Hawala: The algorithm of the underground banking system, preserved from ancient times

A few months ago, a material was published on Habré in which the algorithm for the movement of money in the banking system was described. However, the banks we are used to are not the only tool that residents of different countries of the world use to work with finances.

One of these financial and settlement systems is called "Hawala". It originated in Hindustan long before the appearance of the western-style banking system (according to various estimates, it worked already in the 8th century), and is still used by many citizens of the countries of the Middle East, Africa and Asia as an alternative calculation tool.

Underground banking

The word hawala in Arabic means a bill or package. A feature of the hawala system is the fact that all financial transactions (moving money from one country to another, money or gold) are carried out without any documentary evidence - the work is based on the confidence of the participants in the process.

')

The main link in the hawala system is the system brokers - they are called hawaladars. They organize transfers between countries. Physically, the money does not leave the state: the sender simply gives the money to a broker in one country, receives a secret code from him (for example, digits from one of the bills), which the recipient in another country must then call the second broker to get the equivalent of the initial amount in local currency.

Subsequently, brokers are calculated among themselves according to the clearing scheme - gold, precious metals, or some services can be used to close the balance.

The exact number of hawala brokers operating in the world cannot be calculated - estimates range from 5,000 to tens of thousands. There are regional varieties of hawala, for example, “hundi” in India.

How it works

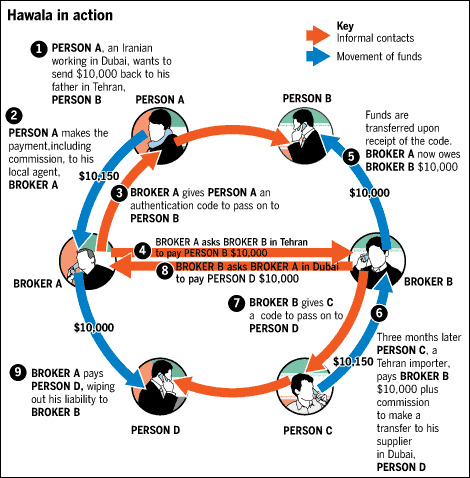

The hawala scheme is easier to illustrate with an example.

Suppose a client (CA) from country A wants to make a transfer (or pay some of its obligations) to client CB from country B. Havaladar (broker) HA from country A receives money in the currency of country A and provides him with a code for confirmation transactions. He then contacts the havaladar from the second country (HB) by email, fax or phone and tells him the details of the transfer and the amount equivalent to which in local currency must be given to the recipient (CB). To receive money, the recipient must call the hawaladar code that the first broker called the sender of the transfer.

Such a scheme is called “ simple reverse hawala ” - in this case, money is not physically transferred from the broker to the broker. If we assume that the sender is in the USA and the recipient is in India, then the Indian hawaladar will pay the recipient from its own funds. Subsequently, to settle the accounts, a broker in the United States will make a payment to a recipient in this country on behalf of a client from India.

Over time, the total net amount of transactions can be balanced, but usually the asymmetry of cash flows between countries does not allow this. Therefore, in the end, mutual settlements are made for which transfers can even be used with the help of the usual banking system.

The method described above is not the only kind of hawala. There are also options for trilateral agreements with brokers . Hawaladars can be part of a network spread over several jurisdictions. Then they use the balance of mutual settlements and correspondents to keep track of their respective accounts.

In the example above, brokers from the USA and India can operate on the same broad network. After the first transaction, the hawaladar from the USA becomes the debtor of the Indian broker. In this case, the second broker may have a client who wants to make a transfer to a third country, for example, Somalia. If this broker does not have partners in the desired country, he can contact the hawaladar in the United States for help, asking him to find a partner in Somalia who owes money to the broker from the United States himself. When a hawaladar in Somalia makes a payment to the recipient on behalf of a broker in India, all mutual settlements are closed.

Another way to make payments through the hawala system is to use trade transactions with overvalued or undervalued accounts . According to the report of the Financial Action Task Force on Money Laundering (FATF), agreements of this type are common in Afghanistan, Iran, Pakistan and Somalia. In this configuration, brokers make payments from the active balance of cash or non-cash funds upon request of an organization, which already, in turn, makes payments to private recipients in the country of destination of the transfer.

What is hawala for?

Hawala allows you to quickly (from 24 to 48 hours) transfer large sums of money with minimal commissions, making the operations completely “invisible” to the authorities of the countries between which transactions take place.

As a rule, remittance transfers are used by immigrants from developing countries to send money to their homeland. The money senders do not always want extra attention to themselves or, in principle, have the opportunity to use banking services. They may be in the country illegally or with an expired visa. In this case, hawala becomes almost the only means of sending money without the need to prove your identity, which is required in the case of a bank transfer.

In addition to private individuals, entire countries use Havala translations - in 2008, the Financial Times published an analysis of how the country bypassed the sanctions imposed on its banks with this financial system. As the journalists found out, the Central Bank of Iran issued hawala brokers licenses for money transfer activities, which ultimately ended up in accounts in banks in the United States, Europe and Asian countries.

Attitude of the authorities

The ease of use of the system, as well as its opacity for government officials and a minimum of “paperwork”, make hawala an attractive tool for money laundering or tax evasion. There are also suspicions of the use of hawala by terrorist organizations - US intelligence agencies have paid attention to the system after the September 11 attacks.

We also found hawala network locations in Russia - for example, several years ago the media wrote about closing a whole network of underground money transfer points in Moscow.

Countering the hawala “shadow banks” is an extremely difficult task. Some economists even suggest not following the way of their prohibition, but preventing the use of hawala for criminal purposes. One of them is the deputy director of the International Monetary Fund (IMF), Mohammed El Korci, in his article “ The Hawala System ” back in 2002 stated that as long as people have reasons to use hawala, such systems will exist and even expand.

“If the formal banking sector is going to compete with the shady money transfer business, it needs to focus on improving the quality of service and reducing commissions,” El-Corci said. “In addition, the authorities need to constantly work to modernize and liberalize the financial sector, as well as eliminate its inefficiencies and weaknesses that cause inconvenience to users.”

Bibliography:

Source: https://habr.com/ru/post/267961/

All Articles