Allocation of IT costs - is there justice?

I believe that all of us go to a restaurant with friends or colleagues. And after a fun pastime the waiter brings a check. Further the question can be solved in several ways:

- Method one, "gentleman". To the amount of the check, 10–15% is added “for tea” to the waiter, and the resulting amount is divided into all males equally.

- The second way, "socialist". The check is divided equally by all, regardless of who eats and drank so much.

- The third way, "fair." Each one includes a calculator on the phone and starts calculating the cost of its dishes, plus a certain amount of “tea”, also an individual one.

The situation with the restaurant is very similar to the situation with the cost of IT in companies. In this post we will discuss just about the distribution of costs between departments.

But before we dive into the abyss of IT, let's return to the example with a restaurant. Each of the above “cost allocation” methods has pros and cons. The obvious minus of the second method: one could eat a vegetarian Caesar salad without chicken, and the other - a Ribeye steak, so the amounts may differ significantly. The minus of the “fair” method is a very long counting process, and in the amount of money it always turns out to be less than on the check. Common situation?

')

And now let's imagine that we had fun in a restaurant in China, and they brought a check in Chinese. All that is clear there is a sum. Although some may suspect that this is not the sum at all, but the current date. Or suppose it happens in Israel. They read from right to left, but how do they write numbers? Who can answer without Google?

Why is IT needed for IT and business?

So, the IT department provides services to all departments of the company, actually sells its services to business units. And, although there may not be a formal financial relationship between departments within the company, each business unit must at least understand how much it spends on IT, how much it costs to launch new products, test new initiatives, etc. It is obvious that not the mythical “modernizer, patron of system integrators and equipment manufacturers” pays for the modernization and expansion of infrastructure, but a business that must understand the effectiveness of these costs.

Business units vary in size as well as the "intensity" of using IT resources. Thus, to share the cost of upgrading the IT infrastructure equally among the departments - this is the second method with all its drawbacks. The “fair” method is more preferable in this case, but it is too labor-intensive. The best option is a “quasi-fair” option, when costs are allocated not to a penny, but with some reasonable accuracy, just as we use π as 3.14 in school geometry, and not the whole sequence of numbers after the comma.

Estimating the cost of IT services is very useful in holdings with a single IT infrastructure when combining or separating a part of a holding into a separate structure. This allows you to immediately calculate the cost of IT services to take these amounts into account when planning. Also, understanding the cost of IT services helps to compare different uses and ownership of IT resources. When men in costumes for a few thousand dollars tell how their product can optimize IT costs, increase what needs to be increased, and reduce what needs to be reduced, estimating current IT services costs allows the CIO not to blindly trust marketing promises , and accurately assess the expected effect and monitor the results.

For business, allocation is an opportunity to understand in advance the cost of IT services. Any business requirement is not assessed as an increase in the total IT budget by as many percent, but is defined as the amount for a specific requirement or service.

Real case

The key “pain” of the CIO of a large company was that it was necessary to understand how to distribute costs among business units and offer participation in IT development in proportion to consumption.

As a solution, we developed an IT services calculator that was able to distribute total IT costs, first for IT services, and then for business units.

There are actually two tasks: to calculate the cost of an IT service and distribute costs among business units using this service, according to certain drivers (the “quasi-fair” method).

At first glance, it may look simple if from the very beginning IT services were properly described, information was entered into the CMDB configuration database and IT asset management system ITAM, resource-service models were built and the IT services catalog was developed. Indeed, in this case, for any IT service, you can determine what resources it uses and how much these resources are worth considering the depreciation. But we are dealing with an ordinary Russian business, and this imposes some restrictions. So, CMDB and ITAM are missing; there is only a catalog of IT services. Each IT service is generally an information system, access to it, user support, etc. The IT service uses infrastructure services such as “Database Server”, “Application Server”, “Storage System”, “Data Transmission Network”, etc. Accordingly, to solve the set tasks, it is necessary to:

- determine the cost of infrastructure services;

- distribute the cost of infrastructure services to IT services and calculate their cost;

- determine the drivers (ratios) of the distribution of the cost of IT services to the business unit and allocate the cost of IT services to the business unit, thereby distributing the amount of expenses of the IT department among the remaining units of the company.

All annual IT costs can be represented as a bag of money. From this bag, something is spent on equipment, work on migration, modernization, licenses, support, staff salaries, etc. However, the complexity lies in the accounting procedure for the accounting of fixed assets and intangible assets in IT.

Consider for example an SAP infrastructure modernization project. Within the project, equipment and licenses are purchased, works are carried out with the help of a system integrator. When the project is closed, the manager must arrange the papers so that the accounting equipment gets into the fixed assets, the licenses - into the intangible assets, and other design and commissioning works are written off as expenses for future periods. Problem number one: when registering in fixed assets, the accountant of the customer doesn’t care what it will be called. Therefore, in fixed assets we get the asset “UpgradeSAPandMigration”. If the project included upgrading the disk array, which has nothing to do with SAP, this further complicates the search for cost and further allocation. In fact, the equipment “UpgradeSAPandMigration” can hide any kind of equipment, and the more time passes, the more difficult it is to understand what was actually bought there.

Similarly with intangible assets, which have a much more complex calculation formula. Additional complexity is added by the fact that the moment of launching the equipment and putting it on balance may differ by about a year. Plus, depreciation is 5 years, but in fact the equipment can work more or less, depending on the circumstances.

Thus, it is theoretically possible to calculate the cost of IT services with 100% accuracy, but in practice this is a long and rather meaningless exercise. Therefore, we chose a simpler method: the costs that can be easily attributed to any infrastructure or IT service can be attributed directly to the corresponding service. The remaining costs are distributed among IT services according to certain rules. This will allow to obtain an accuracy of about 85%, which is quite enough.

At the first stage , financial and accounting reports on IT projects and “common voluntarism” are used to distribute the costs of infrastructure services in cases where it is not possible to attribute the costs to any infrastructure service. Costs relate either directly to IT services or to infrastructure services. As a result of the allocation of annual costs, we get the amount of expenses for each infrastructure service.

At the second stage , the distribution coefficients between IT services are determined for such infrastructure services as “Application Server”, “Database Server”, “Storage”, etc. Some infrastructure services, such as Jobs, Wi-Fi access, Video conferencing, are not distributed between IT services and are allocated directly to business units.

At this stage, the fun begins. As an example, consider an infrastructure service such as “Application Servers”. It is present in almost every IT service, while in two architectures, with and without virtualization, with redundancy and without. The easiest way is to allocate costs in proportion to the cores used. In order to count in “identical parrots” and not to confuse physical cores with virtual ones, taking into account the oversubscription, we assume that one physical core equates to three virtual ones. Then the formula for allocating the costs of the Application Server infrastructure service for each IT service will look like this:

,

,where Rsp is the total cost of the Application Servers infrastructure service, and Khx86 and Kr are the coefficients denoting the share of x86 and P-series servers.

The coefficients are determined empirically based on an analysis of the IT infrastructure. The cost of cluster software, virtualization software, operating systems and application software is calculated as separate infrastructure services.

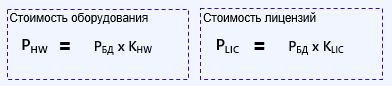

Take an example more complicated. Infrastructure service "Database Servers". The costs of hardware and licenses for the database are sewn into it. Thus, the cost of equipment and licenses can be expressed in the formula:

where HW and LIC are the total cost of the equipment and the total cost of the database licenses, respectively, and KHW and LIC are empirical coefficients that determine the share of costs for hardware and licenses.

Further, with the "iron" is similar to the previous example, and with licenses the situation is a bit more complicated. A company landscape can use several different types of databases, for example, Oracle, MSSQL, Postgres, etc. Thus, the formula for calculating the allocation of a specific database, for example, MSSQL, to a specific service looks like this:

where KMSSQL is a coefficient that determines the share of this database in the company's IT landscape.

The situation is even more complicated with the calculation and allocation of data storage systems with different manufacturers of arrays and different types of disks. But the description of this part is a topic for a separate post.

What is the result?

The result of this exercise can be an Excel calculator or an automation tool. It all depends on the maturity of the company, running processes, implemented solutions and the desire of management. Such a calculator or visual presentation tool helps to properly allocate costs among business units, show how and what the IT budget is distributed to. The same tool can easily demonstrate how improving service reliability (redundancy) increases its cost, and not by the cost of the server, but with all the associated costs. This allows a business and a CIO to “play on the same board” using the same rules. When planning new products, you can calculate the cost in advance and assess the feasibility.

Igor Tukachev, Consultant Jet Infosystems

Source: https://habr.com/ru/post/445716/

All Articles