Banks against blockchain

The blockchain technology is designed to radically change various sectors of the economy, but most of the potential for its use is concentrated in the financial sector, including and in banks. In this article, we compare a number of pilot blockchain projects implemented by Russian banks with similar projects from their foreign counterparts.

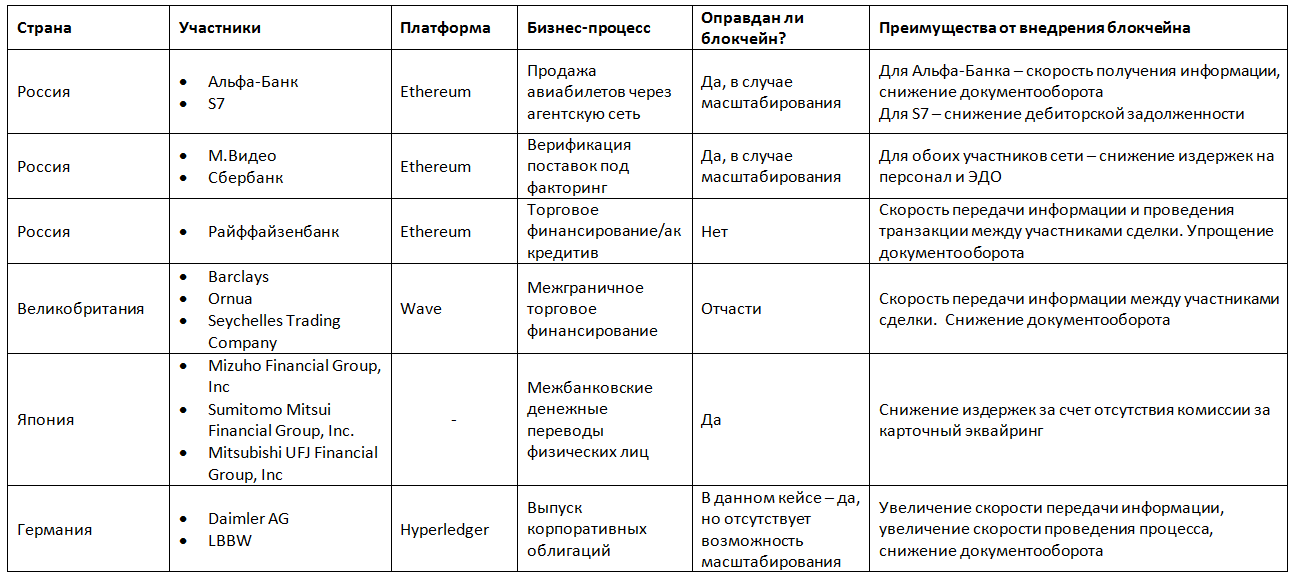

The table provides a brief description of the projects (clickable), in more detail we will describe them below.

Alfa-Bank and S7 airline

')

In July 2017, Alfa-Bank launched a joint project with S7 airlines. In short, this is a private Ethereum blockchain for settlements between the airline and its ticket agents. Alfa-Bank acts as a settlement bank in this scheme. Why is blockchain needed here?

At first glance, it seems that such interaction could be configured using OpenAPI or directly connecting airline systems to bank systems (host-to-host). But, if the system is scaled and other banks and / or airlines connect to this platform, the problem of distrust arises. This is exactly the subject area in which the blockchain is most effective. Plus, a private blockchain allows the platform owner to adjust the block size and commission size depending on the network load. By the way, a smart contract that is quite simple in its logic works on the network. His task is to no more than give instructions to the systems of the bank and the airline to perform certain functions. By itself, he does not make any calculations.

For an airline, this way of working with agents completely changes the established business process. Prior to the introduction of this product, the airline issued agent for the sale of tickets for a certain amount under a bank guarantee. At the end of each decade, reconciliations were made and only after that calculations were made. In other words, the airline acted as a lender for its agents. This is how not only the S7 works, this is a business model established in the airline industry. After the introduction of the blockchain, settlements with agents occur in real time, which allows the airline to reduce receivables.

This platform is a good example of the use of the blockchain (only in the case of scaling), but the presence of a certain central settlement center does not make this project the reference application of the blockchain, although without it this system could not work in current market realities.

At this stage (while there are 2 participants in the system) for the bank, the blockchain only speeds up the settlement time and simplifies the workflow, but for the airline, the blockchain has allowed to change the usual business processes and reduce accounts receivable.

Sberbank Factoring and M.Video

M.Video and Sberbank Factoring have recently used a blockchain platform to verify deliveries for factoring. How it works? M.Video and Sberbank Factoring in a certain format download data on all deliveries that are available in their systems through the web interface in the blockchain. A smart contract on the private network Ethereum makes a comparison of data from both files, and as a result, gives each participant of the network their own files, but with a note whether the counterparty’s supply is found or not. What is this way of interaction better EDT or other solutions?

As in the case of the project of Alfa-Bank and S7, when scaling the platform, the inclusion of new factors or debtors raises questions of distrust and preservation of confidential information. Blockchain due to decentralization will avoid these difficulties. Moreover, this platform can be a unified and unique way to verify deliveries, especially for debtors whose suppliers can be funded in various banks. It is quite problematic and costly to use and maintain various ways of interaction: some use EDM, others have some internal systems for such needs, others do it manually using telephone and mail. The presence of a universal smart contract will unify the verification process, optimize the costs of both factors and debtors.

At the moment, a new factor has joined the platform - Alfa-Bank, which already makes the use of the blockchain justified, since both factors do not want to disclose to each other information about the suppliers they serve, hence the problem of distrust, which is closed using the blockchain. Among all the projects implemented by Russian banks, this is the most revealing, since at the moment it solves several problems for the participants at once:

Moreover, this platform has much to develop. It is possible that in the near future, the calculations and financing of suppliers on the basis of reconciliation will also be transferred to the smart contract.

Blockchain platform for trade finance transactions from Raiffeisenbank

This is an example that cannot be called a working solution, but the R & D division of Raiffeisenbank, as an experiment, created a working concept platform for trade finance on the private Ethereum network.

This is another example of how an existing banking product can be passed on to the blockchain. A rather significant case in which the blockchain is used only to speed up processes. This is more like an experiment with a new technology, and representatives of the bank do not hide it.

The main problem of this example is that both the buyer and the seller are served in the same bank, which is the guarantor of the transaction. This is the original idea of the project - nothing goes beyond the bank. Then, if all the processes are carried out inside the bank, why use the technology that was created in order to remove some central control body from the interaction and make everything decentralized?

Yes, such a solution can significantly reduce workflow and automate some processes, but in general, the solution seems to be incomplete.

Taking into account the fact that the authors of the project themselves state that this is just a way to learn the technology of the blockchain, and most likely this way of interaction will not be working, there is nothing wrong with this project if its authors draw the right conclusions.

Trade Finance Barclays Bank

Unlike the Raiffeisenbank example, the Barclays team went a little different way. They tried to use the blockchain to speed up the transfer of information across the borders of countries, while the funds were sent in a standard way through SWIFT channels. It is worth noting that this decision formed the basis of the “Digital Letter of Credit” solution, which will be used in Masterchain (a project of the Central Bank of the Russian Federation and the Fintech Association). There are two main differences between this project and the Raiffeisenbank project:

If the first is a positive fact in the direction of the implementation of Barclays when comparing two very similar projects, the second difference is a big step in the direction opposite to decentralization. It turns out that Barclays is a central element in the issue of storing documentation and has the ability to "make changes to the data stored on the server."

Speaking about the project as a whole and comparing it with the Raiffeisenbank project, we can say that, conceptually, the Barclays project has advanced a little further from the development point of view than its Russian counterpart.

Interbank P2P transfers in Japan

This case is similar to the project M.Video and Sberbank Factoring, because it also focuses on the banking product and a significant reduction in costs. And this is also one of the most illustrative projects in terms of decentralization. The dream that banks around the world dreamed of — getting rid of card acquiring, reducing costs, and not paying a Visa and MasterCard commission — was realized and implemented by the Japanese company Fujitsu and three Japanese banks. Fujitsu was able to make a fairly simple, elegant and decentralized solution using the blockchain.

The blockchain network is used in this case as a transmitter of information between banks and at the same time a clearing system that informs one bank how much money it should transfer to the benefit of another bank. The use of this kind of solutions, as well as standard interbank channels and methods of interaction, allow to bypass third parties of a fairly simple business process.

This example also demonstrates that to solve any existing problems it is not necessary to use cryptocurrency or tokens. Proper use of the blockchain can significantly affect the income and business of the bank.

Comparing it with the solution from M.Video and Sberbank Factoring, it is important to say that this interaction can also be a kind of unified solution that will save all system participants from various systems, central authorities and / or a large amount of manual tasks.

It is also worth noting that the M.Video project to some extent "kills" the business providers of EDI, and the Fujitsu project, first of all, hits Visa and MasterCard.

Daimler AG bond issue by LBBW Bank

As you might guess, the third case, which I would like to consider, will be somewhat similar to the project of Alfa-Bank and S7. Here we will also talk about the business process, which is difficult to imagine without the participation of the bank, but it brings more benefits to the bank’s customer. With the participation of Landesbank Baden-Württemberg (LBBW), Daimler AG has issued corporate bonds worth € 100 million using blockchain technology.

The entire transaction cycle in this project (from the creation, distribution, execution of the loan agreement to confirmation of the repaid loan and interest on it) was automated in digital form via the blockchain. Everything is implemented on the Hyperledger system. In addition to the automaker and the bank, German banks were also involved in the project, which were bond buyers.

What is remarkable about blockchain here? In general, a certain decentralization is present in this system, LBBW acts only as a guarantor of funds, and the whole cycle passes through a decentralized network. A certain degree of mistrust among potential buyers arises even in the absence of system scalability, and therefore, the use of blockchain is fully justified.

Moreover, both for the auto concern and for banks, such a system significantly reduces the amount of manual labor, increases the speed of information transfer and transactions.

Comparing this project with the solution from Alfa-Bank and S7, it is worth noting that even in the absence of scalability, the Daimler AG solution looks more concise and the use of the blockchain is more justified. But, taking into account the fact that in the future, the Alfa-Bank platform and S7 will be more decentralized and large-scale, then their decision to use the blockchain will be more correct. In the case of German companies, it is difficult to imagine how such a solution can be turned into a decentralized platform.

All the above solutions are not an ideal and a standard to which one should strive when developing a corporate blockchain project. Some projects are more accurate and adequate in terms of using the benefits of decentralization, others are just experiments for testing a new technology.

There are three factors that greatly complicate and limit the possibilities for implementing a blockchain project:

Russian banks are not lagging behind their international competitors. Those products that are born in the R & D divisions of banks and companies can easily be scaled to the international market.

The table provides a brief description of the projects (clickable), in more detail we will describe them below.

Russian banks

Alfa-Bank and S7 airline

')

In July 2017, Alfa-Bank launched a joint project with S7 airlines. In short, this is a private Ethereum blockchain for settlements between the airline and its ticket agents. Alfa-Bank acts as a settlement bank in this scheme. Why is blockchain needed here?

At first glance, it seems that such interaction could be configured using OpenAPI or directly connecting airline systems to bank systems (host-to-host). But, if the system is scaled and other banks and / or airlines connect to this platform, the problem of distrust arises. This is exactly the subject area in which the blockchain is most effective. Plus, a private blockchain allows the platform owner to adjust the block size and commission size depending on the network load. By the way, a smart contract that is quite simple in its logic works on the network. His task is to no more than give instructions to the systems of the bank and the airline to perform certain functions. By itself, he does not make any calculations.

For an airline, this way of working with agents completely changes the established business process. Prior to the introduction of this product, the airline issued agent for the sale of tickets for a certain amount under a bank guarantee. At the end of each decade, reconciliations were made and only after that calculations were made. In other words, the airline acted as a lender for its agents. This is how not only the S7 works, this is a business model established in the airline industry. After the introduction of the blockchain, settlements with agents occur in real time, which allows the airline to reduce receivables.

This platform is a good example of the use of the blockchain (only in the case of scaling), but the presence of a certain central settlement center does not make this project the reference application of the blockchain, although without it this system could not work in current market realities.

At this stage (while there are 2 participants in the system) for the bank, the blockchain only speeds up the settlement time and simplifies the workflow, but for the airline, the blockchain has allowed to change the usual business processes and reduce accounts receivable.

Sberbank Factoring and M.Video

M.Video and Sberbank Factoring have recently used a blockchain platform to verify deliveries for factoring. How it works? M.Video and Sberbank Factoring in a certain format download data on all deliveries that are available in their systems through the web interface in the blockchain. A smart contract on the private network Ethereum makes a comparison of data from both files, and as a result, gives each participant of the network their own files, but with a note whether the counterparty’s supply is found or not. What is this way of interaction better EDT or other solutions?

As in the case of the project of Alfa-Bank and S7, when scaling the platform, the inclusion of new factors or debtors raises questions of distrust and preservation of confidential information. Blockchain due to decentralization will avoid these difficulties. Moreover, this platform can be a unified and unique way to verify deliveries, especially for debtors whose suppliers can be funded in various banks. It is quite problematic and costly to use and maintain various ways of interaction: some use EDM, others have some internal systems for such needs, others do it manually using telephone and mail. The presence of a universal smart contract will unify the verification process, optimize the costs of both factors and debtors.

At the moment, a new factor has joined the platform - Alfa-Bank, which already makes the use of the blockchain justified, since both factors do not want to disclose to each other information about the suppliers they serve, hence the problem of distrust, which is closed using the blockchain. Among all the projects implemented by Russian banks, this is the most revealing, since at the moment it solves several problems for the participants at once:

- Reducing staff costs;

- Reducing the number of systems used by the customer and the factor;

- Creating a new unified way of interaction without a central participant, as is the case with the EDM.

Moreover, this platform has much to develop. It is possible that in the near future, the calculations and financing of suppliers on the basis of reconciliation will also be transferred to the smart contract.

Blockchain platform for trade finance transactions from Raiffeisenbank

This is an example that cannot be called a working solution, but the R & D division of Raiffeisenbank, as an experiment, created a working concept platform for trade finance on the private Ethereum network.

This is another example of how an existing banking product can be passed on to the blockchain. A rather significant case in which the blockchain is used only to speed up processes. This is more like an experiment with a new technology, and representatives of the bank do not hide it.

The main problem of this example is that both the buyer and the seller are served in the same bank, which is the guarantor of the transaction. This is the original idea of the project - nothing goes beyond the bank. Then, if all the processes are carried out inside the bank, why use the technology that was created in order to remove some central control body from the interaction and make everything decentralized?

Yes, such a solution can significantly reduce workflow and automate some processes, but in general, the solution seems to be incomplete.

Taking into account the fact that the authors of the project themselves state that this is just a way to learn the technology of the blockchain, and most likely this way of interaction will not be working, there is nothing wrong with this project if its authors draw the right conclusions.

Foreign banks

Trade Finance Barclays Bank

Unlike the Raiffeisenbank example, the Barclays team went a little different way. They tried to use the blockchain to speed up the transfer of information across the borders of countries, while the funds were sent in a standard way through SWIFT channels. It is worth noting that this decision formed the basis of the “Digital Letter of Credit” solution, which will be used in Masterchain (a project of the Central Bank of the Russian Federation and the Fintech Association). There are two main differences between this project and the Raiffeisenbank project:

- In the case of Raiffeisenbank, all operations were carried out within one bank. In the case of Barclays, this is cross-border trade finance, in which the bank acts as a platform owner and information transfer guarantor;

- In its decision, Raiffeisenbank used Storj.io decentralized platform to store information and documents, while Barclays used a centralized server that stores the document and the hash of this document, which is put into the blockchain.

If the first is a positive fact in the direction of the implementation of Barclays when comparing two very similar projects, the second difference is a big step in the direction opposite to decentralization. It turns out that Barclays is a central element in the issue of storing documentation and has the ability to "make changes to the data stored on the server."

Speaking about the project as a whole and comparing it with the Raiffeisenbank project, we can say that, conceptually, the Barclays project has advanced a little further from the development point of view than its Russian counterpart.

Interbank P2P transfers in Japan

This case is similar to the project M.Video and Sberbank Factoring, because it also focuses on the banking product and a significant reduction in costs. And this is also one of the most illustrative projects in terms of decentralization. The dream that banks around the world dreamed of — getting rid of card acquiring, reducing costs, and not paying a Visa and MasterCard commission — was realized and implemented by the Japanese company Fujitsu and three Japanese banks. Fujitsu was able to make a fairly simple, elegant and decentralized solution using the blockchain.

The blockchain network is used in this case as a transmitter of information between banks and at the same time a clearing system that informs one bank how much money it should transfer to the benefit of another bank. The use of this kind of solutions, as well as standard interbank channels and methods of interaction, allow to bypass third parties of a fairly simple business process.

This example also demonstrates that to solve any existing problems it is not necessary to use cryptocurrency or tokens. Proper use of the blockchain can significantly affect the income and business of the bank.

Comparing it with the solution from M.Video and Sberbank Factoring, it is important to say that this interaction can also be a kind of unified solution that will save all system participants from various systems, central authorities and / or a large amount of manual tasks.

It is also worth noting that the M.Video project to some extent "kills" the business providers of EDI, and the Fujitsu project, first of all, hits Visa and MasterCard.

Daimler AG bond issue by LBBW Bank

As you might guess, the third case, which I would like to consider, will be somewhat similar to the project of Alfa-Bank and S7. Here we will also talk about the business process, which is difficult to imagine without the participation of the bank, but it brings more benefits to the bank’s customer. With the participation of Landesbank Baden-Württemberg (LBBW), Daimler AG has issued corporate bonds worth € 100 million using blockchain technology.

The entire transaction cycle in this project (from the creation, distribution, execution of the loan agreement to confirmation of the repaid loan and interest on it) was automated in digital form via the blockchain. Everything is implemented on the Hyperledger system. In addition to the automaker and the bank, German banks were also involved in the project, which were bond buyers.

What is remarkable about blockchain here? In general, a certain decentralization is present in this system, LBBW acts only as a guarantor of funds, and the whole cycle passes through a decentralized network. A certain degree of mistrust among potential buyers arises even in the absence of system scalability, and therefore, the use of blockchain is fully justified.

Moreover, both for the auto concern and for banks, such a system significantly reduces the amount of manual labor, increases the speed of information transfer and transactions.

Comparing this project with the solution from Alfa-Bank and S7, it is worth noting that even in the absence of scalability, the Daimler AG solution looks more concise and the use of the blockchain is more justified. But, taking into account the fact that in the future, the Alfa-Bank platform and S7 will be more decentralized and large-scale, then their decision to use the blockchain will be more correct. In the case of German companies, it is difficult to imagine how such a solution can be turned into a decentralized platform.

All the above solutions are not an ideal and a standard to which one should strive when developing a corporate blockchain project. Some projects are more accurate and adequate in terms of using the benefits of decentralization, others are just experiments for testing a new technology.

There are three factors that greatly complicate and limit the possibilities for implementing a blockchain project:

- All projects are private networks. The private network partially solves the problem of distrust, because the owner / author of the system chooses who to connect to it and who to leave behind. In this regard, any private network provides only the speed of information transfer, which, in part, can be solved by using other technologies, such as, for example, OpenAPI;

- Due to the uncertain legal status of cryptocurrencies and tokens, banks and companies refuse to use them in their systems, which, in most cases, forces the use of some third party (bank) to conduct settlements;

- The legal status of the blockchain is also not defined, most of them have no precedents when the data from the blockchain were accepted by the court as evidence of something. In this regard, many companies are afraid to use the blockchain for money transfer. Therefore, the main sight is to accelerate the transfer of information, and the money goes by standard routes (SWIFT or other methods of interbank transfers).

Russian banks are not lagging behind their international competitors. Those products that are born in the R & D divisions of banks and companies can easily be scaled to the international market.

Links to project information

Source: https://habr.com/ru/post/374035/

All Articles