XBRL: Just About the Difficult - Chapter 1. Introduction

Comment from the translator

In 2015, the Central Bank of the Russian Federation launched a project for the transition of non-credit financial institutions (NFO) to electronic format for presenting reporting data in XBRL format from 01/01/2018. The deadlines are already coming, and the NFO is only beginning to realize the scale of the coming changes. There are very few quality materials about XBRL in Russian (I can only recommend the XBRL book for teapots , the translation of which was initiated by the Central Bank, though it was not done in the best possible way). I want to fill this gap and bring to your attention my adaptation of a good XBRL in Plain English brochure from Batavia , which talks about the basics of XBRL.

I translate on behalf of the author, I supplement the text with useful links. I try to adhere to the terminology of the Central Bank of the Russian Federation with reference to the original terms. I'll start with the first chapters, and if the topic is interesting for you, I will complete the translation. Comment, ask questions - I'll tell you everything I know.

Roman Udaltsov

1. Introduction

This chapter introduces the book itself and the basic concepts of XBRL.

1.1. What to expect

If you started reading this book, it means you have already heard about the new way of forming business reporting - XBRL. If you took a look at the XBRL specification , you know that it is a 158-page document full of formal definitions. Such a document is necessary for the correct definition of XBRL. It can be considered a relaxing reading at night for mathematicians. But not for us, normal people.

For us, normal people, this book conveys the essence of the XBRL specification in simple Russian. It should give you a good understanding of what XBRL is and how it can be used. Basically, the book focuses on the XBRL functionality provided in the specification.

You do not immerse yourself in the smallest details by reading this book. If you need this level of understanding, for example. if you want to write your own XBRL validation software, you should carefully study the formal specification. But anyway, this book will certainly serve as an introduction to the exciting world of XBRL.

Such blocks will denote a deeper immersion in details (where it is really necessary).

I also will not discuss on such basic technical standards as XML, XML Schema, XLink, XPath, XPointer, etc. If you are not very familiar with these technologies, take a look at the World Wide Web Consortium's W3C website for a list of recommended literature or any good book on XML.

This book is based on the XBRL 2.1 specification dated 02/20/2013 with corrections dated 04.25.2005. If suddenly there are discrepancies between the book and the official specification, modesty requires me to assume that I was wrong, and the authors of the specification did everything right. I would recommend you make a similar assumption.

In the absence of rich formatting capabilities in Markdown and HFM , examples will be indicated in the same blocks.

1.2. I present to you XBRL

XRBL stands for E x tensible B usiness R eporting L anguage (extensible business reporting language), which in itself describes the essence well: it is a reporting language used in business. And it is expandable. It's simple, yes? Well, maybe a little more explanation is required.

This chapter introduces some XBRL related terms that will appear in bold. In the following chapters, we will analyze everything in detail, so do not be intimidated by them.

Let's jump right into the middle: ... B usiness R eporting ...

1.2.1. Business Reporting

We all know that business forms a bunch of statements:

- tax returns

- annual reports

- internal sales figures

- ...

Each report is data representing a set of facts about the report content, such as:

- reporting period

- annual income

- number of clients

- number of sales

- inventory numbers

- ...

In the good old days, such reports were created by collecting all relevant facts and filling them in pre-printed paper forms. Then the completed form was sent to interested persons who read the facts from the form.

It sounds cumbersome, but the way it is. Further - worse ... Different stakeholders require data in different forms, while the facts contained in them may be the same. For this, the report writer has to fill in the same facts in different forms.

XBRL offers a way to improve the process of creating, distributing, and using data in business reports. It defines an electronic reporting format that allows computers to automatically create, validate, and process reporting. It also determines the way to ensure a single semantic meaning of the transferred business facts. The compiler of the report could simply make one report with all the facts and pass it on to the recipient, who would select the facts he needs and present in any form convenient to him. The definition of a single semantic value of the facts ensures that each recipient of the report interprets the facts obtained in the same way.

Another interesting point is the possibility of separating the report form and its content. The pre - defined form of the report is a template that determines the composition of the facts. It is created by the recipient of the report once. And the facts that are transmitted are the content that is created each time a report is generated.

The XBRL standard also uses a similar division:

- The definition of what should or can be contained in the report is described by the so-called taxonomy (taxonomy) - it defines the concepts in the business sphere for which the reporting is generated.

- The reporting data itself is called an XBRL report (instance document). It contains the facts transmitted to the recipient. The report refers to taxonomy to give facts meaning. Each of the facts within the report is associated with the corresponding concept in the taxonomy.

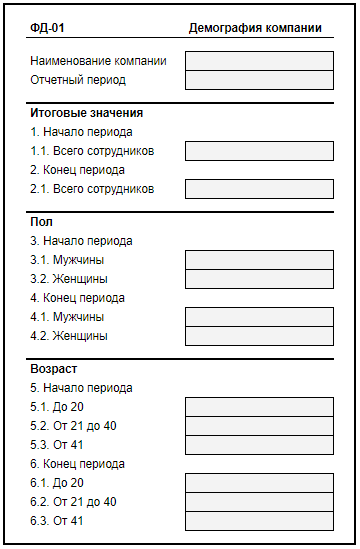

It looks like a good time has come to get acquainted with an example that I will use throughout the book. It illustrates the basic principles of XBRL and shows the technical and formal aspects from a practical point of view. An example consists of a paper form and handwritten data.

The form of the report is as follows:

')

The reporting form can be uniquely identified by its unique identifier FD-01. It consists of the following elements - the name of the company, the reporting period, the number of employees at the beginning and end of the reporting period. Also, it is required to divide the number of employees into men and women and distribute them into several age groups.

An example of a completed report might look like this:

It is easy to see that the number of employees has increased, but at least one person with a lack of mathematical skills works in the company. In such a simple example, it is unlikely that someone will count 27 + 15 as 41, but in more complex reports such errors are very likely, if everything is done manually.

1.2.2. Extensible (Expandable)

Another premise of XBRL is that it is extensible. Returning to the good old days, let's consider a scenario in which extensibility would be useful.

Suppose the European Union defines reporting requirements for any business within the EU.

- This requirement is likely to be in English, but most companies would like to have a reporting form in their own language, since the translation of business terms can be very complex.

- Perhaps in some countries, the government is already putting forward such reporting requirements, and with some additions specific to the country. To avoid the need to prepare two different forms with overlapping requirements, both forms can be combined into a common form for a particular country. But it still requires the creation of a new version of the main form.

XBRL allows you to support such requirements. The EU will create one taxonomy to define reporting requirements. Translation of technical concepts in taxonomy into user-friendly terms is contained in the so-called label base (label linkbase). Each language within the EU can have its own label base or you can create one common base containing labels for each language. Note that the actual concept definition does not need to be repeated for each language.

A country wishing to extend the EU taxonomy will simply create its own taxonomy, which will refer to the EU taxonomy in terms of common concepts. This country will only need to define the specific concepts that are not included in the EU taxonomy.

1.2.3. Language

“L” in XBRL stands for Language. The XBRL language provides a way to express taxonomies and XBRL reports in a single, unambiguous format, which is a necessary requirement for computer processing of information.

The XBRL language is based on world standards such as XML and their corresponding specifications. The following chapters will cover this in more detail.

Chapter navigation

Source: https://habr.com/ru/post/333636/

All Articles