company conducted field tests and test simulations for six months. Everything went without a single bitch and hitch, at the highest technological level, which can only be expected from the latest generation trading platform.

High frequency shock

In the light of what was said on March 23, 2012, they look more improbable than the most unscientific fiction. Meanwhile, the fact remains that the placement of BATS papers began at 11 hours 14 minutes 18 seconds and ended at 11 hours 14 minutes 27 seconds. 9 seconds of trading - and a complete failure!

BATS GLOBAL MARKETS - AREA NOT A NEXT AMERICAN COMPANY, SOLVED TO GO TO IPO. THIS IS THE OPERATOR THIRD AT THE EXCHANGE OF THE EXCHANGE SITE OF THE USA (AFTER THE NYSE AND THE NASDAQ), WHICH HAS BEEN CLEARED TO TAKE 10% OF THE EXCHANGE VOLUME OF AMERICA FROM 2006,

Nanex (the most casual witness!), The largest supplier of ultra-accurate stock information in the USA, helped to reconstruct the dramatic events. Nanex tracks, captures, and then sells the entire chronography of America’s stock market life to traders to the nearest hundredth and thousandths of a second. The analysts of the company, within days after the incident, conducted their own investigation, which showed that there was no “software failure”!

It turned out that BATS shares destroyed 567 transactions that came in over 9 seconds from the same terminal, and not connected with the BATS exchange, but with the platform of its competitor, NASDAQ.

How it was? Let's start with a general chronology

So, on March 23, 2012, BATS, having received in advance all the necessary permissions from the SEC, decides to take its own shares to the exchange. The first tranche consisted of 6.3 million class A securities, of which almost half came from Lehman Brothers Holdings Inc. holdings. (the heiress who died in the Bose Lehman Brothers), and another 1.1 million from Getco.

Bidding was planned to start in the range between 16 and 18 dollars apiece, depending on the current level of demand at the time of opening.

When the placement started, the very first quote on the monitors - $ 15.25 - turned out to be lower than originally planned by 5%. As BATS managers later recalled, their price upset them, but not much. All hoped, if not for the rush demand, right off the bat, then at least for the interest recorded at the level of preliminary surveys, that is, in the range of 16-18 dollars .

According to the first transaction conducted at the site of BATS itself, the lion's share of the shares passed - 1 million 200 thousand shares. Further events developed as follows:

- in the first thousandths of a second, starting from the second, the quote rises to 15.75 - 800 shares are exchanged, which is already carried out on the NASDAQ;

- then in the range of a second, a chain of successive drops follows: $ 14 - $ 13 - $ 10.23 - $ 8.03 - $ 5.79 - $ 4.17 - $ 3.01. Some unfortunate seven orders, and the IPO is almost out of the game! Each of the killer transactions was made on a minimum lot of 100 shares - these are so-called flash orders of the IOC type (Immediate Or Cancel - “execute immediately or cancel”), which are the “firm” sign of the high-frequency trading algorithm. All transactions are conducted on NASDAQ;

- in the second second of life IPO BATS continued to fall: $ 2.17 - $ 1.15 - $ 0.76 - $ 0.0002 (two hundredths of one cent!). A total of 444 trades of $ 100 each were made, and all transactions were made on NASDAQ;

- there is a pause for a second, then at 11 hours 14 minutes 21 seconds a fixing trade of 3 cents per share of BATS passes;

- at 11 hours 14 minutes 27 seconds the price rises to 4 cents, and it is this figure that first appears as a starting transaction on the monitors of most computers from ordinary traders from the street (which, as you might guess, most);

- at 11 hours 14 minutes 33 seconds, the inscription “Halted” lights up on all the boards: the exchange breakers are turned on, which automatically stop trading on the stock if its quotation changes above the allowed limit. In the case of BATS drop from 16 dollars

- up to 4 cents in 9 seconds generally falls outside the scope of the possible;

- after a few minutes of pause, the BAT IPO price was returned on the quotation tape to a technically meaningless value of $ 15.25 per share. Senseless, since no sane trader would ever think to buy paper for such money if he knows that it cost 4 cents a few seconds ago!

- BATS management announces the withdrawal of IPO from the auction.

After a startling embarrassment, CEO and president of the company, Joe Rutterman, made a public appeal to investors, in which he apologized for the disaster and - sic! - put the blame on the “software glitch” (software glitch): “This is a terrible shame,” Joe Rutterman sobbed on the shoulder of the affected investors. - We feel terrible. All responsibility lies with our company. We take responsibility. There were no external influences from the side. ”

The last phrase looks very piquant, because if a stranger Nanex easily found the killer orders from NASDAQ terminals, BATS engineers could do it even faster by analyzing the internal traffic for transactions with shares of their own company. And definitely discovered. However, BATS chose not to exaggerate the scandal and even refused to re-conduct an IPO, fixing essentially a multi-million dollar loss for its shareholders and underwriters! Why was BATS so scared?

Fat fingerprints

Analyzing the transactions that destroyed the IPO BATS, Nanex discovered the mysterious "failures" that accompanied the work of the malignant computer killer algorithm. Moreover, these “failures” did not occur on the NASDAQ, but directly at the BATS sites, which, from the technological point of view, had a reputation as practically bullet-proof - “bulletproof”.

So, a quarter of an hour before the 9-second slaughter in the electronic networks of BATS, another strange glitch occurred, which brought down the quotes of Apple, the most actively traded paper on the US stock exchanges, as a result of which it was necessary to stop trading in all platforms of the country.Three days earlier, Apple's quotes on the same BATS also unexpectedly fell by $ 20, after which, again, the bidding stopped. Finally, a second before the withdrawal of BATS shares from trading, after the attack, the deal on Apple shares was $ 54 lower than the current quotes. And again, trading in securities of the pet was stopped for five minutes.

Apple’s choice as a collateral victim, in my opinion, is not accidental precisely because of the cult status of America’s favorite: as a result of the 9-second sabotage, not only BATS’s shares were discredited, but its ability to control the situation on its own site was also questioned. Who of the high-profile "high-frequency workers" will now want to trade on the stock exchange, which manages to roll the papers of Apple itself ?!

An analysis of the malignant algorithm shows that there was some kind of almost direct connection and dependence between trading Apple and BATS, but Nanex did not dare to take responsibility for such an assertion.

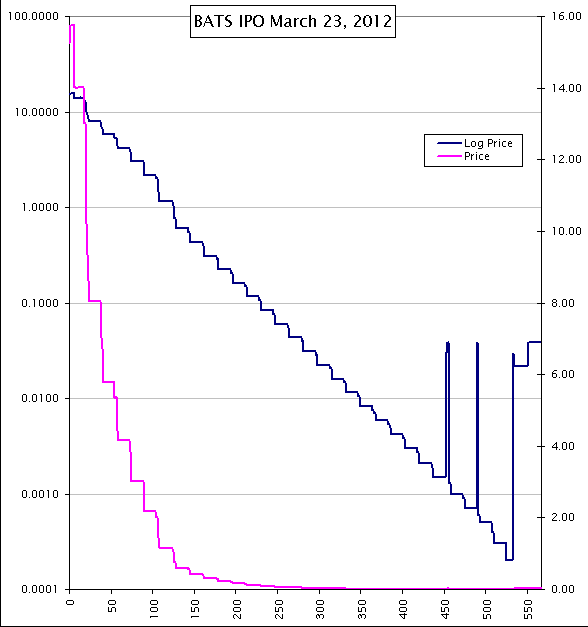

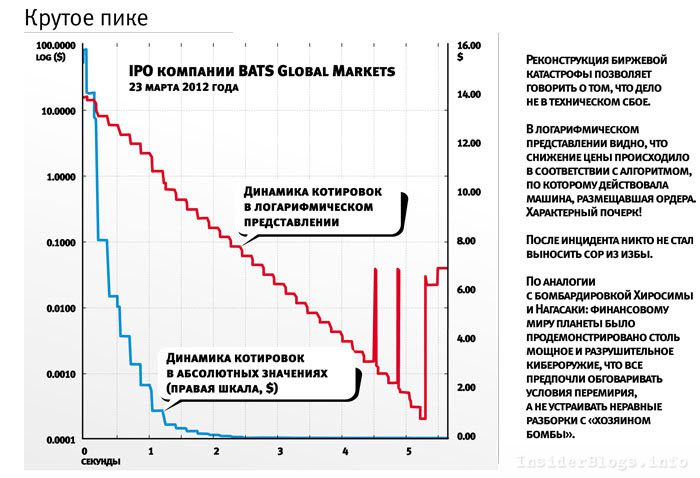

Why is it about the killer algorithm, and not about software failure? Nanex cites several pieces of evidence in his analysis, the most obvious of which is the graph I put here.

The chart displays all 567 deals with IPO BATS, which are presented in two scales. The blue line represents the fall in the value of BATS shares in absolute terms, the red line is taken on a logarithmic scale. In the absolute dimension, we observe a muddled free fall, whereas in the logarithmic representation the price reduction does not occur chaotically, but in strict accordance with a given algorithm by which the machine that placed the orders acted. In other words, the attacker's handwriting is obvious: BATS shares did not depreciate "by mistake" or as a result of a "failure", but were systematically "killed"!

Nanex analysis showed a direct relationship between the Apple and BATS crashes, but Nanex himself did not take the responsibility to make a final statement. However, in its analytical report, this company reported that this is a kind of killer algorithm. The most obvious example is a graph showing deals with paper (see fig.). The graph shows two lines of price decline: absolute and logarithmic scales. It is the logarithmic scale that gives the same algorithm: the price drop in this scale was carried out not chaotically, as usually happens in real market conditions, but consistently. The step chart shows that the shares fell not as a result of a failure, but as a result of someone's planned “trampling into the ground”. On the one hand, this is only a beautiful version, but there are obvious companies that benefit from this situation. Of course,The first thing that comes to mind is the main competitors - the NYSE and the NASDAQ, who don’t like their diminishing share in total trading volume due to the development of BATS. And even more so they are not ready to share such a niche as an IPO with another player.

Will the SEC ever name the killer of an IPO BATS? You can be sure that will not call. If only because all drama participants - and BATS in the first place - this name has long been well known! If the affected company itself chose to take the blame, refusing to remove rubbish from the hut, there are clearly weighty arguments for keeping the silence figure.

What arguments can we talk about? In my opinion, there are two of them.

The first argument: the weight category of the IPO BATS killer in the financial world is such that the alternative platform simply does not see any prospects for itself in any form of open confrontation. For the domestic reader, the situation should remotely resemble army hazing: this is exactly the case when it is wiser for the “young” to swallow a grudge and humbly go to wash the footcloths of the “grandfather” - it will be healthier.

Argument Two: The history of March 23, 2012 can be presented as an analogy with the bombing of Hiroshima and Nagasaki. Such a powerful and destructive cyber weapon was demonstrated to the financial world of the planet, that everyone chose to negotiate truce conditions, rather than arrange unequal showdowns and clarifications with the “bomb owner”.

Now the most important thing.What lesson can ordinary mortals learn from the story told - traders from the street and just inhabitants of our sad planet? The lesson is obvious: to play by the rules created in their own interests by modern dinosaurs - financial elite, fluffy mammals are not under force. Therefore, it remains either to sit quietly in a respectful distance, in no case agreeing to play on someone else's court, which is designed to deliberately beat any outsider, or - to break the rules of dinosaurs!

Source: https://habr.com/ru/post/447834/

All Articles