Principles of building management reports based on data from existing accounting databases

Having spent several years on research in the field of automation of accounting processes, we found and implemented a number of unique innovative technologies, as well as developed a methodology and a number of software products. But, in order to create applied solutions in the realities of everyday practice, we had to spend the last two years communicating directly with accounting specialists and consumers of accounting results.

To describe the results of all the research, we will need to write a whole book, but first we decided to focus on the task that exists in actual practice, which can hardly be called problem-free.

The task of organizing the processes of forming management reports based on rather disparate data in a non-standard format and on non-standard requirements of management interpretation is present at each enterprise. Depending on the size of the enterprise, the level of profitability, the industry, various people are involved in the production of these processes, with different education and different views. In small micro business companies, this is often done by the manager himself, who can be the owner at the same time. In a small and medium business, and this is in quantitative terms the largest segment, this task is often superimposed on accounting. The notion of an economist and a financier appears in medium and large business, the position of finance director appears, which is higher in the hierarchy of the chief accountant, as well as whole FED (financial and economic departments) appear.

')

Only one thing unites these people regarding approaches to solving the problem of building management reports: for the most part, Excel worksheets are used as a tool.

On the one hand, Excel spreadsheets do not initially have any methods and business logic; at the same time, on the other hand, they are functionally capable of providing very broad requirements. Although, with the apparent convenience of this tool, there are significant limitations.

If very short.

The absence of a pledged accounting business logic generates very bad, in terms of basic systematics, construction. Those. Each builds a structure for storing, processing and displaying data in accordance with its own level of understanding of these processes.

Excel is often called "flat." Apparently this feeling arises because relational databases are not used, and the client and server architecture, but few understand this in real practice. Flat and that's it.

As an obvious disadvantage, simultaneous collaboration with data is impossible or extremely difficult.

1C + Excel.

In general, spreadsheets solve a certain stage of the overall task perfectly, so systems begin to line up in a hybrid way. Data is maintained in databases (relational databases and client / server architecture). In Russia, the vast majority use different configurations of 1C. In these databases, a number of aggregate reports are manually formed, which are preempted into Excel, and then a miracle specialists in the limitless possibilities of this tool

Conducting our research for several years, we have felt a clear trend towards this option of building management reporting procedures. As proof, I can offer to conduct an experiment. On the site hh.ru in the search for vacancies type "management reports" or "management accounting." You will receive a list of vacancies related to the functions of management accounting and the construction of management reports. For these vacancies it will be possible to understand how the labor market formulates the requirements for specialists of these functions. In the majority of vacancies there will be a clearly formulated requirement of excellent possession of 1C plus Excel.

You can also find precedents in the market when companies producing a software product for forming management reports position their products as a direct competitor to Excel. Example Fingrad. “Have you already grown from Excel?” By the way, it is this manufacturer that very clearly formulates the disadvantages of using Excel tables in management accounting procedures. Still would! After all, they themselves position themselves. One of the main arguments is a remarkable factor that there is no double entry in Excel. And here begins the most interesting. Most practitioners will not understand this factor, and those who "grew out of Excel" will fully agree.

The main forms of management reports.

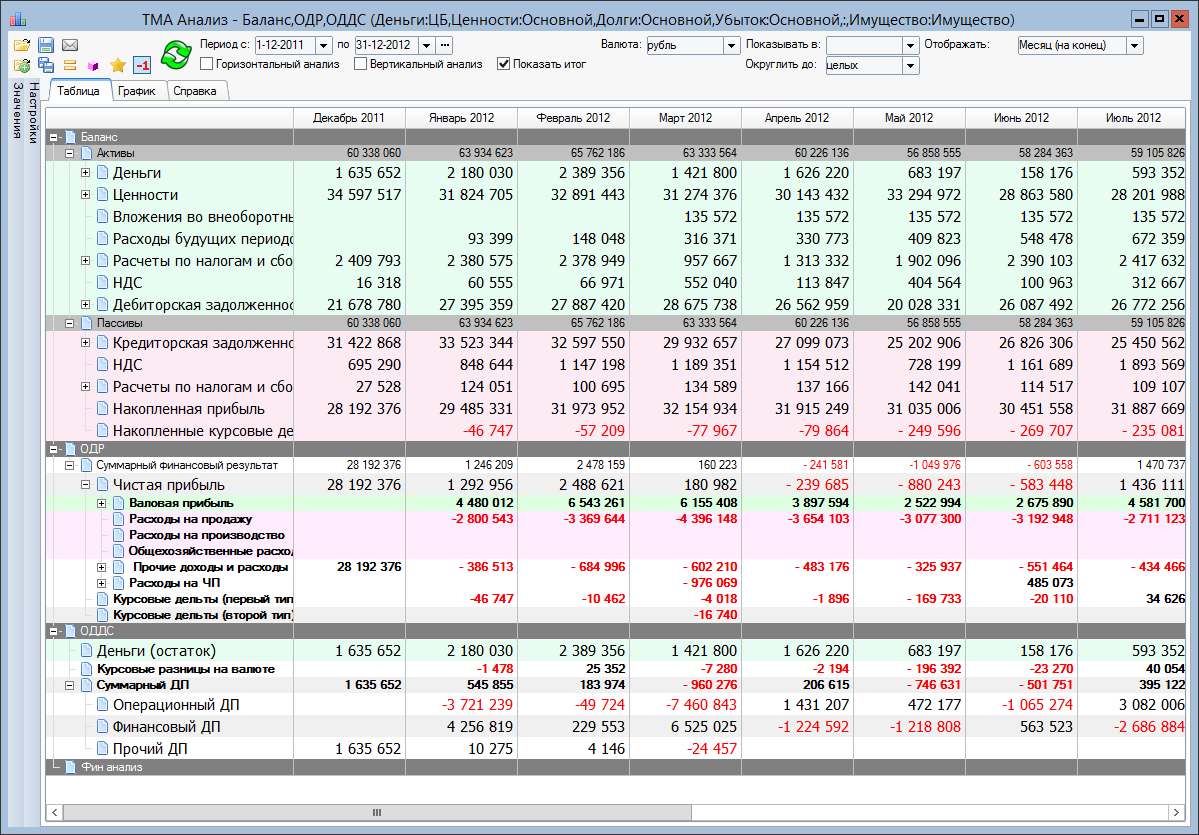

The main idea of this factor is that management reports should be in the form of a standard triad: Balance; Income and Expense Report (SDT); Cash Flow Statement (ODDS). It is technologically extremely difficult to build these forms if the accounting of operations is not conducted on the principle of double-entry, and it is extremely difficult to do this in Excel.

Many financiers still neglect these forms for building information management reports on actual results and, accordingly, in budgeting. I can quote the words of the financial director of one of the largest industrial and trading holdings in Russia: “I don’t need a balance, I need a plan-fact”. I wonder what she meant? It is clear that she does not need a balance, but under plan-fact she most likely meant DDS. But this person determines the structure of the management accounting system in a very large and serious commercial organization. The traditional construction of management accounting and budgeting systems on the initial basis of the monetary basis, according to our research, is probably the biggest accounting problem in the small and medium business segment. And this is understandable. Culture and technology management accounting in commercial organizations, we began to emerge much later than the business itself began to appear.

Some analysts argue that our economic schools have adapted to the demands of a market economy only by 2004, and therefore, only graduates from 2007–2008 have more or less met their professional requirements. And all this time, since the time of restructuring, it was necessary to somehow control the business and analyze its results. Money count is the most understandable and simple. Therefore, they first learned how to count money and make DDS reports, both a plan and a fact, in Excel (in our country it was always at hand, and in the most recent versions), and then they began to try to take into account charges and strive to build a balance.

According to our observations, this is a kind of evolutionary ladder for the development of management accounting in commercial enterprises in Russia. Those who are not very greedy and managed to earn enough money, they made it easier, bought the SAP ERP system. And in the process of implementing the procedures and accounting functions were brought to the proper state at the level of business processes. But such systems do not just cost several million dollars, they are also very expensive to operate. Naturally, small and medium businesses cannot afford such decisions in terms of their level of profitability.

But still it is necessary to note the existence of an emerging trend of demand in this segment for management accounting, where the resulting reports are considered to be a full-fledged triad of financial reports, on the basis of which you can build a full-fledged financial analysis. To prove this, we will return hh.ru and in the same request “management accounting” in the vacancies we will find clearly formulated requirements “Formation of management reports (Balance, ODR, ODS)”. Two years ago it was a great rarity.

The main and most accessible source of data for management accounting.

In this article, I consider the option of building management reports based on data from existing accounting databases. Under management reports naturally means, first of all, a full-fledged triad (Balance, ODS, ODSA), but we are not limited to it. We need reports on physical values, and more detailed data, and general financial analysis, and graphs. By management reports we will mean the main triad plus any other reports on the database of business operations that may be needed to inform management decision-making.

Why do we suggest first looking at the option of using accounting data in management accounting?

1. There is almost all the data that is needed.

2. Accounting records are recorded according to the double entry principle.

3. Accounting is in all enterprises.

4. According to our research, this is the most effective way, and such an approach can easily afford a small business, moreover, using the resources of existing accounting services, without creating additional specialties.

What do you need to get management reports from these accounting databases?

1. It is necessary for the enterprise to conduct accounting properly. This requirement coincides with the requirement of the law!

2. We need a tool that will allow:

a. Collect data from different databases.

b. Interpret the collected data in the conditional rules of management accounting.

c. Correct, delete, add data in order to correctly, from the point of view of management accounting, display information in reports.

d. Perform consolidation procedures (elimination of intragroup transactions and establishment of correspondences of reference information) when a business includes several legal entities or business units.

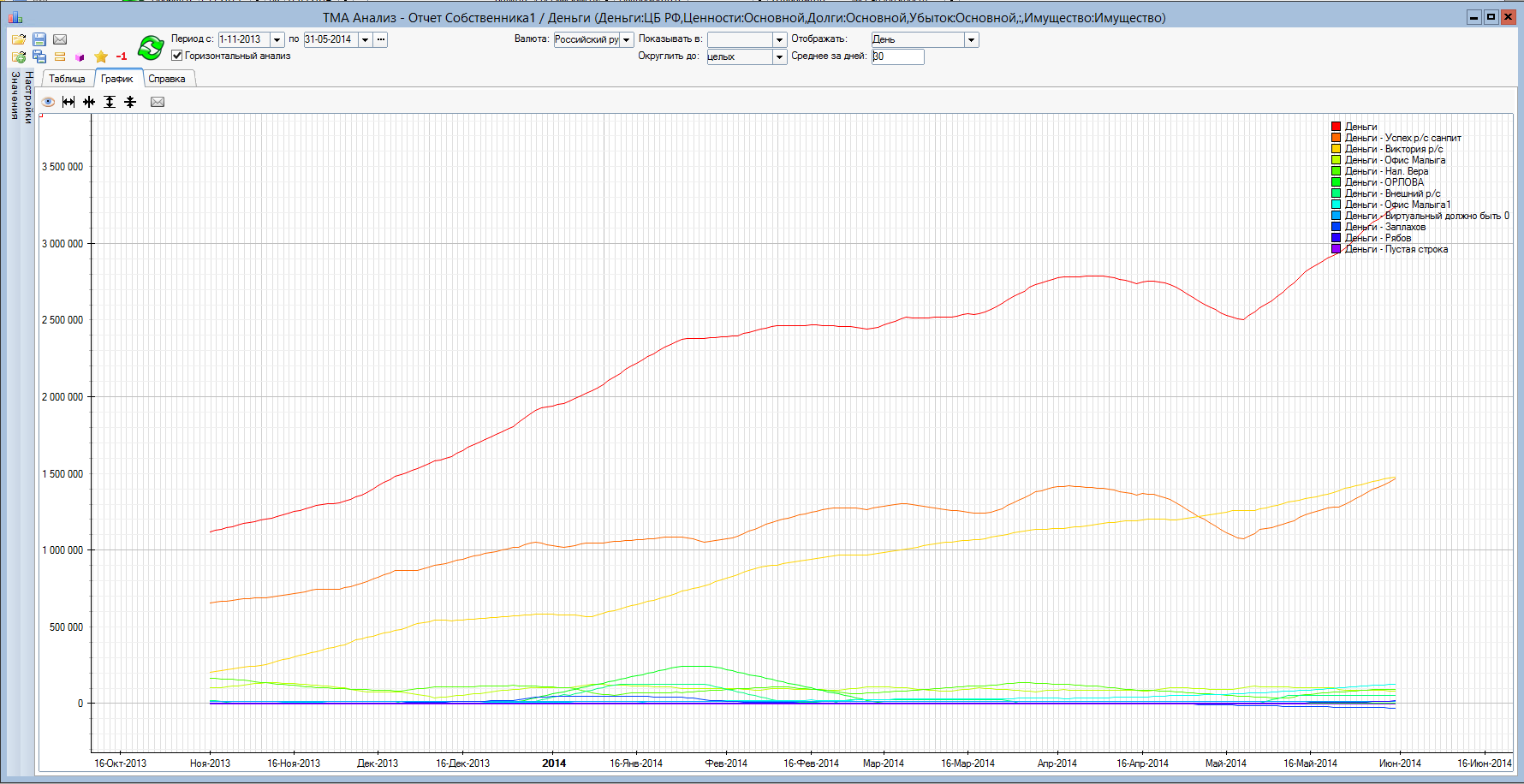

e. Analyze management reports by detailing, matching, graphs.

f. Do all of the above actions without the participation of special tuners or programmers.

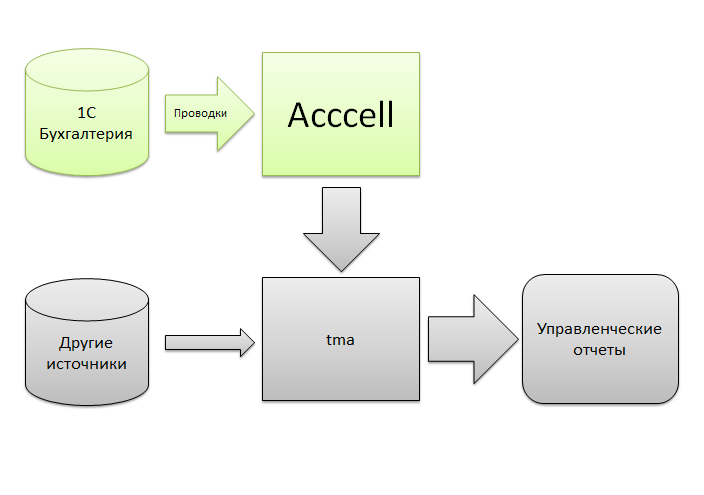

A tool for converting accounting data into management reports.

In the course of our development and their implementation in practice, many tools emerged, but the very first was a tool that allowed to import transactions from accounting databases (the original software does not matter), to prescribe rules for interpreting accounting data in management accounting, to add, correct, exclude data , consolidate them between several interrelated legal entities.

It was the easiest tool. Later we created the possibility of integration with any forms of documents, i.e. ability to import not only from accounting. Then came the possibility of building a chain, when importing data comes from a source into a document with the possibility of correction and subsequent implementation in management accounting. All this overgrown with a significant amount of tools for comfortable work in practice. We used the system in very complex large projects for the formulation of management accounting and budgeting in complex diversified holdings. In general, integration processes in holdings with a “zoo” of disparate different functional bases are so complex that they require a large participation of external specialists. And this is always project work. And it is always very expensive.

But we wanted to create a simple, affordable, even for small business and scalable product, which would be easy to use by the usual practices of various accounting specialties without the special participation of any external specialists.

The last two years, exploring the market and communicating with representatives of all parts of the consumer chain, we decided that the most effective method, in terms of price factors (all resources expended) and quality, is the option of using data from existing accounting databases. We took the initial developments and mounted a scalable option available. We introduced not only the possibilities to form the rules into the program, but also set up preliminary versions for the Russian accounting system, as well as options for ready-made reports. The product was named ACCCell (account + cell).

The basic principles of building management reports, based on data from existing accounting databases, I will describe exactly according to the functions of the ACCCell program. This will no longer be just blah blah in theory, but instrumental methods based on practical experience.

The order of the system to transform the accounting data into management reports using ACCCell.

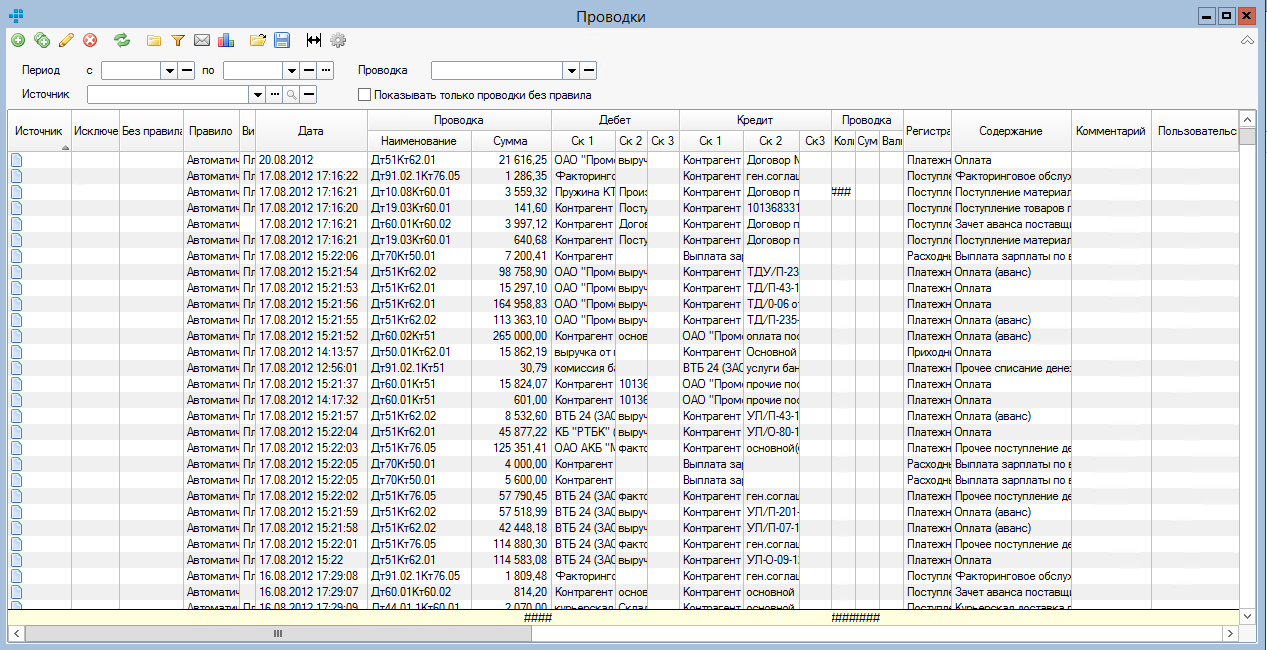

The first step is to import data from accounting databases. In the use case of 1C Accounting, there is the possibility of direct connection and synchronization, plus the ability to import through a file. As a result, we get a complete copy of the list of transactions with all their contents, as the source material.

This operation can be performed by an ordinary accounting operator.

If for a certain period the downloads are re-conducted, then we will see in the list which transactions are new, which have changed, and which have been deleted. The system will require confirmation of these changes, and the specialist will be aware of what was changed retroactively in the unclosed period.

It is possible to download postings from several databases and different legal entities. Each transaction will have a data source identifier, and in the body of the transaction will be information about the organization. It happens that a business uses several legal entities, while there are no intragroup transactions, then you can easily get consolidated reports by downloading all the transactions in one database. If intragroup movements are present, then it is necessary to use consolidation functions.

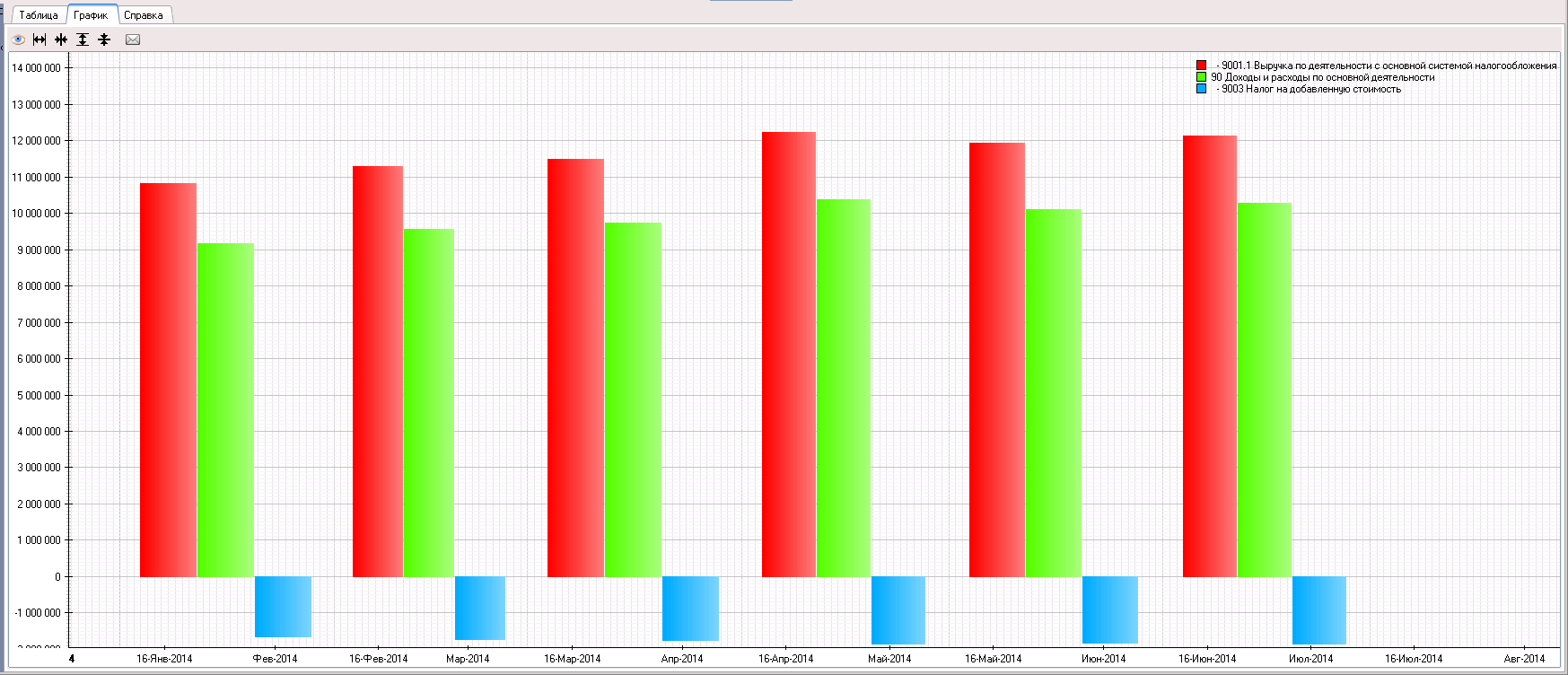

In ACCCell, there is a customized interpretation option and a customized version of the master reports, so loaded wiring can be immediately processed and obtained material for analysis.

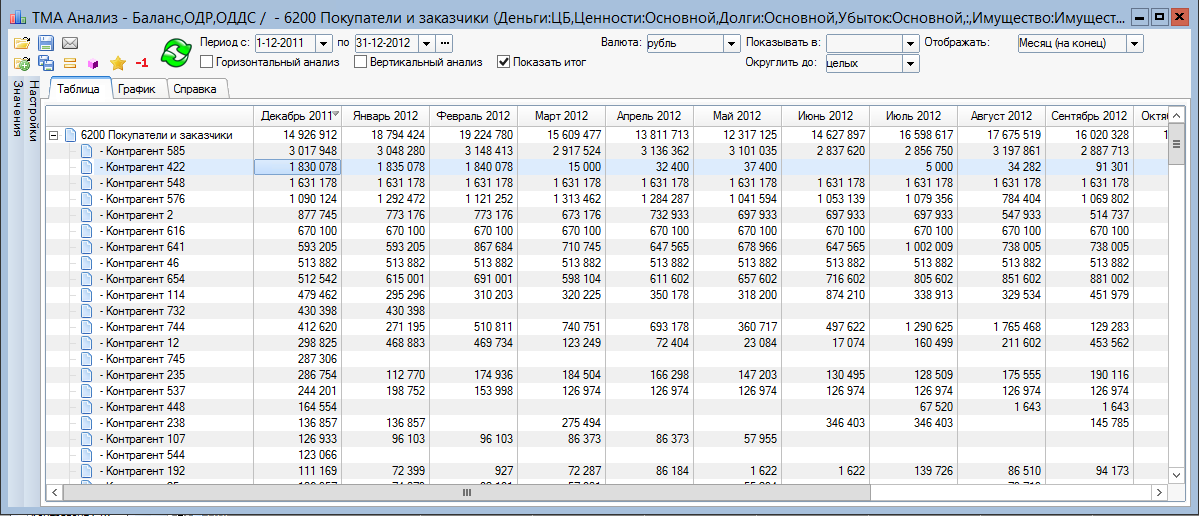

In the resulting report, all articles are detailed in various analytical sections. For example, we can expand the receivables directly in the report.

And then deploy customer receivables by counterparty

As a result, it takes several minutes to get ready basic reports from accounting bases.

Analyzing the data of these reports, the specialist will easily find inaccuracies that may occur both within the accounting and at the level of the set interpretation rules.

In practice, the specialists were very pleased that, thanks to ACCCell, they found many errors in the accounting department.

The next stage of work will be the analysis and correction.

.We can correct the data in various ways.

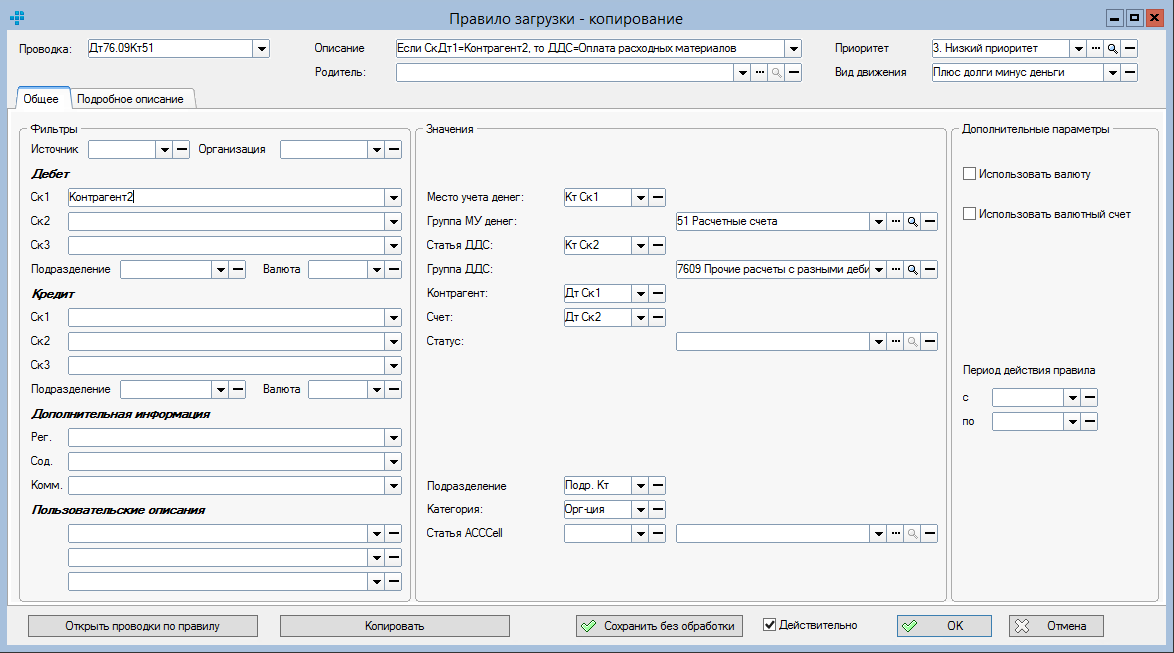

If the automatic processing rule gives a system inaccuracy, then you can enter the most priority rule itself (screenshot 5). This is easily done by a trained specialist.

If it is necessary to change the interpretation of a particular transaction, an exception is easily made, and we immediately get the result.

In ACCCell, you can easily enter manual operations that will complement or correct the overall picture, as well as you can download data from other external sources, for example, Excell tables or other management bases, or bank statements, etc. The general scheme of ACCCell is:

tma is the main processor of accounting within the system, which uses innovative and patented data processing technologies. Thanks to this engine you will not have problems with exchange rate and cost differences, and the accounting process is fully automated.

And finally, corrections can be made in the original accounting databases, then reload data and process, which takes very little time.

The ability to interpret the data of accounting bases in the conditional rules of management accounting is one of the main principles and functionality of the tool for building management reports based on the data of existing accounting.

At the same time, one cannot neglect another basic principle. It is necessary to adjust the accounting itself properly so that the data are entered into it in a timely manner, in accordance with the requirements of management accounting, and not RAS. For example, accounting can be closed quarterly, which means that a lot of data is entered at the end of the quarter, although it could be entered daily. Management accounting may require monthly reporting and this imposes the requirement of completeness of data in the accounting department over the requirements of RAS. It should be noted that the operation of closing the month is not necessary.

Management reports do not end with just three main reports.

In conclusion, another principle should be noted. A tool designed to generate management reports based on accounting data should be able to provide various kinds of analytics, including based on natural values and graphs.

Additional functions

In practice, we have come to the full conviction that management accounting cannot fully exist without the functions of group consolidation, budgeting and treasury.

These functions are fully implemented in the ACCCell program.

Conclusion

In this article, I tried to reasonably enumerate the basic principles of the formation of management reports, based on data from existing accounting databases. But in one article it is impossible to describe all the nuances that we encountered in practice, and how these nuances are solved using the tools of ACCCell.

All those who are interested in this topic are invited to an open seminar and presentation of the ACCCell program, which will be held on September 30.

Registration by reference .

Source: https://habr.com/ru/post/237659/

All Articles