Mathematical model of financial market dynamics

Introduction

Changes in the exchange rate in the financial market affect the prices of goods and services. Therefore, it is important to know the period of time through which prices will begin to react to a change in the exchange rate.

The complexity of solving this problem consists in a large number of factors affecting the change in the exchange rate [1]. An effective way to weed out a number of secondary factors to determine the main market trends is the use of a Wiener Hopf “white” filter [2,3].

It is clear that only the application of the filter does not solve all the problems of analyzing the impact of exchange rates on the financial market, however, as one of the analysis tools, it is certainly interesting. In addition, using the example of such a filter, one can determine the coefficients of the differential equation of the financial market.

')

Formulation of the problem

On the basis of data on currency fluctuations using correlation analysis and the Wiener Hopf system of equations, construct a dynamic model of the financial market with the help of which it is possible to determine time intervals of price response to a change in the exchange rate.

Determine the autocorrelation function Rx (τ) of the first set of X data on currency fluctuations and plot it

I am listing the solution to this problem using Python tools:

import matplotlib.pyplot as plt from sympy import * from numpy import (zeros,arange,ones,matrix,linalg,linspace) X=[797.17, 797.25, 797.15, 797.23, 797.15, 797.08, 797.05, 797.04, 797.14, 797.14, 797.1, 797.1, 797.11, 797.11, 797.11, 797.11, 797.11, 797.1, 797.1, 797.1, 797.12, 797.12, 797.12, 797.12, 797.12, 797.12, 797.1, 797.08] n=len(X) m=int(n/4) Xsr=sum([w for w in X])/n Dx=sum([(X[i]-Xsr)**2 for i in arange(0,n,1)])/(n-1) Rxm=sum([(X[i]-Xsr)*(X[i+m]-Xsr) for i in arange(0,nm,1)])/((nm)*Dx) def fRxm(m): return sum([(X[i]-Xsr)*(X[i+m]-Xsr) for i in arange(0,nm,1)])/((nm)*Dx) ym=[fRxm(m) for m in arange(0,m+1)] xm=list(arange(0,m+1,1)) M=zeros([1,m+1]) for i in arange(0,m+1,1): M[0,i]=fRxm(i) plt.figure() plt.title(' Rx (τ). ') plt.ylabel('Rx (τ) ') plt.xlabel(' -m ') plt.plot(xm, ym, 'r') plt.grid(True) We get:

Here

- the time interval (offset) between the values of the random process x (t) corresponding to the value R (m) of the autocorrelation function.

- the time interval (offset) between the values of the random process x (t) corresponding to the value R (m) of the autocorrelation function.For values of Rx (τ), x (t) values in the range 0.7 <= Rx (k) <= 1 are closely related statistically to each other. In other words, the values separated from each other for a period of time affect each other significantly.

For values of Rx (τ) being in the range 0.4 <= Rx (k) <0.7, the values of x (t) have an average statistical relationship. This means that the values are separated by a period of time.

influence each other, but this influence can be predicted with a significant error.

influence each other, but this influence can be predicted with a significant error.For values of Rx (τ) being in the range 0. <= Rx (k) <0.4, the values of x (t) have a weak statistical relationship and their interrelation can be neglected.

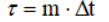

Calculate the mutually correlation function Rxy (τ) of the first set of X and the second set of Y data, plot its graph

I provide a listing fragment to solve this problem in Python:

Y=[577.59, 622.61, 602.23, 554.64, 567.67, 635.47, 608.27, 620.82, 561.73, 639.0, 550.1, 609.31, 640.45, 611.92, 579.33, 552.04, 597.73, 553.4, 605.72, 647.94, 602.26, 610.99, 575.95, 638.99, 631.86, 589.89, 608.17, 619.26] n=len(Y) m=int(n/4) Ysr=sum([w for w in Y])/n Dy=sum([(Y[i]-Ysr)**2 for i in arange(0,n,1)])/(n-1) Rxy=sum([(X[i]-Xsr)*(Y[i+m]-Ysr) for i in arange(0,nm,1)])/((nm)*Dx**0.5*Dy**0.5) def fRxy(m): return sum([(X[i]-Xsr)*(Y[i+m]-Ysr) for i in arange(0,nm,1)])/((nm)*Dx**0.5*Dy**0.5) xy=[fRxy(m) for m in arange(0,m+1)] plt.figure() plt.title(' Rxy (τ). ') plt.ylabel('Rxy (τ) ') plt.xlabel(' -m ') plt.plot(xm, xy, 'r') plt.grid(True) We get:

The lag or economic lag of the market τ0 is determined by the maximum of the mutual correlation function Rxy . On the chart. the maximum of the function Rxy (m) corresponds to m = 4 . Consequently, the change in the exchange rate will affect the change in the price of goods after a period of time equal = 4 * 1 day = 4 days . That is, in three days the price of this product will change due to a change in the exchange rate (dollar).

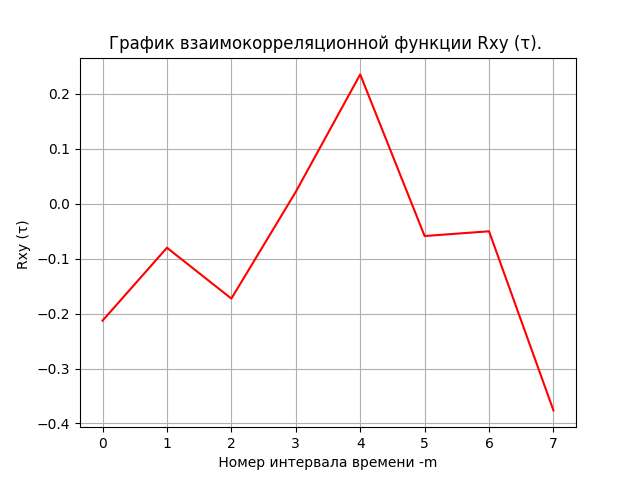

Solve the system of Wiener-Hopf equations and plot the impulse transition function h (t)

Here is a listing fragment to solve this problem in Python:

Wiener-Hopf solution of the system of equations by the algebraic method

P=zeros([m,1]) for i in arange(0,m,1): P[i,0]=fRxy(i) Q=zeros([7,7]) for i in arange(0,7,1): Q[0,i]=M[0,i+1] Q[1,i]=M[0,i] for i in arange(0,6,1): Q[2,i+1]=M[0,i] Q[2,0]=M[0,1] for i in arange(0,5,1): Q[3,i+2]=M[0,i] Q[3,1]=M[0,1] Q[3,0]=M[0,2] for i in arange(0,4,1): Q[4,i+3]=M[0,i] Q[4,0]=M[0,3] Q[4,1]=M[0,2] Q[4,2]=M[0,1] for i in arange(0,3,1): Q[5,i+4]=M[0,i] Q[5,0]=M[0,4] Q[5,1]=M[0,3] Q[5,2]=M[0,2] Q[5,3]=M[0,1] for i in arange(0,2,1): Q[6,i+5]=M[0,i] Q[6,0]=M[0,5] Q[6,1]=M[0,4] Q[6,2]=M[0,3] Q[6,3]=M[0,2] Q[6,4]=M[0,1] H=linalg.solve(Q, P) hxy=[H[m] for m in arange(0,int(m),1)] xm=list(arange(1,m+1,1)) plt.figure() plt.title(' h(t)') plt.ylabel('H ') plt.xlabel(' -i ') plt.plot(xm, hxy, 'r') plt.grid(True) We get:

With a decrease in the exchange rate of two identical impulses and a decline. For analysis, it is necessary to obtain a transition function and determine the coefficients of the differential equation of the market, the solution of which will confirm the general trend.

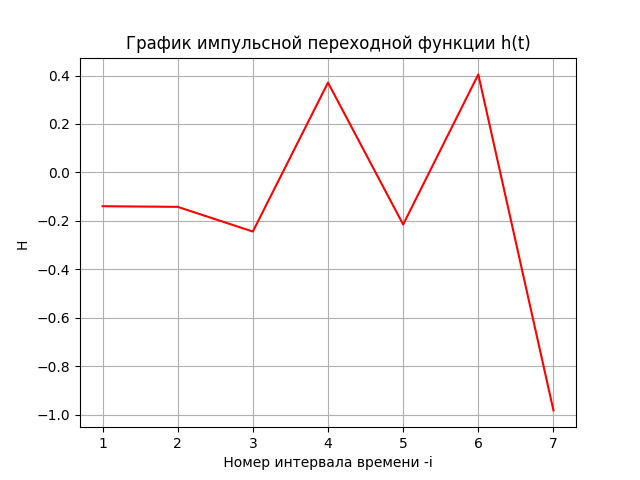

Build a transition function from the found solution of the Wiener-Hopf system of equations, and obtain the financial market differential equation

Here is a listing fragment to solve this problem in Python:

Construction of the transition characteristics and the differential equation of the financial market

s1=H[0,0]/2 s2=(H[0,0]+H[1,0])/2 s3=(H[1,0]+H[2,0])/2 s4=(H[2,0]+H[3,0])/2 s5=(H[3,0]+H[4,0])/2 s6=(H[4,0]+H[5,0])/2 s7=(H[5,0]+H[6,0])/2 N=zeros([8,1]) N[0,0]=0 N[1,0]=s1 N[2,0]=N[1,0]+s2 N[3,0]=N[2,0]+s3 N[4,0]=N[3,0]+s4 N[5,0]=N[4,0]+s5 N[6,0]=N[5,0]+s6 N[7,0]=N[6,0]+s7 nxy=[N[i,0] for i in arange(0,m,1)] xm=[i for i in arange(0,m,1)] plt.figure() plt.plot(xm, nxy,color='r', linewidth=3, label=' -') var('t C1 C2') u = Function("u")(t) de = Eq(u.diff(t, t) +0.3*u.diff(t) + u, -0.24) print(de) des = dsolve(de,u) eq1=des.rhs.subs(t,0) eq2=des.rhs.diff(t).subs(t,0) seq=solve([eq1,eq2],C1,C2) rez=des.rhs.subs([(C1,seq[C1]),(C2,seq[C2])]) g= lambdify(t, rez, "numpy") t= linspace(0,7,100) plt.title(' ') plt.xlabel(' () ') plt.ylabel('y(t), N') plt.plot(t,g(t),color='b', linewidth=3, label=' ') plt.legend(loc='best') plt.grid(True) plt.show() We get:

Differential equation of the financial market:

Eq (u (t) + 0.3 * Derivative (u (t), t) + Derivative (u (t), t, t), -0.24).

At the considered time interval, the financial market can be represented by an oscillatory link of the second order, which corresponds to the increasing periodic price fluctuations with an increase in the exchange rate and a restrained periodic fluctuation in prices for a decrease in the exchange rate.

Full listing of the program

import matplotlib.pyplot as plt from sympy import * from numpy import (zeros,arange,ones,matrix,linalg,linspace) " Rx (τ) . " X=[797.17, 797.25, 797.15, 797.23, 797.15, 797.08, 797.05, 797.04, 797.14, 797.14, 797.1, 797.1, 797.11, 797.11, 797.11, 797.11, 797.11, 797.1, 797.1, 797.1, 797.12, 797.12, 797.12, 797.12, 797.12, 797.12, 797.1, 797.08] n=len(X) m=int(n/4) Xsr=sum([w for w in X])/n Dx=sum([(X[i]-Xsr)**2 for i in arange(0,n,1)])/(n-1) Rxm=sum([(X[i]-Xsr)*(X[i+m]-Xsr) for i in arange(0,nm,1)])/((nm)*Dx) def fRxm(m): return sum([(X[i]-Xsr)*(X[i+m]-Xsr) for i in arange(0,nm,1)])/((nm)*Dx) ym=[fRxm(m) for m in arange(0,m+1)] xm=list(arange(0,m+1,1)) M=zeros([1,m+1]) for i in arange(0,m+1,1): M[0,i]=fRxm(i) plt.figure() plt.title(' Rx (τ). ') plt.ylabel('Rx (τ) ') plt.xlabel(' -m ') plt.plot(xm, ym, 'r') plt.grid(True) " Rxy (τ) X Y , " Y=[577.59, 622.61, 602.23, 554.64, 567.67, 635.47, 608.27, 620.82, 561.73, 639.0, 550.1, 609.31, 640.45, 611.92, 579.33, 552.04, 597.73, 553.4, 605.72, 647.94, 602.26, 610.99, 575.95, 638.99, 631.86, 589.89, 608.17, 619.26] n=len(Y) m=int(n/4) Ysr=sum([w for w in Y])/n Dy=sum([(Y[i]-Ysr)**2 for i in arange(0,n,1)])/(n-1) Rxy=sum([(X[i]-Xsr)*(Y[i+m]-Ysr) for i in arange(0,nm,1)])/((nm)*Dx**0.5*Dy**0.5) def fRxy(m): return sum([(X[i]-Xsr)*(Y[i+m]-Ysr) for i in arange(0,nm,1)])/((nm)*Dx**0.5*Dy**0.5) xy=[fRxy(m) for m in arange(0,m+1)] plt.figure() plt.title(' Rxy (τ). ') plt.ylabel('Rxy (τ) ') plt.xlabel(' -m ') plt.plot(xm, xy, 'r') plt.grid(True) """ -.""" P=zeros([m,1]) for i in arange(0,m,1): P[i,0]=fRxy(i) Q=zeros([7,7]) for i in arange(0,7,1): Q[0,i]=M[0,i+1] Q[1,i]=M[0,i] for i in arange(0,6,1): Q[2,i+1]=M[0,i] Q[2,0]=M[0,1] for i in arange(0,5,1): Q[3,i+2]=M[0,i] Q[3,1]=M[0,1] Q[3,0]=M[0,2] for i in arange(0,4,1): Q[4,i+3]=M[0,i] Q[4,0]=M[0,3] Q[4,1]=M[0,2] Q[4,2]=M[0,1] for i in arange(0,3,1): Q[5,i+4]=M[0,i] Q[5,0]=M[0,4] Q[5,1]=M[0,3] Q[5,2]=M[0,2] Q[5,3]=M[0,1] for i in arange(0,2,1): Q[6,i+5]=M[0,i] Q[6,0]=M[0,5] Q[6,1]=M[0,4] Q[6,2]=M[0,3] Q[6,3]=M[0,2] Q[6,4]=M[0,1] H=linalg.solve(Q, P) hxy=[H[m] for m in arange(0,int(m),1)] xm=list(arange(1,m+1,1)) plt.figure() plt.title(' h(t)') plt.ylabel('H ') plt.xlabel(' -i ') plt.plot(xm, hxy, 'r') plt.grid(True) s1=H[0,0]/2 s2=(H[0,0]+H[1,0])/2 s3=(H[1,0]+H[2,0])/2 s4=(H[2,0]+H[3,0])/2 s5=(H[3,0]+H[4,0])/2 s6=(H[4,0]+H[5,0])/2 s7=(H[5,0]+H[6,0])/2 N=zeros([8,1]) N[0,0]=0 N[1,0]=s1 N[2,0]=N[1,0]+s2 N[3,0]=N[2,0]+s3 N[4,0]=N[3,0]+s4 N[5,0]=N[4,0]+s5 N[6,0]=N[5,0]+s6 N[7,0]=N[6,0]+s7 nxy=[N[i,0] for i in arange(0,m,1)] xm=[i for i in arange(0,m,1)] plt.figure() plt.plot(xm, nxy,color='r', linewidth=3, label=' -') var('t C1 C2') u = Function("u")(t) de = Eq(u.diff(t, t) +0.3*u.diff(t) +u, -0.24) print(de) des = dsolve(de,u) eq1=des.rhs.subs(t,0) eq2=des.rhs.diff(t).subs(t,0) seq=solve([eq1,eq2],C1,C2) rez=des.rhs.subs([(C1,seq[C1]),(C2,seq[C2])]) g= lambdify(t, rez, "numpy") t= linspace(0,7,100) plt.title(' ') plt.xlabel(' () ') plt.ylabel('y(t), N') plt.plot(t,g(t),color='b', linewidth=3, label=' ') plt.legend(loc='best') plt.grid(True) plt.show() Findings:

Using the high-level programming language Python using correlation analysis and the Wiener Hopf white filter, an accessible tool for analyzing the dynamics of the financial market has been obtained.

Thank you all for your attention!

References:

Source: https://habr.com/ru/post/341268/

All Articles