IT asset management: how myths affect projects

All happy projects are alike, each unhappy project is unhappy in its own way.

For 6 years I have been engaged in the implementation and automation of business processes, of which for 3 years I have been implementing ITAM solutions. In projects for automating IT asset management processes, we constantly struggle with various myths.

The nature of these misconceptions is very different: lack of understanding of the methodology, technical aspects, errors in the construction of interrelationships of processes, unjustified expectations, etc.

Consider these myths in more detail, try to dispel them or confirm.

What is an IT asset

To exclude discrepancies, to begin with - about the terms.

IT asset management processes describe several knowledge sources: IAITAM (IBPL), ITIL, COBIT5, ISO 19770, and more. Dr. Naumen, in its practice, uses the above-mentioned sources of knowledge for the organization of IT asset management, but relies on ITIL and IBPL. Therefore, we define an IT asset as an object that participates in service processes, in the formation of the cost of providing IT services and contributes to the formation of its value to the client.

In addition, the IT asset and configuration unit (CU) is not the same for us. The difference is that an IT asset has an extended life cycle compared to KE and covers planning, provision, procurement and decommissioning. An IT asset can be considered a KE, but not every KE is an IT asset.

Parse the myths and get rid of delusions.

Automatic inventory ensures that IT asset information is up to date.

The first myth is one of the most popular. In 8 out of 10 projects, the goal of implementation is: to automate the routine process of collecting information about hardware and software. It's hard to argue with that, because modern inventory tools help to abandon the manual maintenance of data on IT assets.

What is the information about the IT asset:

- Properties of the asset itself. Almost all information about an IT asset can be collected and updated automatically. Name, model, manufacturer, responsible for the operation, etc.

- Financial information. In most cases, it comes from another inventory system or is accumulated automatically. Cost, balance holder, warranty period, procurement contract, etc. One BUT: agreement is required on the rules for matching the IT asset and the Fixed asset if the project is a different concept.

- Configuration information If a configuration model is used, information about the asset and its relationships can be calculated based on it.

- Cost Management Model. Financial and licensing models are used. Cost-sharing drivers, consumed licenses, etc.

The nuance is that some of the properties of an IT asset cannot be automatically collected. For example, how to locate an asset? This is a property of the physical world. As an option, prescribe the principle of IP subnetworks in the configuration model, then continue to maintain a rule base for location and IP subnetwork matching.

The status of an IT asset must be managed through operational processes. The link to the Asset should be set manually, but this can be automated. To do this, it is enough to adjust the interface with the procurement planning process: provide information on purchases in the form of procurement items that will then be easily compared with an IT asset.

Information about the location of the IT asset in the resource-service model or in the resource-financial and licensing models can be obtained automatically, but then the primary task is to carefully conduct this model.

As a result, automatic inventory ensures the relevance of data on IT assets, but it is difficult to do without additional design and “manual” configuration.

Bundling with ITSM-system is not required

The next common myth is that IT asset accounting does not require tight integration with ITSM systems and other user support processes.

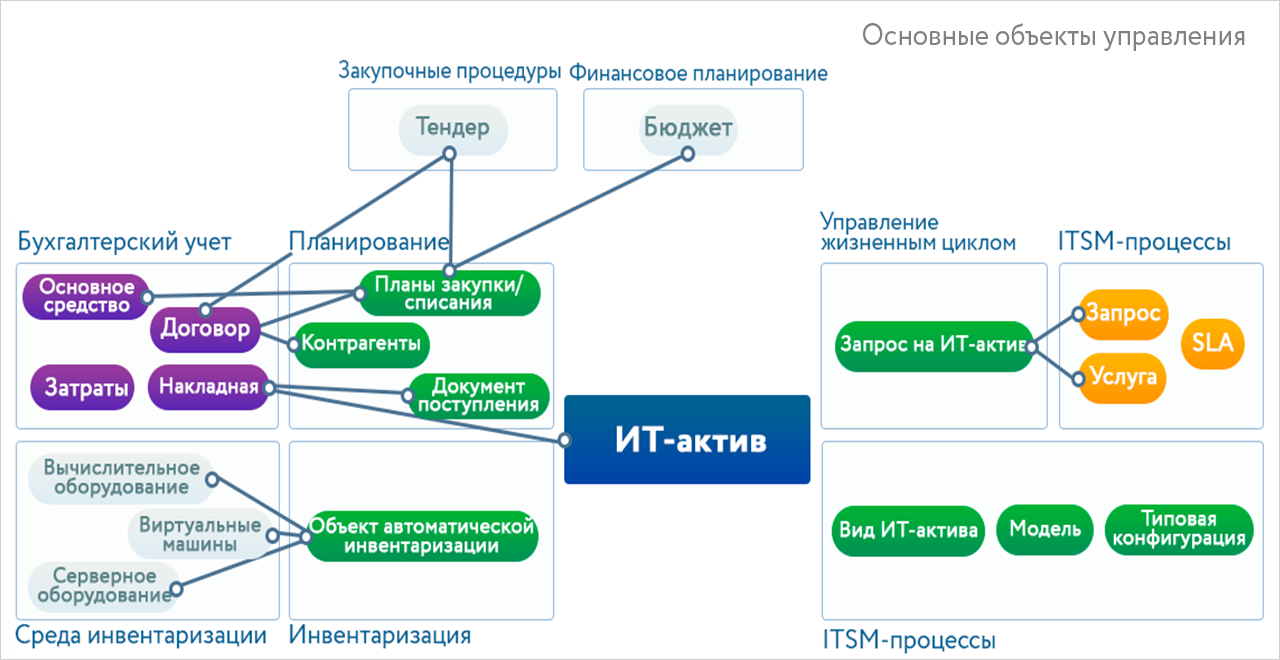

Let's refute this thesis. To do this, consider a simplified model of management objects in the framework of IT asset management processes.

The diagram shows that requests for IT assets and user requests are interrelated. Also traced their relationship with services. In turn, information on the classification and typical configurations of IT assets is used in typical service requests and model change requests. And the IT asset management processes themselves are closely related to IT service management processes.

Thus, the ITSM system is both a source and a consumer of information on IT assets, so the connection between IT systems is obvious.

IT asset management will not affect the Service Catalog

“Classic” ITIL separates the categorization of IT assets (Configuration Units) and the Service Catalog. On the one hand, this is true, but on the other - obliges to keep 2 reference books:

- IT asset classifier;

- Catalog of Services, in which IT assets are maintained within IT.

Let's see what information is determined by these directories.

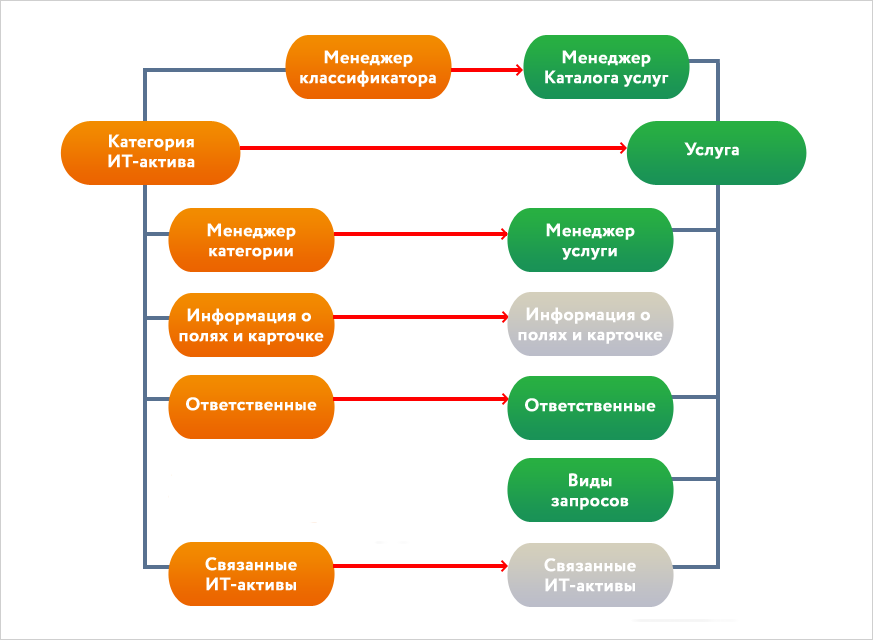

IT asset classifier

Categories contain certain information:

- about the category manager;

- additional fields and appearance of the card;

- responsibility for IT assets;

- related IT assets.

Service Catalog

Services contain information that determines the order of processing requests:

- service manager;

- responsible for requests;

- types of requests available for registration.

')

Remove extra entities

We apply the principle of "Occam's razor", we put out of the brackets the excess and reduce the number of control entities. As a result, it is possible to opt out of the directory of categories.

If we consider some category of IT assets, someone must support it, i.e. provide service inside IT. Information that is maintained in relation to the Service can be supplemented with the missing attributes and get a single entity, the Service-Category.

Why do you need it

Such an approach will add an additional check on the completeness of the Service Catalog and make you more attentive to the categorization of IT assets.

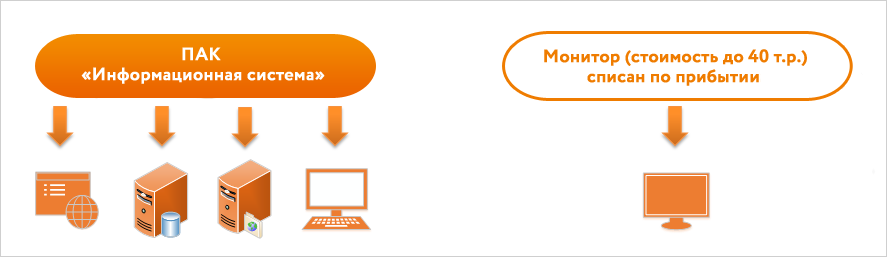

IT asset and Fixed asset identical concepts

It is difficult to agree with this thesis, since An IT asset contains an account of those entities that may not be accounted for in accounting. Therefore, the right step is to reach an agreement at the start of the project and select the primary source of information about IT assets: an IT asset accounting system or an accounting system. Then it is imperative to organize the process of matching Fixed Assets (as well as intangible assets and low valuations) and IT assets.

Why it is impossible to load Fixed assets and compare them one to one with IT assets? Because otherwise, instead of IT assets, we’ll get another product range reference book.

The correct scheme is to separate the entities of the IT asset and the Fixed Assets and bundle them together to further obtain useful information from accounting systems (for example, the costs of Fixed Assets).

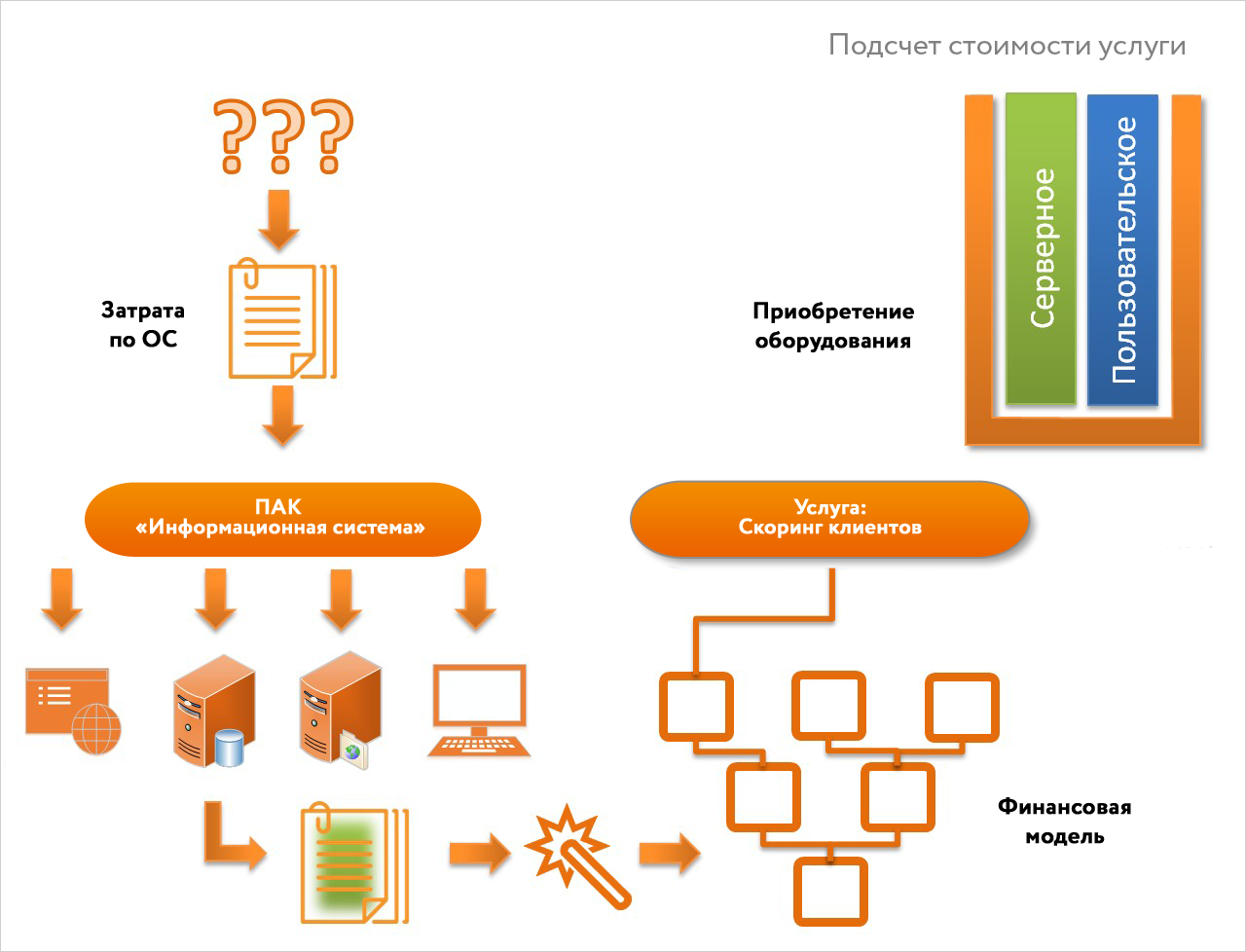

Information on service costs can be automatically accumulated.

Project experience shows that fully automating the collection of information on the costs of IT services can be very expensive. For example, you may need a special employee in the state who will be engaged in the actualization of the resource-financial model. What is more effective in the end: full automation and manual updating of the model or partially manual accounting is a matter of a specific project.

What will be required to fully automate the process of cost accounting for the Service?

| Accounting area | How to automate |

Source of IT asset cost data | Integration with the accounting system:

|

Attribution costs for services | Building a resource-service model:

Building a resource-financial model:

Implementation of the process of maintaining a resource-financial model:

|

As you can see, this is a fairly serious amount of work, the effectiveness of which starts from a certain (rather large) scale.

Subtotals

Resistance to IT myths, incl. Elimination of an erroneous understanding of certain issues or processes in the management of IT assets on the part of the client is an integral part of the implementer's work.

Today we “opened up” and challenged only a part of the IT myths:

- Relevance of data on IT assets is not achieved only due to automatic inventory. It will take a "manual" donation.

- A bundle of IT assets and ITSM systems is required.

- True when IT asset management helps expand the Service Catalog.

- IT asset and Fixed asset are not identical.

- Automating the collection of information on the costs of IT services in full will require significant investments.

Next time I will review other common myths in the field of automating IT asset management processes, and show you how to work with them.

Source: https://habr.com/ru/post/352028/

All Articles