IoT market. There are many grades, no consensus

Alexander Prokhorov. Leading Analyst, Huawei Russia, Ph.D.

Today, the technologies of the Internet of Things and the prospects for the development of a market based on these technologies are actively discussed. It is impossible to judge how promising a technology is, how profitable it is to invest in its development, without numerical estimates. And indeed, a considerable number of such assessments and forecasts appeared in the open press from various analytical agencies.

It would seem that sources are enough to make an impression about the size of the market, the prospects for its growth. However, in a more detailed study of the problem, you encounter the fact that with an abundance of assessments between them there is almost no consistency. In the open press, market figures are often given without a description of the data collection method, the definition of the market boundaries, its structure. The scatter in the estimates baffles the reader, reduces the degree of confidence in the data.

For example, according to IDC, spending on the Internet of Things (IoT) in 2014 amounted to $ 655.8 billion and will increase to $ 1.7 trillion in 2020 with a CAGR level of 16.9%. According to Harbor Research, in 2014 the IoT market amounted to $ 180 billion, and by 2020 its volume will exceed $ 1 trillion. According to Machina Research, the size of the IoT market in 2014 amounted to $ 900 billion, and it will grow to $ 4.3 trillion by the end of 2024. According to Strategy Analytics, the aggregate market for all IoT market elements will be $ 150 billion in 2016 and grow up to $ 550 billion by 2025

')

In addition to the multiple differences in estimates, it is noteworthy that the IoT market accounts for a very large share of total ICT expenditures. For example, according to IDC and Gartner estimates, the total expenditure on ICT in 2015 will be about $ 3.5 trillion. How do such optimistic forecasts of IoT market growth come together with moderate ICT market forecasts? This article provides an attempt to explain the reasons for the variation in estimates, to make a comparison in the approaches of different analysts, to help the reader in interpreting the disparate data on the IoT market.

Quantitative evaluation and interpretation of terms

At the beginning of the article, we brought differences in financial market estimates. Indeed, the market can be considered differently, considering or not taking into account different parts of the IT infrastructure, including those or other sets of services for the implementation and maintenance of solutions. But quantitative estimates of the number of connected IoT devices are directly related to the definition of the term IoT itself. Do analysts have a coherent view of this question? How, for example, do they estimate the number of connected IoT devices in the world today and how many will appear by 2020? The IoT Analytics publication provides a comparative analysis of the forecasts of various companies for the number of connected devices in the world by 2020. According to this publication, opinions are clearly divided: Global Insight predicts that there will be 18 billion of such devices; ABI Research and IDC - about 28 billion, Cisco and Ericsson believe that the connected devices will be about 50 billion. It is interesting to note that these analysts not only give different predictions for the long term, but also estimate data for 2014 differently. For example, ABI Research points to a number - 6 billion, Cisco - 14 billion. What is the reason for such different estimates? Perhaps some of the discrepancies arise in the not quite correct use of terms related to IoT. For example, in some publications IoT solutions are referred to as IoT / M2M or the terms M2M and IoT are generally used as synonyms. Sometimes the terms “industrial Internet”, “Internet of people”, “Internet of things”, “Web of things”, “Internet of all” are used without clarifying the boundaries of the concepts introduced.

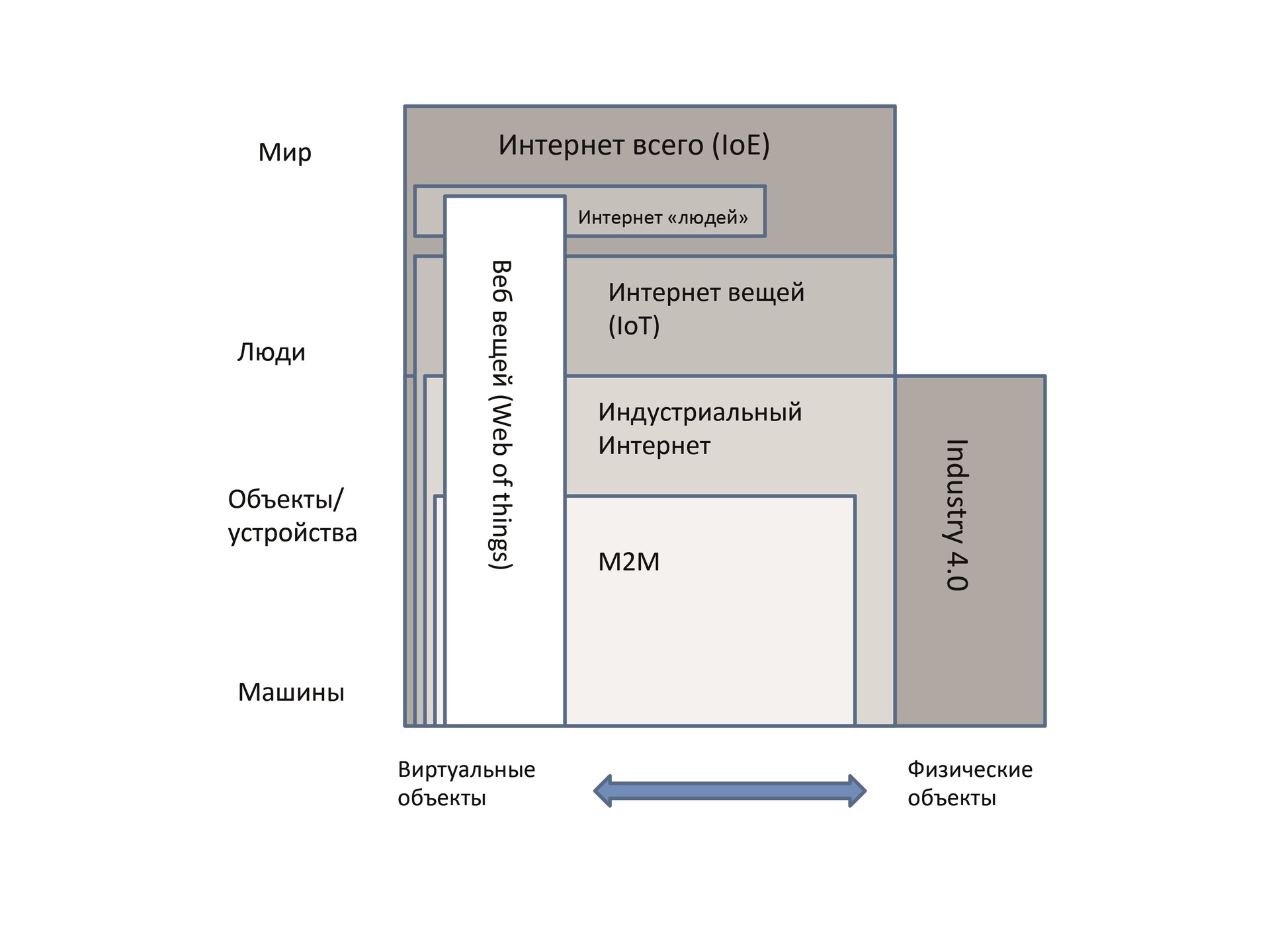

The most obvious distinction between the above terms is given in Figure 1. 1, given in IoT-Analytics.

Fig. 1. The ratio of terms related to the concept of “Internet of things” (source of Wikipedia, McKinsey, IoT-Analytics)

At the center of the scheme is M2M technology, which has been known for a long time and, in the most general terms, is defined as a technology that allows machines to exchange data via wired and wireless technologies. According to the figure, M2M is a subset of the Industrial Internet. The term “industrial Internet” is broader than M2M, and describes technologies that focus not only on machine-machine communications, but also on providing an interface to a person. The set of technologies described by the term Industry 4.0 (the term derives from the fourth industrial revolution) represents the development of the concept of the industrial Internet and involves the creation of smart industries based on digital technologies, including cloud computing, the Internet of things, 3D printers and augmented reality. The Internet of Things (Internet of Things (IoT)) is broader than the concept of the industrial Internet, because it includes consumer solutions, such as wearable IoT devices. According to IoT-Analytics, the Internet of everything is still a rather vague concept, which seeks to describe a set of technologies that provide all kinds of connections, and thus has the highest coverage in Figure. one.

The picture is complemented by a box describing a variety of technologies that correspond to the term “Web of Things” (Web of Things, WoT), which intersects with all the previously listed blocks. WoT is a set of application-level services for creating IoT applications. WoT includes principles, architectural styles, and software patterns that allow real-world objects to become part of the World Wide Web. In fig. 1 also presents the box "Internet of people" - a small amount of box, apparently, emphasizes that the number of connected devices, managed with the direct participation of a person, is less and less. But even with the formal consistency of the above terms, there are differences in details. These discrepancies are most fully analyzed in the publication of the company IDTechEx. IDTechEx researched data from various analysts and gave a graphical interpretation of the interpretation of the IoT ecosystem, emphasizing that the quantitative assessment of the IoT market depends on how it is determined.

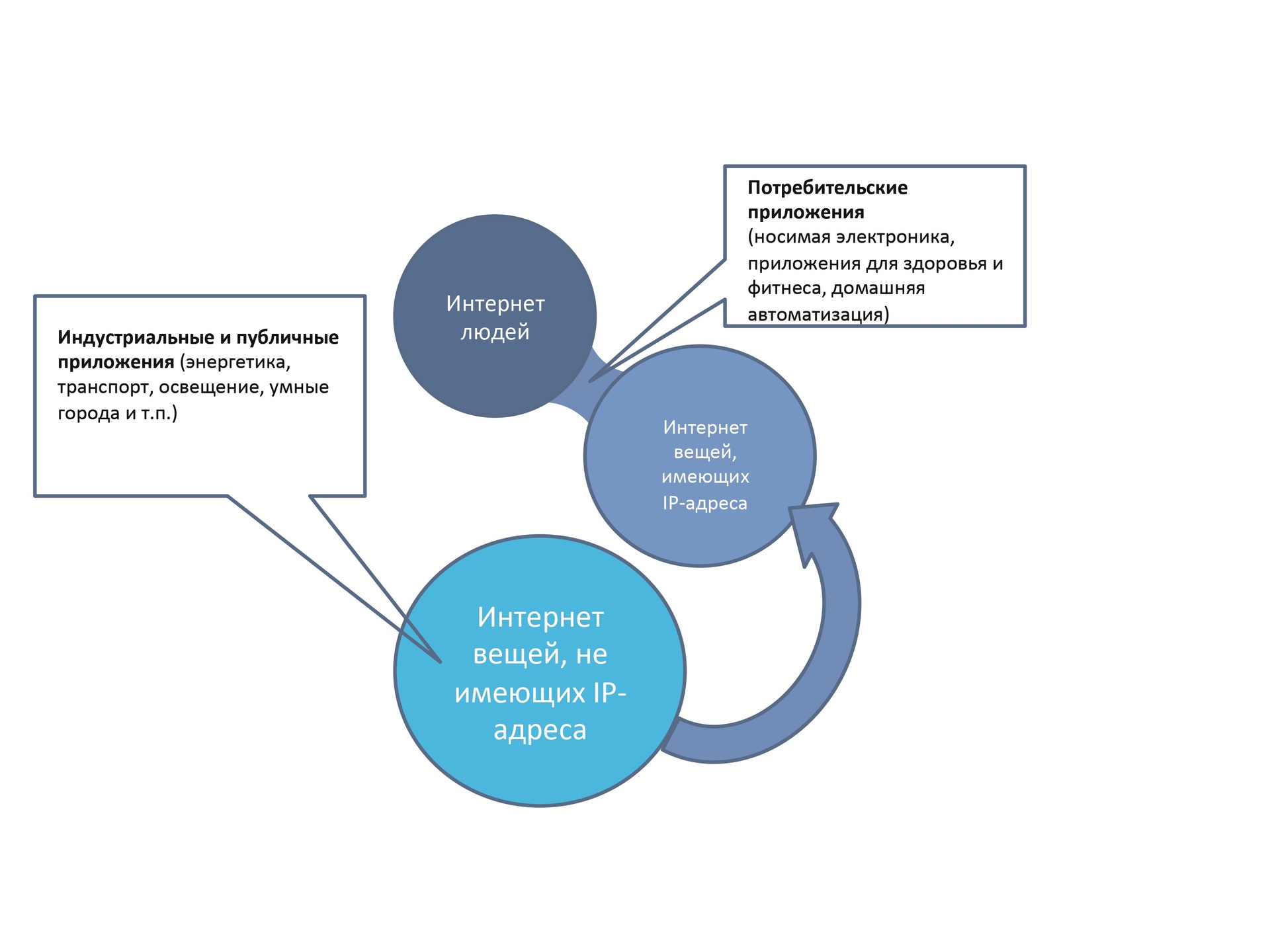

Fig. 2. IoT market taxonomy according to IDTechEx

In fig. 2. a simplified diagram is shown (the complete diagram can be found in the work) - here three subsets are shown. The first, the smallest, is the so-called Internet of People (IoP), this set includes smartphones and other personal electronic devices with Internet access. The next circle around the radius characterizes solutions based on intelligent devices (things), which include various kinds of sensors for capturing data and microcontrollers for local processing of this data. The key point is that these devices have an IP address and can interact with other things without human intervention. As can be seen from the figure, the first and second circles are connected by a jumper, denoting a transition region, which possesses the properties of both sets, but formally does not belong to them. This area includes consumer applications such as wearable electronics, health and fitness applications, and home automation tools. Some analysts attribute these solutions to the IoT market, some do not, referring to the fact that in most of these solutions, communication requires human participation. It should be noted that solutions based on IP sensors are not always required. There are, for example, very cheap solutions based on passive RFID tags, which are much cheaper compared to classic IoT devices. And solutions that use "not IP-things", a great many. Therefore, the third, largest circle defines many specialized “things” that do not have IP addresses at the level of these “things” and use other networks and other data exchange protocols. They cannot be fully attributed to IoT, although some analysts attribute them to this category, which leads to different estimates of the IoT market. However, as can be seen from fig. 2, the general trend is that the transition from solutions based on “non-IP sensors” (which have a number of limitations, including the problem of vendor dependence) to universal solutions based on IP sensors is gradually taking place. In fig. 2 this process is indicated by an arrow.

Financial assessments and market structuring

In the previous section, we looked at the differences in the interpretation of the term IoT and noted that these discrepancies can lead to different estimates of the volume of connected IoT devices. When we move from analyzing the number of deliveries of connected things to the description of the market for IoT solutions, analysts add an additional “degree of freedom” in how to describe the market. First of all, it should be recalled that analytical companies use two types of market segmentation. The first type is the approach in which all segments of the market divide it according to certain functionality, so that all these segments make up 100%. For example, hardware, software and IT services markets together make up 100% of the IT market. When we talk, for example, about the markets for cloud services, the big data market, the IoT market - as a rule, we are talking about intersecting markets. That is, the same servers, programs, IT services, and telecom services can be calculated both within the framework of the big data market and within the market of the Internet of things of things or cloud services. Therefore, in describing the market for IoT solutions, each of the analytical agencies, in principle, can decide for itself from which underlying markets and what share should be included in the market for IoT solutions. And with comparable estimates for the total volume of the ICT market, its division into mutually intersecting parts can be very different. As a confirmation of this thesis, we consider how the different analytical companies determine the boundaries of the IoT market and which segments include it.

According to IDC, spending on the global IoT market in 2014 amounted to $ 655.8 billion and will grow to $ 1.7 trillion. The cost of connecting the Internet of things and IT services will make up the bulk of the IoT market in 2020. And together they will make up more than 2/3 of the IoT market in 2020. Most of the market (31.8%) will be devices (modules / sensors).

IDC defines IoT as a network of uniquely identifiable connected devices (or “things”) that exchange data based on IP connections without human intervention. IDC emphasizes that offline connectivity is a key attribute in the definition, and does not consider smartphones, tablet computers and PCs as IoT devices. What are the horizontal segments of the IoT-market identifies IDC? According to the company's publications, in addition to hardware and software, both IT services and telecom services belong to the IoT market. That is, the IoT market is located at the junction of the IT and telecom market. Telecom services are the cost of wired and wireless providers for connecting IoT devices. IT services include consulting, hardware and software installation services, system integration, support and maintenance services, training, as well as information system outsourcing services, including cloud services.

IDC refers to hardware in the IoT market part of various kinds of connected IoT devices (controllers, sensors, RFID tags and other wired or wireless IoT devices). However, if a device, “thing” or sensor has an IP address and is autonomously connected to the network at some point during its life cycle, it falls under the definition of IoT. The hardware segment includes other elements of the ICT infrastructure (servers, storage systems, network equipment, including switches and routers, as well as hardware security systems). Software includes a wide range of software:

- analytical software that uses data collected using connected things to translate them into information for making management decisions;

- application software that provides an interface to the user, works with analytical applications, provides functions of various kinds of industry specifics;

- IoT platforms are specialized applications that integrate a range of functions and usually include: monitoring and managing connected devices; collecting IoT data, transforming and managing this data, and developing IoT applications; part of the functionality of IoT platforms may intersect with the above software categories;

- security software.

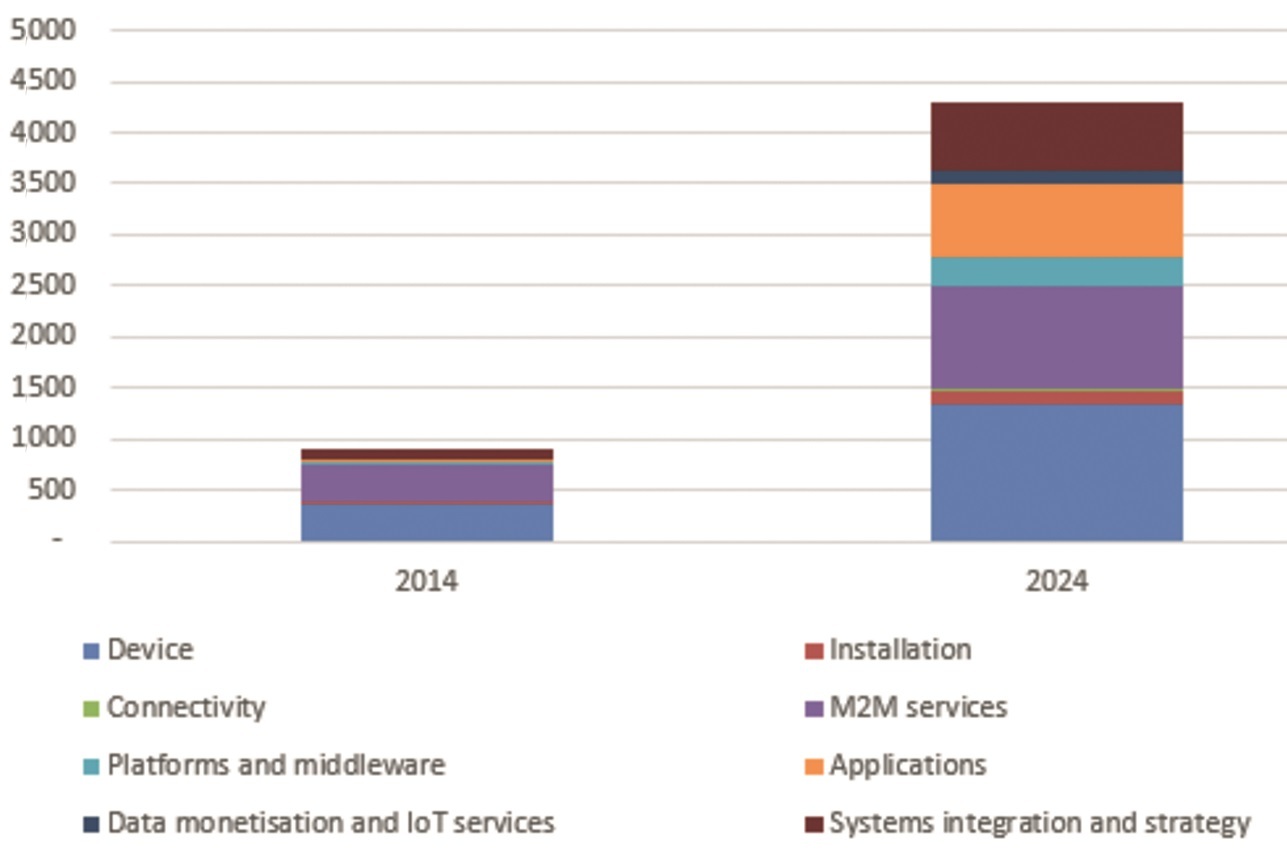

Fig. 3. Forecasts of the global IoT market, $ billion (source Maschina Research, 2015)

Machina Research uses a different market segmentation (see Figure 3). According to Machina Research, the IoT market will grow to $ 4.3 trillion by the end of 2024, reflecting a significant increase compared to $ 900 billion in 2014. As Machina Research analysts note, the main expenses for IoT include applications, professional services, M2M -services and devices. As can be seen from fig. 3, the company uses a different market segmentation from IDC: Device - devices; Connectivity - communication costs; Platforms and Middleware - platform and middleware; Data Monetization and IoT Services - monetization tools and IoT services; Installation - installation services; M2M Services - M2M services; Applications - applications; Systems Integration and Strategy - systems integration and strategy development services. Harbor Research offers its own way of structuring the IoT market (see Table 1)

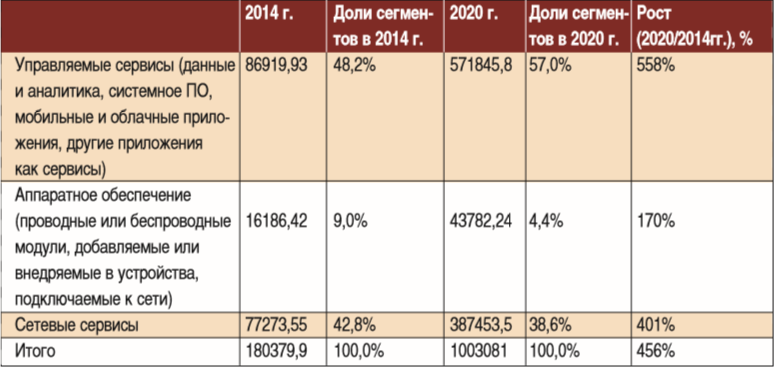

Table 1. IoT Market Development Forecast, $ million according to Harbor Research

Here, the category of hardware in 2014 is only 9%, and its share will decline with time. Apparently, in this methodology, the part of it that is provided in the managed services mode, namely as IaaS, is not included in the hardware infrastructure.

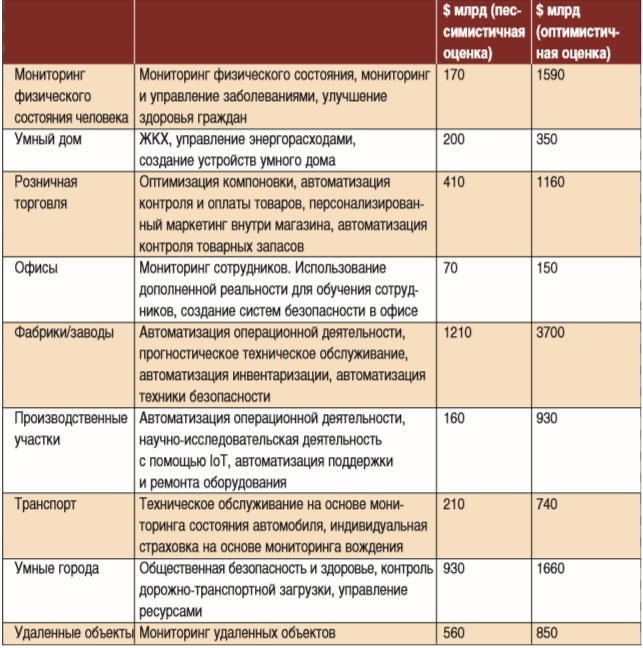

So far, we have looked at the horizontal structure of the market for IoT solutions. An analysis of publications on the vertical structure of the market shows that data from different analysts are also based on different taxonomy. As an example, table. 2 and 3 show predictions from Harbor Research and McKinsey.

Table 2. Vertical IoT Market Structure According to Harbor Research

Table 3. Vertical structure of the IoT market by 2025 according to McKinse

As can be seen from table 3, the McKinsey forecast is the only one of the above mentioned, with a variation, and in some categories the pessimistic and optimistic estimate differ significantly.

findings

To date, the IoT market estimates provided by various analytical companies are inconsistent. The size of the market may differ several times. Market structuring is carried out by internal methods, which makes it difficult to compare data from different analysts. Publications in the open press relating to the size of the IoT market, as a rule, do not provide market assessment techniques and its structure, which exacerbates confusion. Given the importance of a quantitative description of the IoT market, the attention of the IoT community should be drawn to the problem. Vendors, who are clients of analytical agencies, should have a greater influence on the development of taxonomy, on the degree of its coherence between different providers of consulting services. This will allow for greater clarity in market assessments, the role of vendors who will be able to more clearly determine their contribution and their place in the market.

» Full article

Source: https://habr.com/ru/post/312888/

All Articles