Event-oriented Python backtesting step by step. Part 4

In previous articles, we talked about what an event-oriented backtesting system was, dismantled the class hierarchy necessary for its functioning, discussed how such systems use market data , and also track positions and generate purchase orders.

Today we will talk about the execution of orders by creating a class hierarchy that will represent a simulated order processing mechanism associated with a brokerage system or another market access interface. We will also look at metrics for evaluating the performance of the strategy being tested.

')

Class hierarchy for order processing

The

ExecutionHandler component, which will be described in this part of the article, is redundantly simple, since it only executes orders at the current market price. This is an absolutely unrealistic scenario, but it serves as a good initial point for subsequent improvements and complications.As with the previously used hierarchies of abstract base classes, you need to import the necessary entities and decorators from the abc library. You also need to import

FillEvent and OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

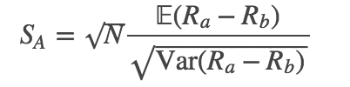

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - . OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - . OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .

OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .

OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - . OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - . OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - . OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - . OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - . OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .OrderEvent:

# execution.py import datetime import Queue from abc import ABCMeta, abstractmethod from event import FillEvent, OrderEvent

ExecutionHandler execute_order :

# execution.py class ExecutionHandler(object): """ ExecutionHandler , Portfolio Fill, . . . """ __metaclass__ = ABCMeta @abstractmethod def execute_order(self, event): """ Order , Fill, Events. : event - Event """ raise NotImplementedError("Should implement execute_order()")

. , , . , , , , .

, FillEvent fill_cost None (. execute_order ), NaivePortfolio ( ). “value”, .

ARCA. .

# execution.py class SimulatedExecutionHandler(ExecutionHandler): """ Fill, , .. . """ def __init__(self, events): """ , . : events - Event. """ self.events = events def execute_order(self, event): """ Order Fill, , , / . : event - Event . """ if event.type == 'ORDER': fill_event = FillEvent(datetime.datetime.utcnow(), event.symbol, 'ARCA', event.quantity, event.direction, None) self.events.put(fill_event)

. , .

- . :

R a , R b — , .

— , . , , .

.

Python

performance.py , . , , NumPy Pandas:

# performance.py import numpy as np import pandas as pd

, — . , .

252 — . , , , . : 252 ∗ 6.5 = 1638 ( ). , 60: 252∗6.5∗60 = 98280.

create_sharpe_ratio Pandas Series returns .

# performance.py def create_sharpe_ratio(returns, periods=252): """ , ( ). : returns - Series Pandas - (252), (252*6.5), (252*6.5*60) ... """ return np.sqrt(periods) * (np.mean(returns)) / np.std(returns)

, ( ) , .

create_drawdowns , , — . — «», .

pandas Series, . HWM (high water mark) — , .

HWM . , , , HWM. :

# performance.py def create_drawdowns(equity_curve): """ PnL . pnl_returns pandas Series. : pnl - pandas Series, . : drawdown, duration - """ # # High Water Mark # hwm = [0] eq_idx = equity_curve.index drawdown = pd.Series(index = eq_idx) duration = pd.Series(index = eq_idx) # for t in range(1, len(eq_idx)): cur_hwm = max(hwm[t-1], equity_curve[t]) hwm.append(cur_hwm) drawdown[t]= hwm[t] - equity_curve[t] duration[t]= 0 if drawdown[t] == 0 else duration[t-1] + 1 return drawdown.max(), duration.max()

, , . . , , Portfolio , .

portfolio.py :

# portfolio.py .. # from performance import create_sharpe_ratio, create_drawdowns

Portfolio — , . NaivePortfolio . output_summary_stats — .

. pandas, :

# portfolio.py .. .. class NaivePortfolio(object): .. .. def output_summary_stats(self): """ — . """ total_return = self.equity_curve['equity_curve'][-1] returns = self.equity_curve['returns'] pnl = self.equity_curve['equity_curve'] sharpe_ratio = create_sharpe_ratio(returns) max_dd, dd_duration = create_drawdowns(pnl) stats = [("Total Return", "%0.2f%%" % ((total_return - 1.0) * 100.0)), ("Sharpe Ratio", "%0.2f" % sharpe_ratio), ("Max Drawdown", "%0.2f%%" % (max_dd * 100.0)), ("Drawdown Duration", "%d" % dd_duration)] return stats

. . performance.py output_summary_stats .

…

PS . ITinvest - .Source: https://habr.com/ru/post/268929/

All Articles