Global map: how different countries of the world approach the development of fintech

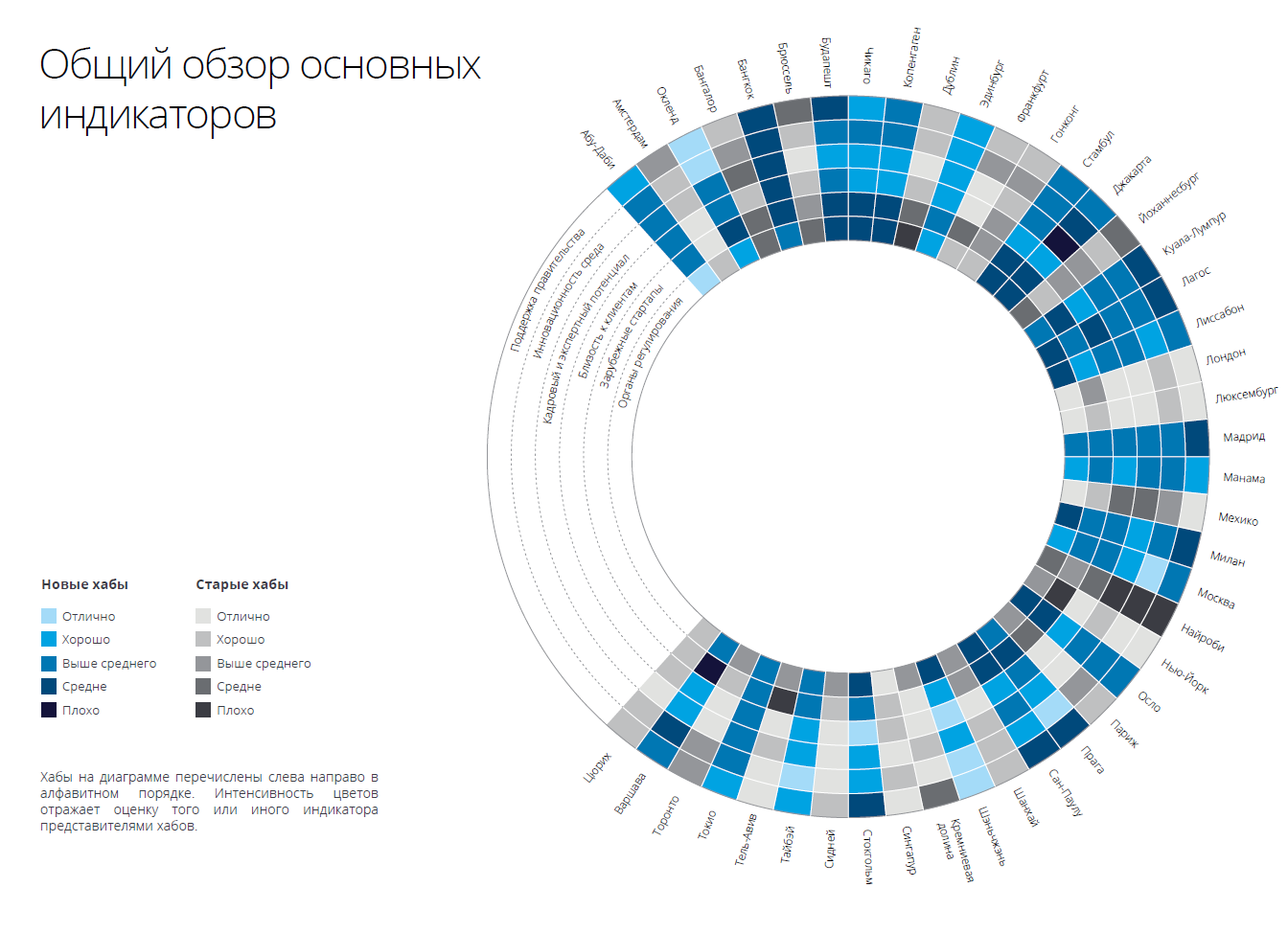

Auditing and consulting company Deloitte conducted a study in which it revealed that the new European fintech hubs, and especially those located in the European Union, tend to rate the local human resources highly. On the other hand, most of the 12 new European hubs rated local regulation of Fintech negatively, and regulatory barriers were noted as one of the ordinary difficulties.

Auditing and consulting company Deloitte conducted a study in which it revealed that the new European fintech hubs, and especially those located in the European Union, tend to rate the local human resources highly. On the other hand, most of the 12 new European hubs rated local regulation of Fintech negatively, and regulatory barriers were noted as one of the ordinary difficulties.The Deloitte study of regulatory sandboxes and collaboration between supervisors confirms the validity of these points of view. His results show that of all European countries only the UK, the Netherlands, Russia, Switzerland and Norway (5 of the 20 European fintech hubs included in the report) are working on projects of sandtech fintech. At the same time, only three supervisory bodies (in Great Britain, France and Switzerland) concluded agreements on cooperation in the field of fintech with their colleagues from other countries of the world.

Representatives from the Asia-Pacific region, unlike their European counterparts, were more positive in their assessments of local regulation, and for good reason. Throughout the past year, we have witnessed many constructive actions by supervisory authorities throughout Asia, and the speed of these changes left the most pleasant impression. For example, 7 out of 16 regulators who have committed themselves to the deployment of regulatory sandboxes are located in Asia. Moreover, the Asian supervisory authorities have taken a very active position regarding cooperation with their colleagues from other regions of the world.

For example, as shown in the following map of regulator cooperation, international cooperation agreements with regulators from other countries among Asian countries were signed by China, South Korea, Hong Kong, Japan, Singapore, Australia and India. The Monetary Authority of Singapore has become the absolute record holder for this indicator worldwide. Of course, it should be remembered that the tangible fruits of these agreements are yet to be seen. Be that as it may, collaboration between regulators around the world has undoubtedly become commonplace, gaining momentum.

')

The countries of the Persian Gulf in the report are represented by only two hubs. Both of their representatives gave very similar ratings. For example, they declared excellent government and regulatory support for fintech companies, which was repeatedly confirmed by a number of initiatives launched by the governments of these countries together with the supervisory authorities. As a supporting example, RegLab in Abu Dhabi, FinTech Hive and 2020 blockchain projects in Dubai and the work of FinTech by the Bahrain Economic Development Council are examples.

In Africa, the development of financial technology continues to revolve around mobile and social payments. Fintech projects that enjoy great success are rare for the region due to the low level of support from the government and regulators, as well as the lack of quality infrastructure. All these factors remain obstacles to the large-scale development of local initiatives.

In Central and South America, Brazil is the leader of the pack, most of the Fintech projects and activities are concentrated in Sao Paulo. On the whole, investors and corporations make an active contribution to the development of local Fintech ecosystems. Nevertheless, there are more and more signs of growing support from the government and regulators. For example, it is expected that the new government strategy for expanding access to financial services in Mexico will actively stimulate Fintech growth.

The Deloitte study concludes with information about North America. Silicon Valley and New York continue to be the undisputed leaders of Fintech USA. As for Canada, 80% of all Canadian fintech activities are still concentrated in Toronto. Nevertheless, in recent years we have witnessed the emergence of several more new hubs: Chicago and Charlotte (North Carolina) included in this interim report.

Other changes in the United States over the past few months relate to regulation. The Fintech Charter of the Office of the Comptroller of Monetary Circulation (US Federal Agency) deserves special attention. Taking into account the fact that the complicated and fragmented regulatory environment of the United States was more than once designated by the Fintech hubs of the United States as an obstacle, it will be interesting to observe developments in this direction.

The full version of the report is available here .

Source: https://habr.com/ru/post/399303/

All Articles