Information technology and big money

Banking services are essential. Banks - no.

Bill Gates

For several decades, information technology has changed the world beyond recognition. As applied to the banking sector and financial institutions, issues of state regulation and protection of information, as well as issues of countering the laundering of proceeds from crime are most often raised. However, these are not the only challenges facing the financial sector. Customer needs and habits change over time, and information technology is one of the most important drivers.

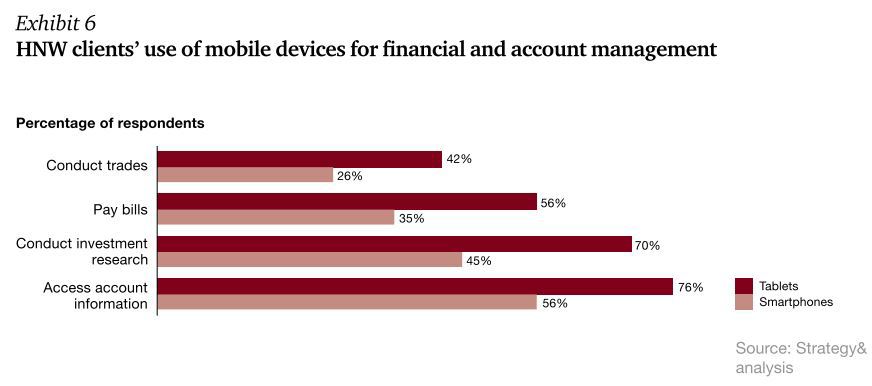

So, secured customers are already using mobile devices not only to access information on the account and pay bills, but also to enter into transactions.

')

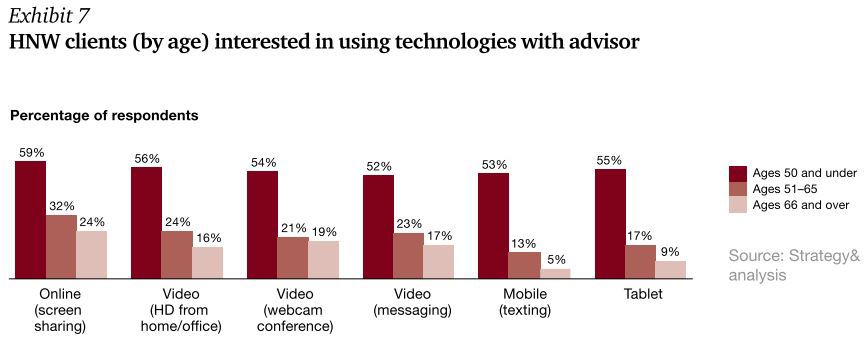

But it's not just the daily use of tablets and smartphones. A new generation of customers requires new channels of communication and modern forms of interaction. In this case, a similar request comes in, including from the older generation.

Let's try to analyze the challenges facing the wealth management industry, serving the interests of the most sophisticated clients.

Service Providers

Individuals with free invested assets of one million dollars are served by a special group of financial (and not only) service providers. The main task - the preservation and enhancement of well-being. To this group we can conditionally refer:

- private banking - special units of universal or investment banks, as well as independent banks serving only wealthy clients;

- wealth managers - individual companies that will help with asset management and select premium housing in London and advise the right university for children;

- family offices are separate structures created for the interests of a specific family with a unique set of services, most often of a financial nature.

Some facts

- American millionaire uses an average of 2.8 social networks and has 110 contacts

- Almost half of the wealthiest Europeans use Facebook

- Only 22 out of 50 banks optimized their websites for smartphones.

- According to experts, by 2030 the number of online customers of banks in Germany will be 44 million people (against 27 million in 2010)

- More than 50% of wealthy Europeans view social media as an important channel of communication with their bank.

New rules of the game

Chris Pitts, a Canadian partner of PwC, names six strategic megatrends for which the wealth management industry needs to prepare now. Technological change is one of them, along with emerging markets, competition for natural resources, government regulation, demographic, social and behavioral changes. An asset manager who successfully uses the data will find new opportunities for his business. At the same time, there are significant threats to today's players. In the future, the role of technologically armed managers is expected to increase. A well-technologically structured solution aimed at the mass market can completely change the rules of the game. Imagine that tomorrow, Google will start managing assets and investments.

Technologies are necessary for the effective exchange of information between participants in the investment process, primarily between the manager of the state and the client. At the same time, the approaches to the markets of India and China are very different from work, for example, in Canada. In such conditions , the requirements for the architecture of information systems and scalability are increasing . So, when designing a mobile money transfer solution, you need to be prepared to meet regulatory disclosure requirements (for example, FATCA ). This is especially important when entering emerging markets with a large number of potential consumers. In the foreseeable future, we can expect significant capital investments in IT by service providers who want to work with data in the wealth management industry. Although aggregated client reports remain the main task today, data management and security issues may be the number one priority in the next year or two. Two other hot issues are CRM and client interfaces.

Another reason for financial institutions to think about is rapidly aging systems. The consumer needs integrated solutions of higher quality, easily accessible, providing relevant information in real time.

Outsourcing

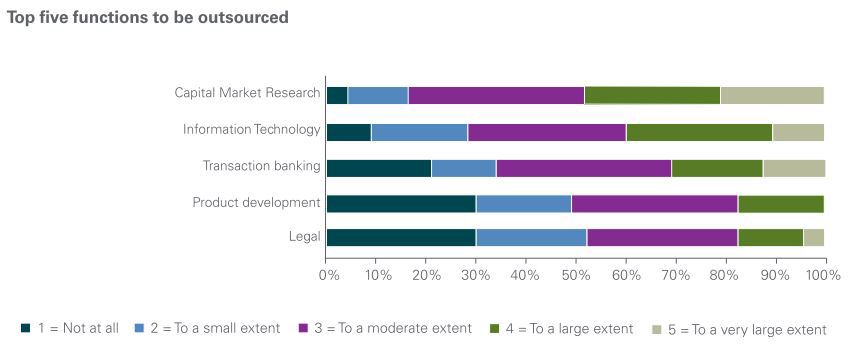

Of course, financial institutions are aware of the rapidly growing role of technology in business. The described challenges can stimulate new interaction formats. Often their own competence is not enough, besides the development of in-house solutions is expensive. In 2013, KPMG conducted interviews with 39 heads of Swiss banks. According to the research, information technologies are among the top five functions that banks will outsource in the next 10 years. At the same time, the majority of respondents tend to transfer “moderate” or “significant” number of tasks (answers “3” and “4” on a five-point scale). Interesting is the position of 10% who plan to outsource the vast majority of IT functions.

Demand for in-house specialists

Family offices are rarely investigated. This is due to the difficulties of obtaining information relating to such structures, as well as a broad interpretation of the concept itself. With the exception of representatives of the wealth management industry, few were interested in them. In 2014, the Center for Wealth Management and Philanthropy of the SKOLKOVO Business School conducted several dozen interviews with Russia's largest entrepreneurs, including the richest Russian businessmen, according to Forbes. One of the questions concerned the need for their own specialists. It turned out that more than a third of the respondents would like to have (or already have) their own IT specialists within their family office.

According to the Family Office Association, the position of Director of Information Technology / CIO is often underestimated in family offices. In such structures, there are often highly specialized software requirements, and the role of the CIO is to coordinate the entire technical infrastructure. The main tasks are to ensure the unity and interaction of the entrepreneurial family, strengthen control over the family office and reduce costs. The salary of such a specialist is $ 75,000- $ 150,000 per year, depending on the complexity of the tasks.

Scenarios 2030

Professor Teodoro D. Cocca, Professor Teodoro D. Cocca, offers 4 scenarios for the development of the situation in the wealth management industry over the next 15 years.

Scenario 1: No change

Most customers will reject the integration of information technology in the banking business. Scandals related to hacking banks, security problems and protecting the privacy of customers among the first innovators will finally undermine the confidence of wealthy customers. Stricter regulation will prevent the creation of new companies in the financial sector. Banks will not have an urgent need to restructure their business models. By 2030, financial services are rendered in the traditional way - through face-to-face meetings with financial advisors.

Scenario 2: Evolutionary

Wealthy clients are served in reliable and time-tested banks, and the latter combine traditional services, physical presence and new communication channels, including social media. Modern technologies help the interaction between the capital manager and the client, but at the same time, the complex and complex nature of the services does not allow to go completely to the virtual mode. Successful innovative solutions are bought and integrated by banks into their business models. Constant monitoring of new solutions is becoming necessary for market leaders.

Scenario 3: Apple and Facebook create iWealth

Traditional service providers were completely unable to optimize their business models for rapidly changing customer needs. To the forefront of the company, in the past not related to the financial sector. The world's first virtual bank created by Apple and Facebook is becoming a new force in the asset management business. By 2030, iWealth used by 5 million millionaires worldwide. This customer network is at the same time the key “asset” of the new company. iWealth brings design and client interfaces to perfection, while financial products themselves are developed by traditional banks, which now never work directly with customers.

Scenario 4: Own virtual bank

IWealth and similar companies provide access to products of a limited number of service providers, while consumers need even more flexibility in choosing. The client creates his own virtual financial services aggregator based on his needs. In this case, any of the links in the chain of services is interchangeable. Banks provide technical infrastructure without interacting directly with the customer.

Scenarios 2 and 3 are rated as most likely.

Sources

- Conference “Private Welfare in Russia” - Center for Welfare Management and Philanthropy of the SKOLKOVO Business School, November 25, 2014

- C. Pitts, “The Future of Wealth Management,” CFA Inst. Conf. Proc. Q., vol. 31, no. 2, pp. 24–31, Jan. 2014

- Private Banking Survey 2013: Success through innovation - KPMG, 2013

- Talking Wealth Management Digital - Booz & Company, 2013

- Online Banking and Demography for Granted - Dapp, T., Deutsche Bank Research, 2013

- Social Media Study - Assentium, 2012

- AJ Robles, Family Office Association, 2009.

- Five Social Networking Sites Of The Wealthy - Forbes, 2008

Source: https://habr.com/ru/post/244907/

All Articles