Fintech Digest: blockchain legalization, reduction of branches in favor of IT

Fintech hello reader!

The outgoing week was full of news related to cryptocurrencies. As bitcoin companions won back the January losses, banks around the world imposed bans on buying credit card cryptocurrencies. The wave of prohibitions reached as far as the kangaroo's homeland, where the Commonwealth Bank of Australia recently noted . Since the beginning of the year, Lloyds, Bank of Scotland, Halifax, MBNA, Bank of America, Citigroup, Capital One, Discover, JP Morgan and Virgin Money have been added to the list of fighters with investments in bitcoin.

')

It should be clarified that you can not buy only credit cards, and if you attend to the release of a debit card, you can safely spend at least all the money in the account. But the problem is that a significant part of the clients of Western banks have never had such a card. Debit if there are, then unnamed and are issued by organizations as an alternative to cash. Therefore, the introduction to the world of cryptocurrency turns into a rather intricate quest that an unprepared person can not pass. And prepared bypass any banking obstacles.

Meanwhile, the Polish central bank caught on the order of video bloggers videos , discrediting investment in the crypt. The local star Youtube received for one, as it is now fashionable to say, the integration of 30 thousand dollars. In the video, a scene plays out, as a young man loses absolutely everything because of a cursed bitcoin, and cannot even pay for dinner at a restaurant, shaming before a girl. It would be funny to find out if the blogger has invested the entire fee in something like XRP.

At the beginning of 2018, one after another, the reports of Western banks about the very successful results of 2017 came out. So, Wells Fargo reported a 17% increase in net profit in the fourth quarter, while Lloyds had an increase of 24% (before taxes) and the rest of the big business, in general, did not lag behind either. And synchronously with vigorous reports, the next program of staff reduction and branches was announced. The same Wells Fargo promised to close as many as 900 offices by 2020.

In Europe, it is more difficult to cut people off, because trade unions are actively opposing this. It is even a bit strange when a bank saved by public funds by a miracle genuinely wants to cut costs, but it is not allowed. And yet, the earned directive PSD2 , forcing banks to give out the API of their services, suggests quite unambiguous thoughts. No, banks will not go anywhere, but the day will come when customers will not even know which one they are currently using.

Bank aggregators can be just as commonplace as taxi aggregators. To earn commissions without spending power on attracting customers - isn't this a dream? Yes, and people need much less ... In general, according to incoming data , Lloyds will invest £ 3 billion in its digital infrastructure in the next three years, while hoping to cut spending by $ 8 billion by 2020. This is, of course, in addition to the existing IT costs. The sum of the latter has not been disclosed, but we know that business colleagues at Deutsche Bank spend on IT 4.1 billion euros per year, and JP Morgan Chase 7.4 billion dollars.

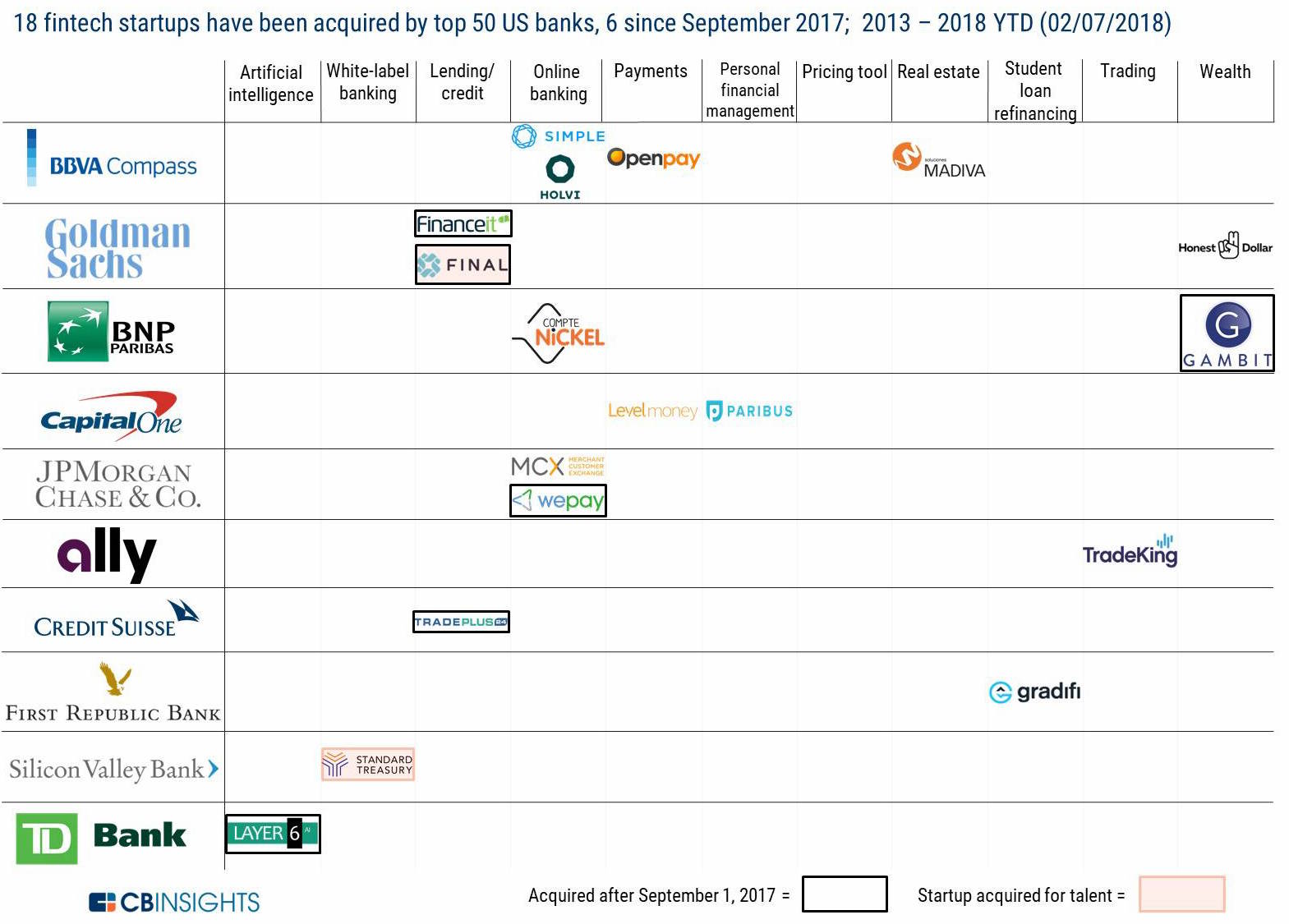

The cost of purchasing fintech startups is also increasing. Recently, a study was published, according to which the largest US banks have bought only 18 startups since 2013.

CB Insights

But 6 purchases fell on the last six months. The reason, I think, is simple: banks began to realize that there was simply no time to leisurely create their own factories of digital ideas. Yes, banks are becoming IT companies, but the giants who were them initially do not hide the desire to manage the money of their users. Therefore, the only possible option is to buy ideas together with their creators. And by the way, this is not only in the States. In our country, there are absolutely similar processes.

How many times have the world been told that blockchain is ideal for storing sensitive information, and smart contracts are an excellent business tool. The only problem is that the state, which seems to be unnecessary with the widespread use of the blockchain, cannot consider these technologies within the legal field. That is terribly cool to make a deal to buy property in the blockchain, but then you still have to duplicate the traditional way.

In the free state of California, bill number 2658 is filed, which contains a quiet revolution. If the bill passes, the entry in the blockchain will be equated to an electronic entry, and the electronic signature protected by the blockchain, from the point of view of the law, will become a regular electronic signature. And, probably the most important thing is that a smart contract is equal to a simple contract.

Interestingly, this is not the first initiative of local lawmakers, just California is a landmark place. An inquisitive researcher will quickly find out that a similar bill was filed in Florida a month ago, and in Arizona blockchain entries and smart contracts were legalized last year.

That's the way it will happen. First parallel walking, then the final move. No one seems to be seriously vouching for the future of cryptocurrencies on the blockchain, but the technology itself is omnipotent because it is true. Poor, poor notaries.

The outgoing week was full of news related to cryptocurrencies. As bitcoin companions won back the January losses, banks around the world imposed bans on buying credit card cryptocurrencies. The wave of prohibitions reached as far as the kangaroo's homeland, where the Commonwealth Bank of Australia recently noted . Since the beginning of the year, Lloyds, Bank of Scotland, Halifax, MBNA, Bank of America, Citigroup, Capital One, Discover, JP Morgan and Virgin Money have been added to the list of fighters with investments in bitcoin.

')

It should be clarified that you can not buy only credit cards, and if you attend to the release of a debit card, you can safely spend at least all the money in the account. But the problem is that a significant part of the clients of Western banks have never had such a card. Debit if there are, then unnamed and are issued by organizations as an alternative to cash. Therefore, the introduction to the world of cryptocurrency turns into a rather intricate quest that an unprepared person can not pass. And prepared bypass any banking obstacles.

Meanwhile, the Polish central bank caught on the order of video bloggers videos , discrediting investment in the crypt. The local star Youtube received for one, as it is now fashionable to say, the integration of 30 thousand dollars. In the video, a scene plays out, as a young man loses absolutely everything because of a cursed bitcoin, and cannot even pay for dinner at a restaurant, shaming before a girl. It would be funny to find out if the blogger has invested the entire fee in something like XRP.

Banks cut branches and employees, but increase IT costs

At the beginning of 2018, one after another, the reports of Western banks about the very successful results of 2017 came out. So, Wells Fargo reported a 17% increase in net profit in the fourth quarter, while Lloyds had an increase of 24% (before taxes) and the rest of the big business, in general, did not lag behind either. And synchronously with vigorous reports, the next program of staff reduction and branches was announced. The same Wells Fargo promised to close as many as 900 offices by 2020.

In Europe, it is more difficult to cut people off, because trade unions are actively opposing this. It is even a bit strange when a bank saved by public funds by a miracle genuinely wants to cut costs, but it is not allowed. And yet, the earned directive PSD2 , forcing banks to give out the API of their services, suggests quite unambiguous thoughts. No, banks will not go anywhere, but the day will come when customers will not even know which one they are currently using.

Bank aggregators can be just as commonplace as taxi aggregators. To earn commissions without spending power on attracting customers - isn't this a dream? Yes, and people need much less ... In general, according to incoming data , Lloyds will invest £ 3 billion in its digital infrastructure in the next three years, while hoping to cut spending by $ 8 billion by 2020. This is, of course, in addition to the existing IT costs. The sum of the latter has not been disclosed, but we know that business colleagues at Deutsche Bank spend on IT 4.1 billion euros per year, and JP Morgan Chase 7.4 billion dollars.

The cost of purchasing fintech startups is also increasing. Recently, a study was published, according to which the largest US banks have bought only 18 startups since 2013.

CB Insights

But 6 purchases fell on the last six months. The reason, I think, is simple: banks began to realize that there was simply no time to leisurely create their own factories of digital ideas. Yes, banks are becoming IT companies, but the giants who were them initially do not hide the desire to manage the money of their users. Therefore, the only possible option is to buy ideas together with their creators. And by the way, this is not only in the States. In our country, there are absolutely similar processes.

Legalization of blockchain

How many times have the world been told that blockchain is ideal for storing sensitive information, and smart contracts are an excellent business tool. The only problem is that the state, which seems to be unnecessary with the widespread use of the blockchain, cannot consider these technologies within the legal field. That is terribly cool to make a deal to buy property in the blockchain, but then you still have to duplicate the traditional way.

In the free state of California, bill number 2658 is filed, which contains a quiet revolution. If the bill passes, the entry in the blockchain will be equated to an electronic entry, and the electronic signature protected by the blockchain, from the point of view of the law, will become a regular electronic signature. And, probably the most important thing is that a smart contract is equal to a simple contract.

Interestingly, this is not the first initiative of local lawmakers, just California is a landmark place. An inquisitive researcher will quickly find out that a similar bill was filed in Florida a month ago, and in Arizona blockchain entries and smart contracts were legalized last year.

That's the way it will happen. First parallel walking, then the final move. No one seems to be seriously vouching for the future of cryptocurrencies on the blockchain, but the technology itself is omnipotent because it is true. Poor, poor notaries.

Source: https://habr.com/ru/post/349694/

All Articles