Investing for Dummies

Many of Habr's readers earn good money (I hope) and have the opportunity to cover not only current expenses, but also spending money on something promising. Again, many of us are thinking about how to save money for the future, so that they do not “burn out” over time (minimum task) and how to make money to make money (

Many of Habr's readers earn good money (I hope) and have the opportunity to cover not only current expenses, but also spending money on something promising. Again, many of us are thinking about how to save money for the future, so that they do not “burn out” over time (minimum task) and how to make money to make money ( I became interested in this question about two years ago. As it turned out, the maximum problem is solved, and the dream of a free pastime of up to 60 years is quite real. Moreover, in the West, the “asset allocation” approach is popular, which allows you to spend up to an hour per year on an investment question and have results comparable to professional investors. And you just need to firmly understand the basic information and not dive into the abysses of technical and fundamental analysis.

As it turned out, this approach is available in our country, in our reality. The results of the research I want to share with you. Yes, so far only research ... In 30 years I will tell you about the results of the practice.

')

Now I see that if I had thought about it ten years ago, I would have been halfway to my dream! What a pity that I was only thinking about computers (well ... not only about them, but I certainly didn’t think about finance!) ... However, it’s better later than very, very later.

PS Why do it yourself? Because you yourself can save yourself some good money - you, not banks, a pension fund or financial companies!

UPD. PPS My thoughts are based on Sergey Spirin's article “Portfolio of couch potatoes, or how to increase capital by 118 times in 12 years” . Actually, from him I learned about this investment strategy. I am an IT person, not a financier. Therefore, for details from the expert - to him !

The first stage of the search - forex shmorks

Since my childhood I have loved math and programming. And when, at the 5th year of IT-university, a colleague told me about Forex , showed him the mathematical essence, I became interested in this matter. And when I saw math at the base of the graphs, I was fascinated and subdued. The only thing is that I did not want to meditate for hours in front of the monitor and frantically catch the moments of entry and exit from the transaction. When I learned about the possibility of creating my own trading strategies, that is, programs that work without my constant presence, I seriously took up research.

Since my childhood I have loved math and programming. And when, at the 5th year of IT-university, a colleague told me about Forex , showed him the mathematical essence, I became interested in this matter. And when I saw math at the base of the graphs, I was fascinated and subdued. The only thing is that I did not want to meditate for hours in front of the monitor and frantically catch the moments of entry and exit from the transaction. When I learned about the possibility of creating my own trading strategies, that is, programs that work without my constant presence, I seriously took up research.Months of labor were spent on all sorts of strategies for catching a sharp trend change (on a virtual account, the result was amazing ... but once in several months of testing). Then more sophisticated systems based on neural networks went into action (it turned out that for a real result, the networks should learn and learn ...). Then there were plans to tackle the optimization of the training of neural networks by genetic algorithms.

I decided to enter into a contract. Yes, I did not have a hundred dollars. But I was happily given the opportunity to work with even ten dollars. When I made a real contract, I was unpleasantly rebuffed by two points in it:

- all my positions are bets on this or that event;

- values of quotes and in general all data can only be those that this broker provides me. Data from other forex firms are not considered.

The first implied that I got into the casino. The second implied that I had to believe only what the croupier told me at my table.

How so??? Forex is a global market for exchanging various currencies! All brokers should have the same pictures (as it happens, by the way, on the stock market)! And what is this - "rates"? I buy and sell currency, and here the rates?

Further careful study of the issue led me to very disappointing conclusions:

- real forex opens with a minimum account of $ 500, and better - a few thousand;

- the rest of the mini, micro, nano-forex - this is just an illusion of forex. Your money does not go beyond the organization providing services in Forex. This organization redistributes money between its customers and its account. Your winnings are a loss to the organization. Your loss is the salary for the organization;

- quotes that come to your computer, gives the organization providing services for Forex. She is quite entitled (technically and legally) to display any picture to you;

- Another unpleasant addition to the previous moment - you wrote your ingenious strategy, launched MetaTrader (or Quik or something else), the strategy opens a deal, and you are waiting for its happy ending. The program is cleverly written, everything is provided. Class! .. But

on the other side of the barricadesin the organization that supplies you with information, professional programmers are sitting. At 90% you can be sure that they know your program. Why? Because its - your strategy - MetaTrader / Quik / ... knows. They can easily transfer its compiled or source code. Knowing your strategy, you can slip such quotes for just one second that a margin call takes place immediately ... I know what I'm talking about, since I kept statistics of quotes for more than a year on 15 currency pairs (a database of millions of records). And I have often met such wonderful strides for a split second, which completely destroy your account - thanks to the leverage; - Speaking of marging call - if at the training stage, a 1: 1000 leverage seemed to be a blessing, then in practice it is a nightmare, which leaves you no chance with a slight unsuccessful market fluctuation;

- studies of the present Forex have shown that the expected value of a currency pair movement in the long term is close to 50% and is 51% ... 54%. Consequently, in the short term, currency movements can be considered random;

- real earnings in Forex are possible either for professional speculators or for fanatical scalpers .

There is another variant of clairvoyance.Both that and another implies serious and long work on self-education, psychology and sitting in front of the monitor.

Everything! I didn’t have a free thousand dollars, I didn’t want to sit in front of the monitor for hours. About Forex, I could forget.

However, like the alchemists, I did not waste a lot of time - I studied neural networks in detail, I understood the statistics, the MetaTrader programming language, working with MySQL, and also studied many issues from the world of finance.

My path, however, lay further.

Anti-Kiyosaki: diversification

Of course, I have studied Kiyosaki up and down. From it I learned a lot of useful things, including a terrible dislike for diversification . But from the institute I also learned critical thinking and the absence of blind faith to the authorities. Why is Kiyosaki against diversification? What is she bad?

Of course, I have studied Kiyosaki up and down. From it I learned a lot of useful things, including a terrible dislike for diversification . But from the institute I also learned critical thinking and the absence of blind faith to the authorities. Why is Kiyosaki against diversification? What is she bad?I was very interested in this question, since I was faced with the fact that real investors are widely using diversification. In the end, I came to this conclusion: diversification greatly reduces your winnings. But it also reduces the risk. If you are a professional and clearly confident in your financial instrument (and this is exactly the case of Kiyosaki), and consider risk to be tending to zero, then you really have no reason to scatter over various financial instruments.

But I am a simple computer programmer who is not well versed in all the tools of the New York Stock Exchange. Moreover, I do not want to understand them much.

Somewhere at the same time, I began to gradually study portfolio theory, which states: the sum of the tools can give a better result than the individual tools that make up its structure.

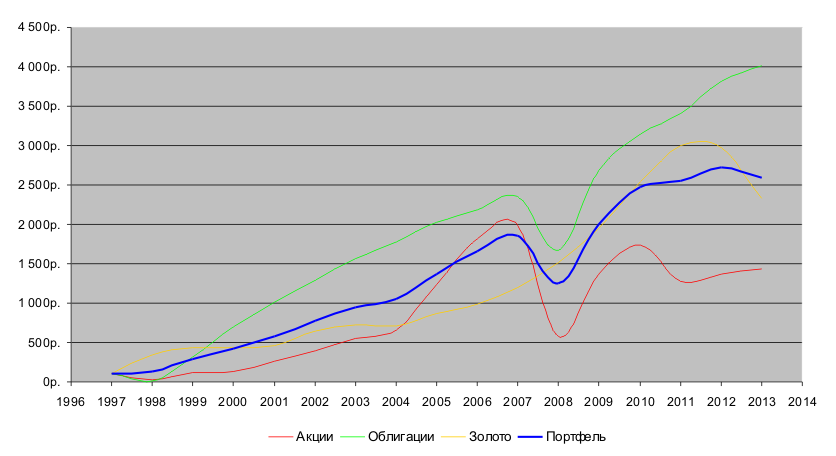

Then I decided to do such a thought experiment: for example, now is the end of 1997. I own 100 rubles. I have access to 3 instruments: 1) Dobrynya Nikitich share fund , 2) Ilya Muromets bond fund, and 3) gold . Consider another 4th option, when I initially divided 100 p. between all these tools equally. Such are the investments. Let's see how these 4 investments will change over time:

| Year | Promotions | Bonds | Gold | Together | |||

|---|---|---|---|---|---|---|---|

| Share price | Amount | Share price | Amount | Share price | Amount | Amount | |

| 1997 | 475.50 p. | 100r. | 584,21 p. | 100r. | 54.40 p. | 100r. | 100r. |

| 1998 | 137,03r. | 29. | 91,95 p. | 16r. | 187,25 p. | 344. | 130r. |

| 1999 | 540,08 p. | 114r. | 1 818,18. | 311r. | 238,62 p. | 439r. | 288r. |

| 2000 | 606,52 p. | 128r. | 4 107,58 p. | 703r. | 233.30 p. | 429r. | 420r. |

| 2001 | 1,253.94 p. | 264r. | 5 897,85 p. | 1 010. | 253,17 p. | 465r. | 580r. |

| 2002 | 1 851.79 p. | 389r. | 7 569,17. | 1 296. | 348.50 p. | 641r. | 775r. |

| 2003 | 2 607,48. | 548r. | 9 159,94. | 1 568. | 393,15 p. | 723r. | 946r. |

| 2004 | 3 116,65. | 655r. | 10 397,10 p. | 1 780. | 388,80 p. | 715r. | 1,050r. |

| 2005 | 5 854,48. | 1 231. | 11 821,31. | 2 023. | 472.35 p. | 868r. | 1 374. |

| 2006 | 8 651,54. | 1 819. | 12,782.30 p. | 2 188. | 535.47 p. | 984r. | 1 664. |

| 2007 | 9 458.50 p. | 1 989 p. | 13 796,38 p. | 2 362. | 654,69 p. | 1 203. | 1 851 p. |

| 2008 | 2 738,07. | 576r. | 9 726,63 p. | 1 665. | 821.80 p. | 1 511. | 1 250r. |

| 2009 | 6 510,21. | 1 369. | 15 676,50. | 2 683. | 1,062,32 p. | 1 953. | 2 002. |

| 2010 | 8 258,51. | 1 737 p. | 18 367,32 p. | 3 144r. | 1,383.06 p. | 2 542. | 2 474. |

| 2011 | 6 041,56. | 1 271. | 19 926,27 p. | 3 411. | 1 629,81. | 2 996. | 2 559. |

| 2012 | 6,483.72 p. | 1 364. | 22 323,24 p. | 3 821. | 1 618,56 p. | 2 975r. | 2 720. |

| 2013 | 6 843,69. | 1 439. | 23 455,99 p. | 4 015. | 1 264,30. | 2 324. | 2 593. |

Well ... If I were a

But I have neither the one nor the other case. I do not want to guess and spend a lot of effort in order to understand where I should invest my money. I want to put them on the account and do a more interesting thing. And what can I tell you - the portfolio in this case would help me a lot! Yes, not stars from the sky, but quite a confident average result.

However, the average is poorly said! Over 16 years, the amount increased 26 times, the average annual yield was 23%, the maximum drawdown of the account was 32%.

What would I have done all these years as part of my investment activities? Nothing . The only thing is that I had to move 1998, 2008 with iron nerves, since my portfolio there was a big deal. Can you imagine a speculator or even more so a scalper, who would have an annual income of 23%, who would withstand a drawdown of his account of 32%? If so, compare his time spent and mine. And remember that nerve cells are not restored.

So I do not understand what diversification is bad for me, a teapot in finance.

Portfolio theory

Traveling further across the expanses of the Internet, I got on William Bernstein’s book Reasonable Asset Distribution . There I first became acquainted with the Markowitz portfolio theory . The essence and its mathematics for a teapot of the type of me can be expressed in simple language (as a matter of fact, this is what asset allocation does).

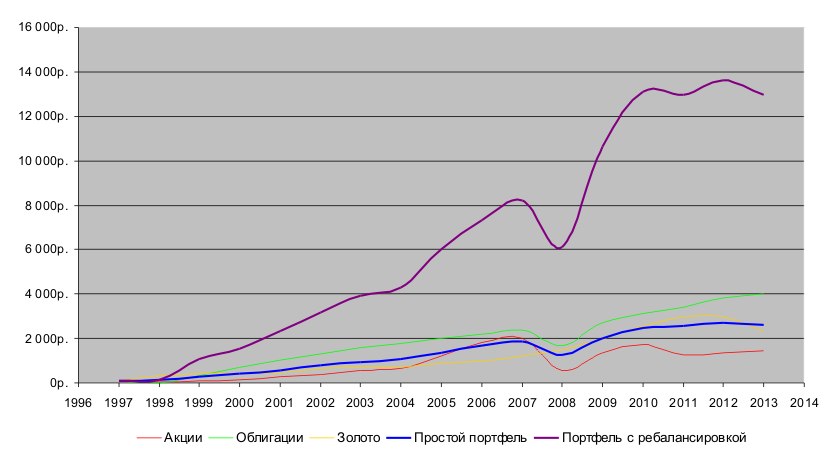

Traveling further across the expanses of the Internet, I got on William Bernstein’s book Reasonable Asset Distribution . There I first became acquainted with the Markowitz portfolio theory . The essence and its mathematics for a teapot of the type of me can be expressed in simple language (as a matter of fact, this is what asset allocation does).Do you remember a good result of our portfolio in stocks, bonds and gold? So, the result can be significantly improved, as well as risk sensitivity can be reduced at the cost of very simple efforts — once a year, change the distribution of money (more precisely, assets) in this portfolio. In science, this is called "rebalancing." See the result:

| Year | Promotions | Bonds | Gold | Simple briefcase | Rebalancing Briefcase |

|---|---|---|---|---|---|

| 1997 | 100,00 rub. | 100,00 rub. | 100,00 rub. | 100,00 rub. | 100,00 rub. |

| 1998 | 28,82 p. | 15.74 p. | 344,21 p. | 129,59 p. | 129,59 p. |

| 1999 | 113,58 p. | 311,22 p. | 438.64 p. | 287,81 p. | 1 068,65. |

| 2000 | 127,55 p. | 703,10 p. | 428,86 p. | 419,84 p. | 1 537,53 p. |

| 2001 | 263.71 p. | 1 009,54 p. | 465,39 p. | 579,55 p. | 2 328.12 p. |

| 2002 | 389.44 p. | 1,295.62 p. | 640.63 p. | 775,23 p. | 3 178,14. |

| 2003 | 548,37 p. | 1 567.92 p. | 722,70 p. | 946,33 p. | 3 929,14 p. |

| 2004 | 655.45 p. | 1 779,69 p. | 714.71 p. | 1,049.95. | 4 303,82 p. |

| 2005 | 1 231,23 p. | 2,023.47 p. | 868,29. | 1,374.33 p. | 6 008,17 p. |

| 2006 | 1 819,46 p. | 2 187,96 p. | 984,32 p. | 1,663.91 p. | 7 321,47. |

| 2007 | 1 989,17 p. | 2 361,54. | 1,203.47 p. | 1 851.40 p. | 8 203,22 p. |

| 2008 | 575,83 p. | 1,664.92 p. | 1 510,66. | 1,250,47. | 6 090,21. |

| 2009 | 1,369.13 p. | 2 683,37. | 1 952,79 p. | 2 001,76 p. | 10 615,69 p. |

| 2010 | 1,736.81 p. | 3 143.96 p. | 2 542,39. | 2 474,38. | 13 109,30. |

| 2011 | 1,270.57. | 3 410,81. | 2 995.97 p. | 2 559,12. | 12 955,89 p. |

| 2012 | 1 363,56 p. | 3 821,10 p. | 2 975,29. | 2 719,98 p. | 13 624.03 p. |

| 2013 | 1,439.26 p. | 4,014,99 p. | 2 324,08. | 2 592,78. | 12 981.49 p. |

For 16 years, the amount has increased 130 times, the average annual yield was 36%, the maximum drawdown - 26%.

Effort - once a year to calculate according to simple formulas that where (10 minutes), give the order to the broker (another 15 minutes) - that's all. You see the result yourself. What else can I say? Only the fact that so many years have passed by, for which it would be great to increase capital ... However, life is not over yet (I hope), what else can be done (I hope even more). So emotions aside.

How did it happen? What is the magic?

The magic is that from time to time the composition of the portfolio changes in order to buy the depreciating assets, which have become more expensive to sell. This reduces the overall risk of the portfolio and, as you can see, increase its profitability.

The technique here is simple. We initially decided to invest one-third into stocks, one-third into bonds, and the remainder into gold. Take, for example, the end of 1997 - 33.33 p on stocks, 33.33 p on bonds and 33.33 p on gold. A year has passed, and now our shares have fallen in price - now there is 9.61 rubles, bonds have dropped even steeper - 5.25 rubles, but gold has grown - 114.74 rubles. Despite everything, our portfolio has slightly grown - now it is 129.59 rubles. What does common sense require? Throw cheap assets, buy gold going up. So it comes

We do exactly the opposite. We will continue to follow the rule of 1/3 for each asset. 129.59r / 3 = 43.19r (I’m sacrificing the accuracy of the least significant digits a bit, since there are a lot of decimal places). So, on the account of each asset should lie 43.19 p. How to achieve this? Sell gold in the amount of 71.55 rubles (114.74 rubles - 71.55 rubles = 43.19 rubles). Then add 33.59 shares (9.61 + 33.59 = 43.19) and add to bonds 37.95 (5.25 + 37.95 = 43.19). If you told your friends about it in those days, they would quickly hide you far away! But next year, they would have gnawed on everything that they could ...

That's so simple! In theory…

... and her practice

What is “rebalancing”? When and how? What kind of assets to recruit? What kind...? What do you need...? Where is ...?

What is “rebalancing”? When and how? What kind of assets to recruit? What kind...? What do you need...? Where is ...?In general, it is time to collect specific information. Bernstein, Markowitz, Kiyosaki is good, but it is a wild West. How to apply this knowledge in our civilized East?

Here now and trample on. More precisely, I accumulate funds and study the theory in detail.

Where to get funds for all this activity? I really enjoyed this lecture . Or rather, the “Simple Mathematics” section. It shows simple calculations of how an investment of $ 100 is growing from 20% profit per year (as you have seen, this is more than realistic). After 51 years, this amount will exceed $ 1 million. And if this amount is increased annually with additional injections ( the same 10% of the salary ), then it will take much less time. Having personally read this first lecture, I immediately ran to the bank and opened several deposits (at that time I didn’t have a portfolio theory). As I become smarter - I will invest in more serious financial instruments.

How often do rebalancing? Most sources advise doing it once a year - no more and no less.

In what proportion to collect assets?

There is a sea of mathematics ... Formulas are simple - in particular, we recall the expectation, the variance of a random variable and the covariance. Excel and his ilk allow you to perform all complex calculations easily and quickly, in various combinations.

The mathematical expectation of annual profit (expressed in%) will give us "profitability", the variance of annual profit (I turn it into a standard deviation - it is somehow more visual for me ...) - "risk", covariance (according to monthly data) - the dependence of tools on each other. Those tools that show high dependency are not suitable for portfolio theory. It is better not to consider them at all.

For those interested and ready for calculations. Take the tools you are interested in (those that I took, for example). Upload data to a spreadsheet. Calculate from them the arithmetic mean and variance. Then you form all sorts of combinations - say, 10% of gold, 50% of bonds and 40% of shares. For each such combination, consider the profitability and risk.

Finally, you can choose what you need. As a rule, high returns are accompanied by high risk. You find the combination that is most comfortable for you. And according to this proportion you start working.

It is necessary to take into account - the portfolio theory works for a long time (a dozen years - this is not much). So, the chosen proportion will have to comply with the whole period.

You also need to remember that future combinations are weakly related to history. This also needs to be kept in mind.

In general, here for me the most questions. I try, I drive different models, I study ... If there are interesting results and interest of the readership, I will write in some detail.

And the main question - how wide should be diversification ? Different fin. instruments? Yes, but it should be wider. There must be tools not only in our country, but also abroad - remember, 1917? Before him, it was necessary to invest in the assets of the St. Petersburg Stock Exchange. Only in a year all your money would evaporate ... This can happen now. For example, Yukos shares are the same asset that could destroy your portfolio. So his advice is the wider the better.

Conclusion

I went the following way:

- I refused consumer loans - it was easy for me, since I didn’t have time to get hooked on them, and my second loan turned out to be such a pretty penny that I now fear them as fire. However, the fire is useful. Therefore, my attitude to loans is: a loan is a powerful but very dangerous financial tool, and should be used with great skill . As well as antibiotics - their correct application saves, and if they are "shyryatsya", then they will destroy you;

- I began to postpone 10% of the profits - I already wrote about this and mentioned earlier . In a nutshell - with every profit (except donated money) I save 10% in the piggy bank. For the year I get more than one salary. This money is inviolable and is used only for investment purposes (or some reserve amount is accumulated first, then everything is spent only on investments). So you can periodically, without significant damage to your finances to replenish investments;

- invested in several deposits - put money in several banks at high interest rates for an average (9 months) term. Why different banks? Because the deposits are risky - there is a possibility that not all the money will be able to be withdrawn (this has not happened yet);

- I keep a financial report - this has already become a habit for me. In the evening I write down everything in detail. As a result, I found small financial holes. Now I clearly know how much and what I need money for. Along the way, made friends with statistics. Useful!

- I raise my theoretical level - I spend time and money on studying financial theories. I also study the financial instruments I plan to use;

- I make researches - I try, I drive different models. For deposits are good (low risk), but weak (small profitability). In fact, this is a reserve for me, I am preparing for more serious investments;

- Constantly constructing their global goals - an important point! Why save money? How much do I need them? How do I plan to withdraw funds? Will I continue to invest after the "retirement"? When will this happen? What if some assets burn out?

Now I have the level of deposits and deferred "urgent" funds. For the future I plan to save up money for investing in more serious instruments. By that time, I hope to confidently navigate in all the necessary issues.

I am very sorry that so much time has passed by. I am even more glad that there is much more time ahead!

I wish you financial success!

Source: https://habr.com/ru/post/231797/

All Articles