Where is the Internet of Things going?

The term IoT (Internet of Things) appeared quite a long time ago, in the late 90s of the last century. It was invented by marketers in order to promote the RFID technology, which was revolutionary at the time, and the “things” at that time were mostly different goods in warehouses and stores, covered with radio tags. But the term got accustomed, and soon it was “pulled” on practically all M2M (machine-to-machine) communications, including sensors and sensors in traditional SCADA systems.

The next 10 years, from 2000 to 2010, IoT existed in a state of drowsiness, he occupied his small niche, but no one especially produced it. From 2000 to 2010, the mobile boom was actively rolling up, everyone had smartphones, and traffic was growing at a pace that both operators and manufacturers were busy exploring this new market. But then there was the crisis of 2008, there was less money, refinancing became more difficult, and the old growth model began to falter. Far-sighted industry visionaries began to wonder: what will happen after the era of smartphones? Who will lead the industry, where will the main money in mobile communications be in the year, so to say, in 2020?

“My dear, you just need to stay in place.

”

Lewis carroll

And in 2009, Ericsson published a report in which, among other things, among the remaining 100 pages of useful analytics, I mentioned that, actually, by 2020 there will be 50 billion world wide connections of smart devices (read things) to the Internet. Everyone transferred it to money, licked it off, and somehow immediately liked the idea. The Internet of Things was woken up, dust shaken off and pulled back onto the platform with the words: “Meet our future! Soon there will be the main flow of money in mobile communications. ”

')

Indeed, if one soberly assesses the prospects of the industry, then there are two facts:

- telecom operators are increasingly turning into an effective “pipe” for transmitting data that does not belong to them;

- The main vector of development of the industry lies in the field of intellectual services, and the main money is spinning today there, and not in the "pipes".

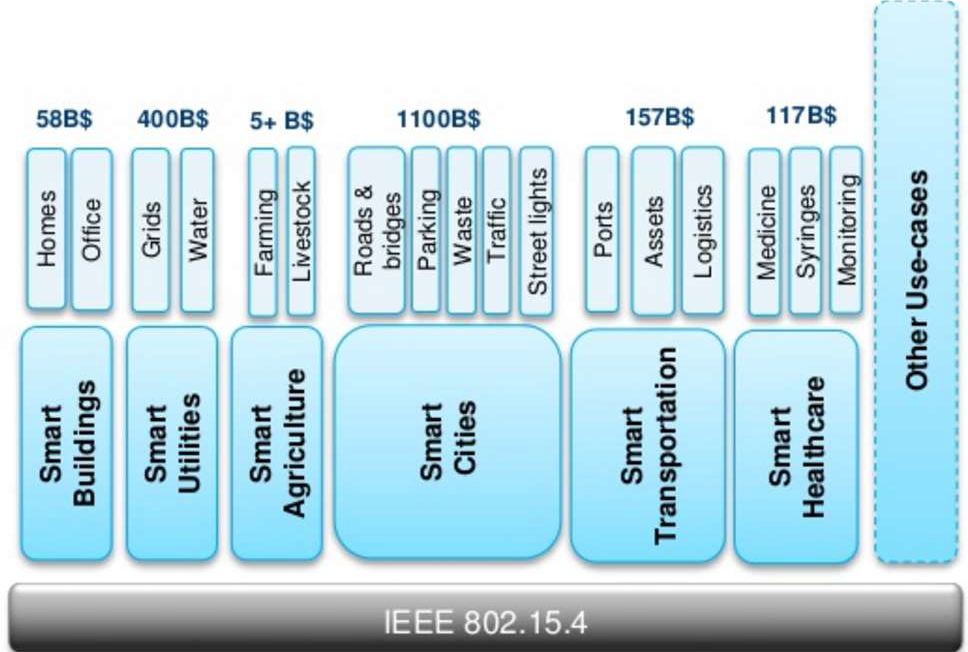

And the operators would really like to touch this money, especially since voice services, their main “money generator”, quickly begin to “eat up” various nimble guys from Facebook (with their WhatsApp), Google, etc. Internet of things in this sense looks promising. Based on it, you can create a huge number of different services. Here you’ll have smart buildings and offices, which they themselves order their favorite coffee and adjust the climate in the workplace as you like, and smart construction management, when concrete arrives at the right object on time, and traffic control, and smart farming, and smart safe cities, and housing and public utilities, and health care, and ... In general, almost any area of human life can potentially be made smart and make money from it. And everyone in the industry likes it.

Figure 1. Estimates of the contribution of IoT to the industry

Figure 1 shows a rough estimate of how much money approximately the money can bring to the industry of the "internetization" of things. If we consider that the entire IT market today weighs about $ 3.5 trillion, and the communications market weighs about $ 1.5 trillion, then even according to this modest estimate, the Internet of things is expected to at least double this money.

But these are lyrics, let us now descend closer to the ground and try to understand why in the 5 years that IoT have been actively producing, it still does not grow by leaps and bounds and has not withdrawn from the market any substantial part of the money indicated in Figure 1. In our opinion, there are two types of problems that do not yet allow the Internet of things to develop very quickly, technical and ideological. We will talk about technical problems a bit later, but now a few words about more fundamental difficulties - ideological.

The fact is that, despite the large information flow through all marketing channels about the Internet of Things, the main business model through which this market should operate is still not completely clear. All conversations that are heard about monetization of IoT are reduced either to the idea of taking money for traffic at special rates, or taking money for the fact of connecting the sensor to the infrastructure, or taking money for a service that is built on the basis of IoT. Since The main engine of IoT today is still communication operators, it seems that the easiest option for them is to work “in the old way”, i.e. take money for traffic or for connecting IoT sensors to the network. But in this case the question arises: how much does it cost to install, authenticate and conduct this sensor for all operator systems? Will it have a SIM card? Or will it be pre-provisioned at the factory? How much will it cost to simply screw to the system and check the sensor for operation? How much will the billing of such a sensor cost? In the end, if you count the business case, it turns out that with the current business model, the IoT story begins to “float”, according to various estimates, somewhere at $ 30-40 per year ARPU (where U-user is the same sensor, which is connected to the system).

But with such prices no one will massively buy and install sensors! This is the fundamental ideological problem of the Internet of Things today. And until the new IoT service business model is run-in, mass implementation will be slowed down.

“What should be done to make the cow eat less and give more milk? Feed less and milk more. ”

Folk wisdom

What are the options out of this situation now? According to the classics, reduce costs and look for additional income. To minimize costs, it is necessary to simplify the sensors as much as possible, throw out all unnecessary things from them and simplify the processes of their processing in operator systems as much as possible. For example, to take money upfront-ohm for connecting to the IoT service, without reference to the period, for the entire lifetime of the sensor (s). Another part of the story - increasing revenues - is traditionally more difficult for telecom operators. Complicated because operators entail the execution of the non-intrusive function of the Application Provider, where, for example, an intelligent application will be launched in their public cloud to manage specific areas of the national economy (parking lots in the city, utilities, smart buildings, etc.) and leased under certain conditions. Such projects, as a rule, are hard for large operators, although, in fairness, there are successful examples.

But every cloud has a silver lining. Just here and now there is a place for flexible and nimble, who are ready to quickly turn on a small profit and make innovative projects not so much for money, but for interest and perspective.

Now about the technical problems that also prevent the Internet of things from developing rapidly. With technical problems in some ways easier, because it is clear about how they should be solved, and it is possible to more or less accurately predict what the final results may be. Let us briefly list the main difficulties faced by the implementation of IoT projects:

Sensor problems

- Existing things, as a rule, do not have sensors.

- Different interfacing interfaces (ZigBee, 6LoWPAN, PLC, RS-485, Modbus, BACnet, HART, etc.)

- Poor compatibility between different solutions

Communication problems

- A huge number of connections from sensors

- Many different scenarios ( Video Surveillance, Industrial Control, Autopilot, Smart Metering, etc.) applications with different requirements for the application environment with different requirements for the environment

Problems with extracting value from data and monetization

- Deep understanding of the subject area

- Saving and processing data

- Security

All of the above difficulties prevent IoT from running, without the sensors in existing things and compatibility between different protocols, the IoT concept will not work. But there is a problem, without solving which it is fundamentally impossible to move on. This problem is SAFETY. A unified, unified approach to security in the world of the Internet of Things has not yet been developed. All security approaches offered by different companies are based on old principles and do not solve all the problems of the Internet of Things. And if they decide, it becomes so hard and expensive that in the end no one needs. Why is this problem key? Because the very field of application of the Internet of Things is extremely sensitive to security breaches of any type (integrity, confidentiality or accessibility violations). Imagine, for example, that a hacker gained access to a system that collects data and controls pacemakers? Or, for example, hacked the kettle and then turned it on empty ... You can think of a lot of apocalyptic pictures, like the Internet of things is destroying someone’s life or the whole world. We recommend to look at this topic "Black Mirror", the 6th episode of the third season. There, the colors show what can turn into a story that violates the confidentiality and availability of a system with a mass connection of electronic devices. So, when it comes to managing life support systems, the word “SAFETY” should come first.

Another important problem at the interface of technology and ideology of IoT is the problem of extracting useful information from the data that the sensors will transmit. The problem is even, rather, not in the technique of the issue, effective algorithms and data mining techniques have been around for a long time. The question is, WHAT data should be collected and HOW to monetize them later? Actually, this is again a question of the business model, but at a different level - at the application level.

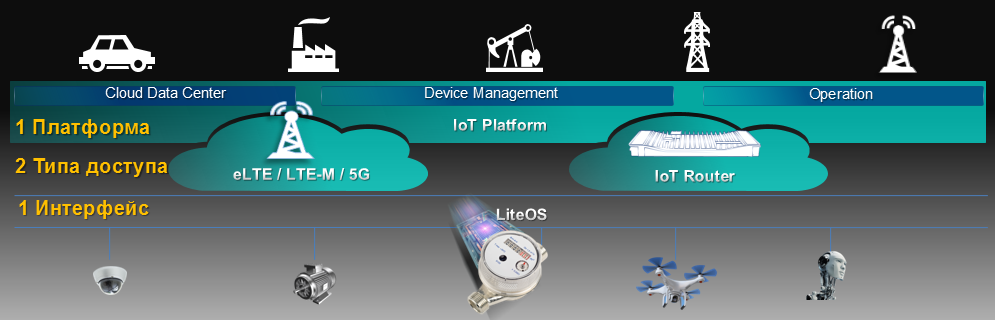

So what does the Internet of things end up with today? What parts does it consist of and who does what in this area? Globally, the Internet of Things consists of three parts: smart sensors, network infrastructure and a platform where information from sensors is processed.

Figure 2. The Internet of Things - of which

The most expensive part of smart sensors is a chip. And in order for the Internet of things to become massive, it is necessary that the chip be as cheap as politeness. According to analysts, the IoT sensor should not cost more than a few dollars, despite the fact that the main weight in the cost of the sensor is the cost of the chip.

In order for the data to "flow" from sensors to the platform, you need a network infrastructure. And the requirements for it are also quite specific. Considering the specifics of the sensors (on average, the need to transmit several hundred bits per minute and 95% of the time in standby mode), the network requires: 1) ultra-low bandwidth; 2) ultra-low overhead to different service protocols. Currently, traditional mobile technologies are poorly designed for this, as they carry too much service overhead. This makes the end devices, firstly, relatively expensive, and secondly, consuming a lot of energy. Therefore, to implement the Internet of things, special technologies have been invented that have a low overhead and allow you to create sensors that consume little energy. Conventionally, according to the distance at which the sensors from the gateway / base station can be located, the technology can be divided into “long” - with a distance to the sensor measured by kilometers, and “short” - with a distance to the sensor of hundreds of meters. And those and other technologies solve problems with the power consumption of sensors, but require fundamentally different approaches to building infrastructure for the Internet of things.

“Everyone is equal, but some are smoother”

J. Orwell

Folk wisdom

Typically, hardware manufacturers focus on different parts of the Internet of things infrastructure or on a specific technology, for example, a specific transport for the Internet of things. In this regard, Huawei differs from other vendors and develops products on all three infrastructural levels of the Internet of things, and it does this on the basis of several different technologies.

The company has developed its own chip, which consumes little energy, is cheap and under which a specialized software platform (LiteOS) is implemented. Huawei has all the infrastructure for collecting and transmitting data from sensors, ranging from mobile networks in all forms to wired technologies like Ethernet and GPON. In addition, Huawei has a platform for collecting, storing and processing big data - the very place where value added is born in the history of the Internet of things.

Fig. 3 Levels of IoT implementation

Let's tell a little more about the second, network level. As mentioned above, at the access infrastructure level there are two actually competing approaches to network implementation — based on “long” or “short” technologies. Option number 1 - use the transport of the mobile operator, which, as mentioned above, implemented a specialized technology (NB-IoT, for example). But with this option, while there are certain questions:

- specialized IoT-transport in mobile networks only starts → while not everywhere and not everyone has;

- The service user is tied to the operator's infrastructure, with an incomprehensible business model for the sales of this service → poorly forecasted operating costs (see above), many fear this.

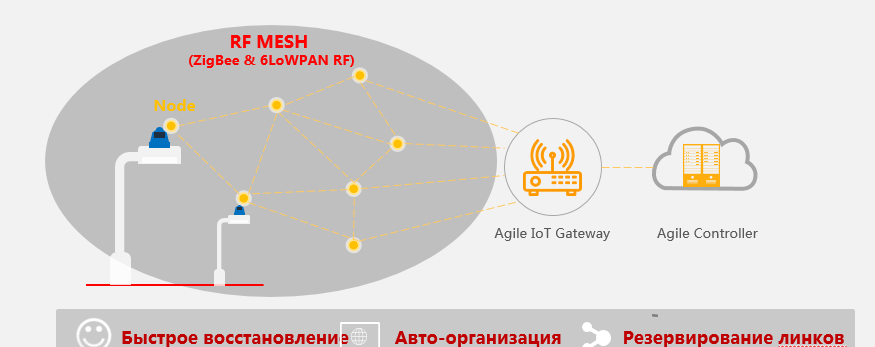

Option number 2 - build your transport infrastructure under IoT without a mobile operator, for example, based on “short” technologies like ZigBee and 6LoWPAN. Such an access infrastructure, “sharpened” for the performance of one particular service, is much easier and simpler than the network of a mobile operator designed for a wide range of services. To implement their transport infrastructure under IoT, two things are needed, by and large:

- a specialized IoT gateway that will take over the connections from the sensors;

- a controller that manages the gateway network and aggregates the information on itself.

Such an infrastructure also works quite simply: the gateway collects data from a specific set of sensors, usually collected in a Mesh network. Further, the collected data through the controller is transmitted to the application, which solves a specialized task, for example, the task of controlling the light in the city. In the opposite direction, everything works in a similar way:

- the application, after processing the data, generates a control signal and transmits it through an open interface to the network controller;

- the network controller through the corresponding gateway sends a signal to the sensor that executes the transmitted command.

Fig. 4. Example: smart light control

Figure 4 shows an example of how a system of intelligent management of urban lighting can be implemented without the participation of a mobile operator. Specialized sensors embedded in LED lighting lamps form local Mesh networks using a special protocol (ZigBee or 6LoWPAN). Each such local Mesh-network is closed at the IoT-gateway, which communicates via the controller with the application that controls the lighting in the city. In the annex, the whole city is marked up into groups of lamps, clearly represented on the map below. The system operators set policies for controlling the light in the city (at what intensity of lighting to turn on the lamps, at what time to turn off, which lamps burn all the dark time, which ones turn off in the dead of night, what intensity should the lighting be at different times of day, etc.). Control policies are loaded through the transport infrastructure into the sensors, and the lighting control in the city follows the rules set by the operators.

What are the advantages of such an implementation? The entire infrastructure does not depend on the specific mobile network operator. The service company itself owns the transport infrastructure, controls all operating expenses and can derive additional profit from it. What are the cons? As usual, the reverse side of the advantages: you need to maintain the transport infrastructure yourself and do it quite professionally. Otherwise, instead of additional flexibility and profit, there will be additional losses.

In conclusion, I would like to emphasize two points:

- the cost of transport infrastructure is a few percent of the total cost of infrastructure projects with the Internet of Things;

- For those who do not want to give IoT-transport to the side of mobile operators and want to build and manage the entire infrastructure of the Internet of Things, today there is a unique "window of opportunity" that closes as soon as all operators launch IoT-transport in their networks and finally determine with a business model of services provided.

Source: https://habr.com/ru/post/317176/

All Articles