Fixed and variable costs in software development

Software development and maintenance of already implemented software (for example, applications) is in a special position in the context of cost analysis. The peculiarity is that the typical production cycle of a product and its sale does not exist in the IT industry. Instead, we actually have free copies of the product, but high costs for the very creation of this product and its maintenance. For this reason, the economy of an IT company is very different from the economy of a “candle factory” or a store.

Let's take a closer look at the cost situation in an IT company. Unfortunately, it will not be possible to summarize all IT companies in one scheme. I will try to highlight a few common work patterns and review them. Perhaps some of the readers will add some more interesting schemes for consideration.

I want to highlight the following types of IT companies, although this list is, of course, not complete:

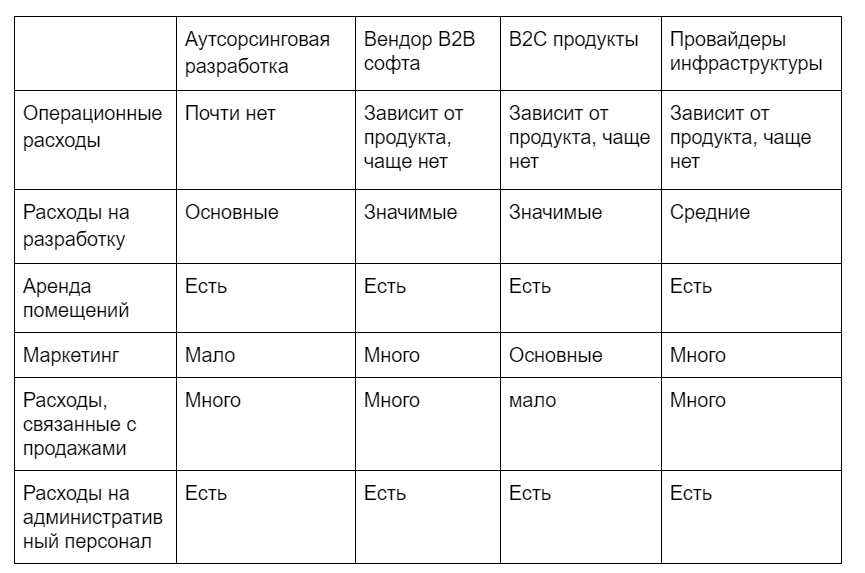

- Outsourcing development - the team writes software for the order and the requirements of the customer. In the future, software is often accompanied by the customer. Relationships focus only on the development and sales of employee watches (both in the form of direct sales of watches and fix price, when the risks of changing the project timeframe fall on the developer)

- B2B software vendor - the team writes software for B2B distribution, implements the implementation, support and development of new functionality.

- B2C products - here I will take all the companies involved in the creation of B2C applications and products that work with a mass client.

- Infrastructure providers - hosters, data centers, server capacities, transaction processing services, etc.

What costs does the first type of company have? Let's divide into different groups the costs of the main types that do not depend on the company:

- Operating expenses

- Costs directly related to the production of 1 unit of production.

- General and administrative expenses

- Development costs

- Rental of premises

- Marketing

- Sales Costs

- Administrative expenses

- Infrastructure costs

- Depreciation

- Financial expenses

- Interest on debt

- Exchange differences

- Revaluation of property

- Taxes

Let me draw your attention to the fact that in finance there is a big difference between “expenses” in the financial sense and “expenses” in the household. On this occasion, I wrote a separate article

Returning to our 4 types of companies, we have the following picture regarding their cost structure (excluding financial expenses):

How to analyze the cost structure of such different enterprises?

Just a picture and cost structure gives us not too much. We can find out the largest articles and this can give us directions for optimization, but it often happens that the largest items of expenditure are the largest, not without reason.

You can try to calculate the cost per 1 unit of the sold service / product from this data. But this information actually gives you nothing. Firstly, we have a mixture of fixed and variable factors, each of which varies in response to rising / falling sales, secondly, the figure for “such” cost does not give you any additional information, which means that you will not take any action for the company on the basis of these you can’t think of data. Besides, for the reasons described above, our investment projects do not fall into this data. The conclusion is that we need a different view on the economy of the enterprise.

One approach is to break up the enterprise into products and projects, and then break down the costs into general and project / product costs. How then the cost structure might look like:

Product

- Direct operating costs of the product

- Total allocated expenses

- Perfomance marketing

- Infrastructure (in terms of assets used)

- Expenses for labor support

- The cost of labor development

- Rental of premises (busy projects)

- Depreciation (in terms of assets used)

- Whole enterprise

- Total non-allocable expenses

- Sales Costs

- Administrative costs

- Brand marketing

- Financial expenses

- Depreciation of common property

- Common infrastructure

Allocated expenses are expenses allocated to a project based on an analytical / expert assessment of resource consumption. When you do not have an unambiguous “account” for the power consumption services of your server infrastructure, you can give an estimate by dividing the maintenance costs in proportion to the use of resources. Do not be carried away by the search for an exact metric, allocation already implies assumptions, therefore you should rather determine a less correct proportion between products than come up with a formula for “fair” calculations.

Nonlocated expenses are expenses whose consumption will not change if you change the scale of your projects. There are expenses that cannot be tied to specific projects and that the company needs in general: brand marketing, financial expenses, accounting costs, lawyers, etc.

What gives us this approach:

- Costs that are directly generated by a separate project are correlated with the revenues generated by it. You understand whether the project is profitable or not. If it is not profitable, it becomes better for you to understand what you will lose when you close it and how much resources you have free.

- You also understand if you are not bury yourself under the weight of bloated general expenses and can try to work on reducing costs in this part. Many of these costs are not productive and their control and minimization is an important task for any manager.

- You can now begin to compare projects and evaluate their dynamics, because now you will not have hidden costs and situations when a project’s profit is fictitious, because The absorption of total associated costs was not taken into account.

Combining this data with the data on revenue and its decomposition into components ( Introductory article, inside, below links to the rest of the cycle of articles ) you get your basic reporting on products and enterprise.

')

Source: https://habr.com/ru/post/422003/

All Articles