How banks will develop blockchain solutions in 2017

In a recently published report, the Indian software company Infosys outlined the main points regarding the prospects for the introduction of blockchain-based business solutions in 2017. We publish the main theses from this report in the blog of our international blockchain service Wirex .

About 50% of the respondent banks admitted that they were waiting for the technology to reach a more mature level of development. In the short term, these banks plan to work out limited scenarios for the application of technology, before allocating funds for larger investments.

')

Just over a third (35%) of respondents fall under the category of “early supporters”. This includes financial institutions that have already identified useful and suitable for their development strategy blockchain cases. They plan to invest in related initiatives in the near future. The range of financing projects in this category is from 1 to 10 million dollars.

Genuine "innovators" are players who have already carried out a full-scale launch of blockchain initiatives with the support of specially established internal teams or partners in the face of technology start-ups and companies. About 15% of banks fell into this category.

Such players have already allocated funds worth over $ 10 million to support initiatives and are exploring experimental blockchain options that go beyond traditional scenarios, such as cross-border transfers, clearing and mutual settlements. In an effort to take advantage of the pioneers, these banks have already taken the first steps in shaping and developing solutions that have all the chances of becoming one of the first full-blooded blockchain-ecosystems in the industry.

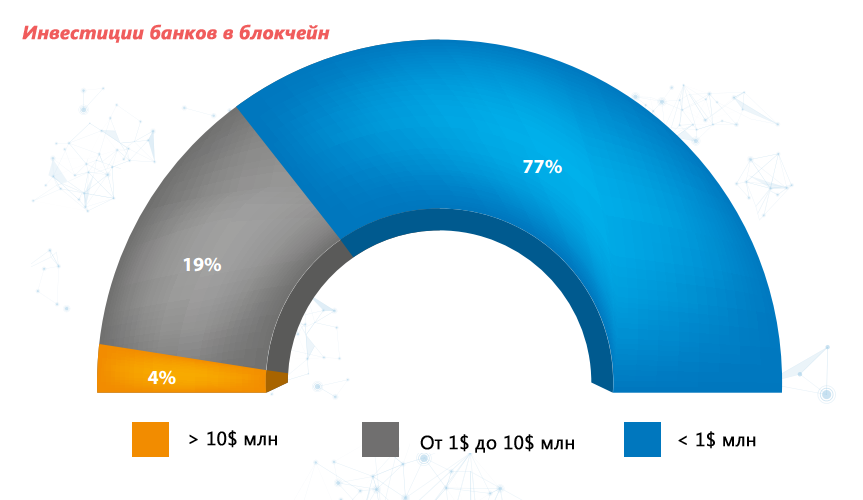

The size of the investment of the majority (77%) of the respondent banks is at the level of $ 1 million. At the same time, 4% of participants reported investing more than $ 10 million. Anyway, the share of this group will grow in the future, since the remaining 19% of participants who have allocated from 1 to 10 million dollars plan to increase funding for blockchain initiatives.

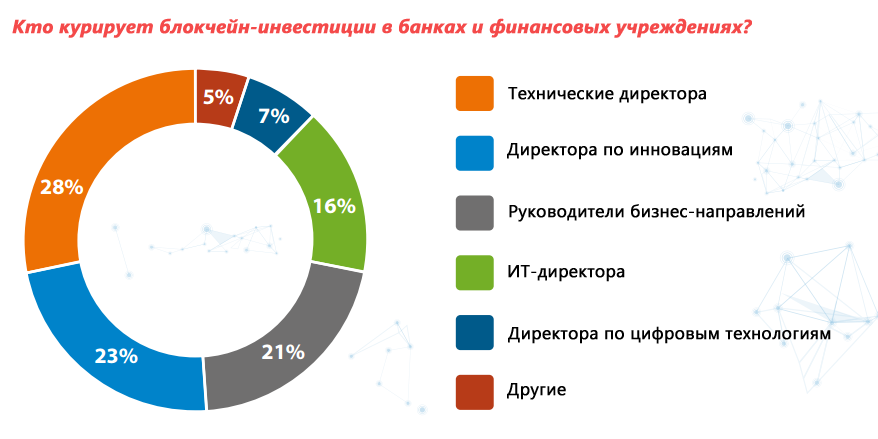

The initiative to finance blockchain projects in banks currently comes from representatives of various departments. In most cases, the heads of technical departments and the director of innovation are the stakeholders, however, the heads of business units are increasingly playing a key role in the launch of related projects. In 28% of the banks surveyed, technical directors are working on blockchain projects, and in 23% of banks this role is assumed by the director of innovation. A variety of options for the application of technology also did not go unnoticed by the heads of business units. Thus, 21% of respondents indicated that such initiatives are under the control of business directors. Representatives of a small proportion of respondents (16%) also reported that in their organization blockchain projects are managed by CIOs, mainly because their activities are also closely related to the operation of business systems.

The security of consumer data and transactions is a matter of primary importance for financial institutions. The concept of open blockchains is associated with security concerns and therefore most of the banks use closed regulated blockchains as a model that can reduce security risks. Closed blockchains also offer greater flexibility, increased reliability and adaptability compared to an open blockchain infrastructure.

69% of surveyed banks reported using the model of closed blockchains. In addition to concerns about security, this choice is due to the ambiguity of the situation with the regulatory approval of open blockchains because they do not provide an opportunity to carry out KYC checks and fulfill anti-money laundering requirements, which, in turn, provokes operational risks.

About 21% of respondents are either already using hybrid blockchains, or are planning to use them in the near future.

Banks are exploring various uses of technology in the financial services industry, both traditional and non-traditional. This survey confirms that the most preferred of them are those that allow you to reduce costs, simplify business processes and increase operational efficiency.

Cross-border payments, digital identity systems, clearing and mutual settlements, along with slightly less relevant cases, such as credit on the basis of payment documents and processing of letters of credit, constitute the top five most preferred application scenarios.

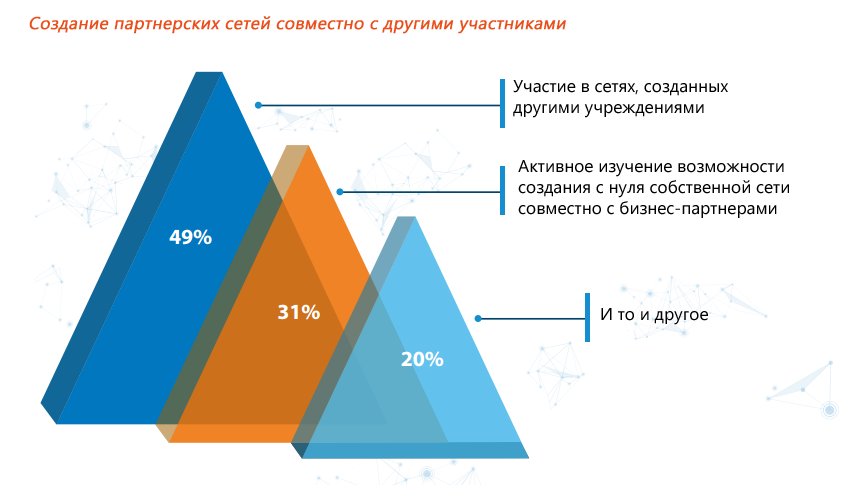

Distributed technology platforms such as blockchains can reach their true potential only with the support of business networks and partner groups. And therefore, it is not surprising that most of the respondent banks have reported participating in partnerships with technology firms, fintech companies, colleagues in their line of business and central organizations aimed at developing blockchain applications. The most preferable (49%) way to create networks of blockchain partners was to participate in already formed associations.

According to the survey, the majority of respondent banks (80%) expect that the full-scale and large-scale use of the blockchain in the financial services industry will be as close as possible to 2020.

The survey participants consider cross-border payments as the most ready for practical implementation case. They expect that the first decisions in this segment will be presented already this year.

Among other application scenarios, they also identified seven areas that, in their opinion, must necessarily acquire full-fledged blockchain applications. This includes documentary operations, loan syndication, clearing and settlement, digital identification of individuals, lending on the basis of payment obligations and smart contracts.

Be that as it may, the authors of the survey conclude that the first practical examples expected in 2017 will not differ in scale or wide coverage. To feel the solidity of blockchain innovations, in their opinion, will succeed no earlier than 2020.

Based on the survey data, they predict that in the next two years we will see the emergence of predominantly intrabank blockchain solutions, or interbank solutions, intended for use within the network of partners in such segments as cross-border payments and digital identification. Then (2–5 years) there will be a period of appearance of other interbank decisions and cases with the participation of regulators, in particular, in the segment of documentary operations. In subsequent years (5 years or more), we will witness a wider spread of Blockchain in the financial services industry and the banking ecosystem.

The authors of the study also expect that by 2020 the spread of blockchain applications will reach a scale sufficient to involve them in larger ecosystems, involving government and corporations from other industries and, possibly, even end users.

The research results show that in the next two years, Blockchain technology will become the main area of research for banks. Today, the main question is no longer whether they will be engaged in the practical implementation of Blockchain, but when and how this will happen. In this regard, the authors of the survey identify two possible directions - internal and external.

Banks can begin to master the technology from in-house cases checked within their own infrastructure in order to subsequently apply their accumulated experience with Blockchain in the course of joint projects with industry partners.

From the point of view of the external direction of development, several banks have already begun to conduct relevant experiments in collaboration with technology partners, as well as having formed consortia.

Further, there follows a brief assessment of the main stages of the practical distribution of blockchain in the coming years, provided by the authors of the survey.

2014–2016. Phase 1. Blockchain Value Analysis for the Financial Services Industry

2016–2018. Phase 2: Concept Verification

2019–2020 Phase 3. The emergence of joint infrastructure

Industry players will begin to implement blockchain products that meet the needs of individual business areas.

Efficient use of collaborative infrastructure, APIs and interfaces to expand the scope of technology.

As Blockchain spreads, consolidation and standardization will become the norm.

Previously competing financial organizations are aware of the benefits of a unified approach, such as accelerating trading processes and improving data management processes for business operations.

2021–2025. Phase 4. Prosperity of blockchain networks

- 50% of the surveyed banks either have already invested in the blockchain technology, or plan to do so in 2017.

- It is expected that in 2017 the average size of investment in blockchain projects will be $ 1 million.

- 33% of respondents expect a widespread blockchain in the commercial sphere to occur in 2018, while most of them (50%) believe that this will happen in 2020.

- Most banks surveyed - about 69% - are experimenting with regulated blockchains. Significant and the proportion of players who choose the hybrid options - 21%.

- Cross-border payments, management of digital means of identification, clearing and settlement, processing letters of credit and loan syndication are the five main cases in which Blockchain, according to respondents, is most likely to receive the most commercial distribution.

- About 50% of the surveyed banks have chosen to cooperate with FINTECH start-ups or technology companies to increase their potential in the field of blockchain solutions. Another 30% took the path of participation in consortia.

- “Ecosystem readiness” and “lack of management models among interested players” were identified as the two most serious difficulties on the path to large-scale application of technology.

- “Improved transparency between counterparties” and “reduction of transaction time and settlement transactions” were recognized as the two most significant advantages of the technology.

- According to 74% of banks surveyed, the technical directors, innovation directors or business leaders are the engines of blockchain projects.

Innovators, early supporters and observers

About 50% of the respondent banks admitted that they were waiting for the technology to reach a more mature level of development. In the short term, these banks plan to work out limited scenarios for the application of technology, before allocating funds for larger investments.

')

Just over a third (35%) of respondents fall under the category of “early supporters”. This includes financial institutions that have already identified useful and suitable for their development strategy blockchain cases. They plan to invest in related initiatives in the near future. The range of financing projects in this category is from 1 to 10 million dollars.

Genuine "innovators" are players who have already carried out a full-scale launch of blockchain initiatives with the support of specially established internal teams or partners in the face of technology start-ups and companies. About 15% of banks fell into this category.

Such players have already allocated funds worth over $ 10 million to support initiatives and are exploring experimental blockchain options that go beyond traditional scenarios, such as cross-border transfers, clearing and mutual settlements. In an effort to take advantage of the pioneers, these banks have already taken the first steps in shaping and developing solutions that have all the chances of becoming one of the first full-blooded blockchain-ecosystems in the industry.

Expected growth in blockchain investments in 2017

The size of the investment of the majority (77%) of the respondent banks is at the level of $ 1 million. At the same time, 4% of participants reported investing more than $ 10 million. Anyway, the share of this group will grow in the future, since the remaining 19% of participants who have allocated from 1 to 10 million dollars plan to increase funding for blockchain initiatives.

Business executives, technical directors and innovation directors lead blockchain-financing

The initiative to finance blockchain projects in banks currently comes from representatives of various departments. In most cases, the heads of technical departments and the director of innovation are the stakeholders, however, the heads of business units are increasingly playing a key role in the launch of related projects. In 28% of the banks surveyed, technical directors are working on blockchain projects, and in 23% of banks this role is assumed by the director of innovation. A variety of options for the application of technology also did not go unnoticed by the heads of business units. Thus, 21% of respondents indicated that such initiatives are under the control of business directors. Representatives of a small proportion of respondents (16%) also reported that in their organization blockchain projects are managed by CIOs, mainly because their activities are also closely related to the operation of business systems.

Most banks (69%) choose the model of a closed regulated blockchain

The security of consumer data and transactions is a matter of primary importance for financial institutions. The concept of open blockchains is associated with security concerns and therefore most of the banks use closed regulated blockchains as a model that can reduce security risks. Closed blockchains also offer greater flexibility, increased reliability and adaptability compared to an open blockchain infrastructure.

69% of surveyed banks reported using the model of closed blockchains. In addition to concerns about security, this choice is due to the ambiguity of the situation with the regulatory approval of open blockchains because they do not provide an opportunity to carry out KYC checks and fulfill anti-money laundering requirements, which, in turn, provokes operational risks.

About 21% of respondents are either already using hybrid blockchains, or are planning to use them in the near future.

Quick reference

- An open blockchain is a completely decentralized blockchain. Anyone can join his work and participate in the process of achieving consensus.

- The hybrid blockchain works in a consortium-like manner, where the consensus process is controlled by a certain group of nodes.

- In a closed blockchain, stricter access control is applied, including by separating the rights of reading and changing certain information.

Cross-border payments, digital identity systems, clearing and mutual settlements are the most preferred scenarios for blockchain applications.

Banks are exploring various uses of technology in the financial services industry, both traditional and non-traditional. This survey confirms that the most preferred of them are those that allow you to reduce costs, simplify business processes and increase operational efficiency.

Cross-border payments, digital identity systems, clearing and mutual settlements, along with slightly less relevant cases, such as credit on the basis of payment documents and processing of letters of credit, constitute the top five most preferred application scenarios.

Partnership agreements play a key role in blockchain projects

Distributed technology platforms such as blockchains can reach their true potential only with the support of business networks and partner groups. And therefore, it is not surprising that most of the respondent banks have reported participating in partnerships with technology firms, fintech companies, colleagues in their line of business and central organizations aimed at developing blockchain applications. The most preferable (49%) way to create networks of blockchain partners was to participate in already formed associations.

Some common patterns of technology introduction to the market

According to the survey, the majority of respondent banks (80%) expect that the full-scale and large-scale use of the blockchain in the financial services industry will be as close as possible to 2020.

The survey participants consider cross-border payments as the most ready for practical implementation case. They expect that the first decisions in this segment will be presented already this year.

Among other application scenarios, they also identified seven areas that, in their opinion, must necessarily acquire full-fledged blockchain applications. This includes documentary operations, loan syndication, clearing and settlement, digital identification of individuals, lending on the basis of payment obligations and smart contracts.

Be that as it may, the authors of the survey conclude that the first practical examples expected in 2017 will not differ in scale or wide coverage. To feel the solidity of blockchain innovations, in their opinion, will succeed no earlier than 2020.

Based on the survey data, they predict that in the next two years we will see the emergence of predominantly intrabank blockchain solutions, or interbank solutions, intended for use within the network of partners in such segments as cross-border payments and digital identification. Then (2–5 years) there will be a period of appearance of other interbank decisions and cases with the participation of regulators, in particular, in the segment of documentary operations. In subsequent years (5 years or more), we will witness a wider spread of Blockchain in the financial services industry and the banking ecosystem.

The authors of the study also expect that by 2020 the spread of blockchain applications will reach a scale sufficient to involve them in larger ecosystems, involving government and corporations from other industries and, possibly, even end users.

Way ahead

The research results show that in the next two years, Blockchain technology will become the main area of research for banks. Today, the main question is no longer whether they will be engaged in the practical implementation of Blockchain, but when and how this will happen. In this regard, the authors of the survey identify two possible directions - internal and external.

Banks can begin to master the technology from in-house cases checked within their own infrastructure in order to subsequently apply their accumulated experience with Blockchain in the course of joint projects with industry partners.

From the point of view of the external direction of development, several banks have already begun to conduct relevant experiments in collaboration with technology partners, as well as having formed consortia.

Further, there follows a brief assessment of the main stages of the practical distribution of blockchain in the coming years, provided by the authors of the survey.

2014–2016. Phase 1. Blockchain Value Analysis for the Financial Services Industry

- Banks and financial infrastructure intermediaries formed industry groups to discuss opportunities.

- Creation of closed groups of representatives of the industry, as well as their technological and fintech partners.

- Creating partnership projects covering the entire industry, such as the R3 and Linux Hyperledger Foundation.

2016–2018. Phase 2: Concept Verification

- Search for key concepts that can have a particular impact on the business and assess the possibility of scaling up blockchain solutions in order to reduce costs while maintaining an adequate level of security.

- The dialogue between regulators, auditors, partners and the ecosystem in order to identify the most important processes that need to be optimized, which will benefit the most from technology implementation.

- The goal of test projects is to evaluate whether blockchain processes provide any advantages in terms of performance, price, speed, and scalability compared to existing processes.

- Despite the fact that some influential consortia were already formed by 2017, on the whole, the issue of establishing a collective dialogue and joint agreements on universal and flexible open industry standards remains open.

- Governments and regulators will play an important role, which will be to protect consumers and at the same time encourage innovation.

2019–2020 Phase 3. The emergence of joint infrastructure

Industry players will begin to implement blockchain products that meet the needs of individual business areas.

Efficient use of collaborative infrastructure, APIs and interfaces to expand the scope of technology.

As Blockchain spreads, consolidation and standardization will become the norm.

Previously competing financial organizations are aware of the benefits of a unified approach, such as accelerating trading processes and improving data management processes for business operations.

2021–2025. Phase 4. Prosperity of blockchain networks

- Completion of the formation and strengthening of standards for interoperability and communication channels.

Source: https://habr.com/ru/post/400569/

All Articles