Illustrious Russian accountant. He also improved the scores

If a person who understands accounting, to ask who is the most famous Russian accountant, the answer will follow immediately: Fedor Venediktovich Yezersky . And this is true - for the reasons that will be named below.

Despite the fact that there are a lot of biographical materials on the Network in Yezersky, I post his illustrated biography on Habré. Let the broad masses of habravchan, from a number far from accounting, learn about the fate of an extraordinary and controversial person who:

- created a new information technology called triple Russian accounting;

- is the inventor of the computing device - accounts of the original design.

So, Fedor Venediktovich Yezersky.

')

1. Childhood

Nobleman.

Born February 17, 1835, in the family estate of Zalesovichi, Rogachev district, Mogilev province.

Got a home education. Here the information varies: according to other sources, he graduated from the Chernihiv district school.

His uncle, Grigory Frantsevich Yezersky , who worked as manager of the accounting and control department of the Ministry of War, instilled a love for bookkeeping to the young Fedor. In those days it was a very, very high position. Or maybe the uncle's profession predetermined the choice of a young man for the sphere of activity - now it is already impossible to say.

2. Public service

In 1853 (according to other sources in 1856) Fyodor Venediktovich got a job as a scribe in the Mogilev Chamber of a civil court. Then he stayed in the public service in various institutions and in various positions:

1861 - was seconded to the Warsaw intendance of the First Army to establish new forms of accounting in the regiments. At the same time he submitted an essay on the topic “Manual on Agricultural Accounting” to a competition organized by the academic committee of the Ministry of State Property;

1862 - in Astrakhan, he audited the food department, was a member of the investigative commission on the case of abuse in the Tsaritsyn food store;

1864-65 - was a member of the Interim Commission to draw up a regulation on material accounting;

1867 - Audited various departments of the military department in Tver and Vilna.

In one of his works, Fyodor Venediktovich referred to “official duties consisting in auditing the most diverse reports since 1855, such as old reports: - on troop food, rafting bread through Astrakhan to the Caucasus, on Sevastopol and other shops, women's institutions; and new reporting: - on the collection of state revenues of the Tver province, the expenses of the Ministry of Finance in the same province, reporting in six provinces of the Vilna military district, according to the departments: engineering, artillery, medical, military schools, etc. ”.

3. Triple Accounting

In 1868, Fedor Venediktovich Yezersky retired - at the age of 33, by the way! - and went to Dresden, where he studied bookkeeping, simultaneously collecting a library of accounting literature in all languages.

On March 28, 1870, an article entitled Russian Triple System was published in the Moskovskie Vedomosti newspaper. In the same year, the first book on triple bookkeeping, entitled “The First Public Experience of the New System,” was published in Dresden, after which the works of Fyodor Venediktovich began to appear, in Russia and abroad. There were many, many: books on triple bookkeeping were published one after another for over 45 years.

What was Yezersky's invention? New form of bookkeeping. Under the form of accounting then understood the form of accounting books and the rules for transferring indicators from one book to another.

I will give the floor to the inventor himself, for - who better than him will convey the essence of his creation? A small excerpt - under the spoiler, so that those who are not interested in information technology in the field of accounting, can safely skip it.

F.V. Yezersky - about his system

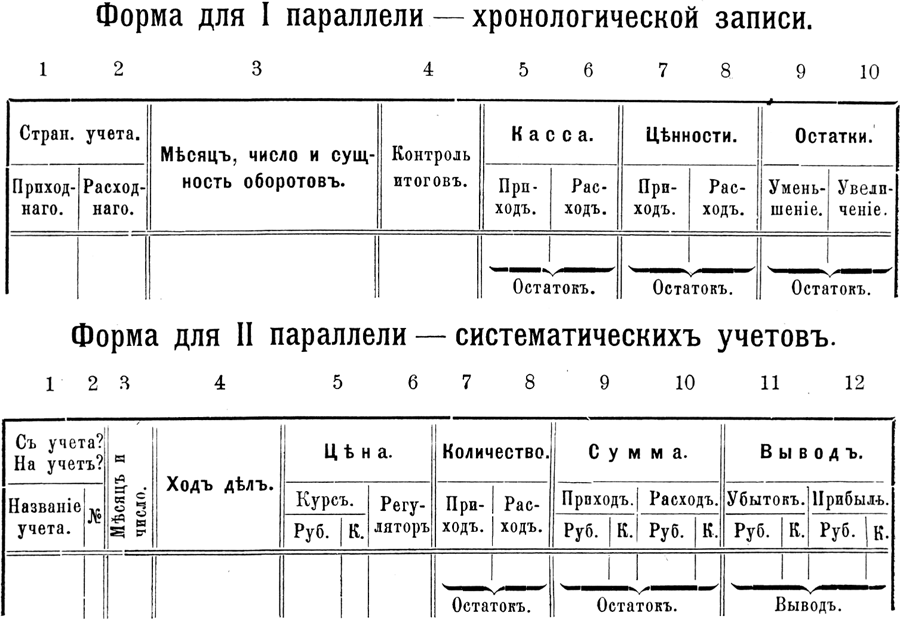

If we define the essence of any accounting system by the number of parallel records, then the essence of the proposed system should be the distribution of its records in three parallels.

I. Chronological,

Ii. Systematic

Iii. Consolidated.

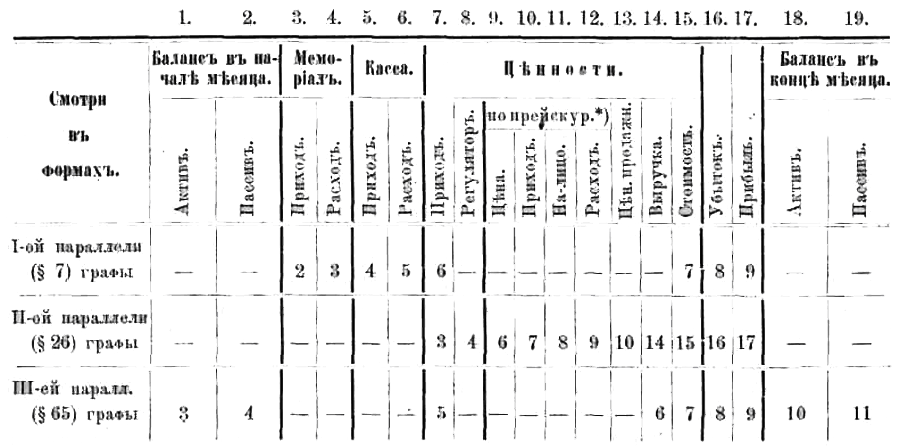

The peculiarity of the new system's system is in a peculiar, only inherent in it, the separation of amounts by books, bills and graphs, bringing them together according to the results and the subordination of all the results to 19 non-deceptive signs of loyalty.

The construction of the proposed system is based on the following 19 columns.

The brevity of the proposed system and the subordination in it to the control of all the figures essential in commercial accounting give it the following advantages over existing systems.

1) Elimination of the possibility of hiding errors and deceptions. Descriptions and errors, of whatever kind, they will inevitably produce discord in the results and conclusions - on the same page where they happened, or on the closest pages to it; this discord not only reveals existence near an error, but also indicates its magnitude.

Consequently, the new system eliminates any possibility of hiding both errors occurring as a result of an oversight, and frauds produced by wrong conclusions.

2) The ease and speed of error detection. Errors can be assumed only in those columns in the results of which the absence of the required agreement is noted; therefore, there is no need to look for them where such agreement exists. The above 19 columns are connected, as it were, into one musical chord: as in a chord, the discrepancy of one tone with the others produces a dissonance, just as here the discrepancy between one column and the output with the others produces a sensitive disorder; as in the first case, the tone that produces the dissonance is highlighted, so in the second, the column or conclusion that produces the discord is highlighted. This makes it possible to always immediately determine the location of the error and the very nature of it; in a word - all kinds of mistakes are opened easily and quickly.

According to the double system, one cannot predict either the place or the nature of the errors, and in order to find them, one has either to revise all the bookkeeping, or to look for mistakes in it at random.

3) Ease of control . The complete agreement of all the mentioned results guarantees the inerrancy of all accounting, and the conviction of such inerrancy is obtained in a short time, the necessary

only to find the said consent.

According to the double system, in order to obtain a belief in the loyalty of bookkeeping, it is necessary to resort to tedious and lengthy, and therefore open in turn for errors, verification of all component parts through.

4) Loss clarity. All cases that caused damage or loss to a trading house are highlighted in one column of loss, which is visible in all three parallels, and no such case can escape from the attentive eye.

5) Clarity of profits. In the same way, all happy occasions stand out in one prominent graph of profit - in such a way that the attentive eye can see in it the totality of all profits in their chronological, systematic and reporting manner.

In the forms of existing systems there are no special graphs for loss and profit, and therefore there is no place for designating the course of the increment or decline of merchant capital in historical order. Losses and profits are shown in them only at the year-long conclusion of books as a result - after deducting from the total amount of loss all private profits, and vice versa. Moreover, the sum of the total result of loss and profit varies arbitrarily due to the existing custom of taking inventory prices for inventory.

6) Ease of identifying capital figures. The difference between the results of income and expenditure in the capital books, in the cash department, indicates the state of cash, and the same in the department of values - the state of all values; their sum indicates the amount of net capital at a given time. Therefore, the sum of the latter can be found at any desired time, in a few minutes.

The same amount of net capital can be obtained in another way: the difference between the arrival and expense transport in the memorial department indicates the amount of capital invested in the trade, and the difference between the loss and profit graphs is the result of the trading turnovers; the figure of the first together with the result of profits or minus the amount of losses gives the figure of net capital.

Both of these conclusions serve one another.

None of the existing systems provide these results.

7) Ease of reviewing bookkeeping in its whole. The columns listed above give space to all the essential figures of all the turns and are distributed in them either privately or in general; Not a single figure or amount is hidden, unbalanced or obscured by another. Thus, the accounting of a new system presents, as it were, a photograph of all trading cases, either individually (each account), then in private groups (a book of detailed monthly totals, profits and balances), then in a general group (summary book of total monthly totals, profits and balances ) - in such a clear picture, from which, transferring the gaze from the general to the parts and to the particular, and vice versa, one can see everything that only the inquiring mind of a person is able to demand from the past trading turnarounds to discuss them and for considerations regarding further directions and development of bargaining.

Even the unfilled places remaining in the book of monthly totals of profits and balance sheets eloquently indicate scores for which there was no turnover at all during certain months of revolutions, and thereby warn the owner against the false direction of bargaining.

In the adopted systems, as already noted, there are no special columns for loss and profit, and therefore are not visible either in chronological or systematic order of development of commercial capital.

8) Reduction of labor. When trading at list prices, the time spent on keeping track of the new system can be reduced to a few minutes a day, or even a week, and then a few hours after the end of the month. This reduction in labor, which does not violate the accuracy of bookkeeping, is achieved by using accounts for interest capes.

This method of account management has not existed until now in any system.

9) Ease of work. In comparison with existing systems, the proposed offers the following significant reliefs.

a) All bookkeeping is limited to three forms: 1) For the capital book, 2) for systematic accounts and 3) for the summary book - therefore it does not burden the accountant with a variety of forms.

b) For each digit of the sums there is a special graph in the forms, which achieves the visibility of the forms.

c) All columns are arranged in the order of their mutual relationship, which facilitates their comparison.

d) Freedom is allowed in the compilation of the text - the accountant is not constrained by any conditional forms and terms.

e) Next to the text there are columns “memorial” and “revenue”, intended for placing figures quickly, so that with the rest of the more difficult work you can expect free time and execute it at your leisure when attention is not diverted by other matters.

The essence of the new system

If we define the essence of any accounting system by the number of parallel records, then the essence of the proposed system should be the distribution of its records in three parallels.

I. Chronological,

Ii. Systematic

Iii. Consolidated.

Build a new system

The peculiarity of the new system's system is in a peculiar, only inherent in it, the separation of amounts by books, bills and graphs, bringing them together according to the results and the subordination of all the results to 19 non-deceptive signs of loyalty.

The construction of the proposed system is based on the following 19 columns.

Advantages of the new system

The brevity of the proposed system and the subordination in it to the control of all the figures essential in commercial accounting give it the following advantages over existing systems.

1) Elimination of the possibility of hiding errors and deceptions. Descriptions and errors, of whatever kind, they will inevitably produce discord in the results and conclusions - on the same page where they happened, or on the closest pages to it; this discord not only reveals existence near an error, but also indicates its magnitude.

Consequently, the new system eliminates any possibility of hiding both errors occurring as a result of an oversight, and frauds produced by wrong conclusions.

2) The ease and speed of error detection. Errors can be assumed only in those columns in the results of which the absence of the required agreement is noted; therefore, there is no need to look for them where such agreement exists. The above 19 columns are connected, as it were, into one musical chord: as in a chord, the discrepancy of one tone with the others produces a dissonance, just as here the discrepancy between one column and the output with the others produces a sensitive disorder; as in the first case, the tone that produces the dissonance is highlighted, so in the second, the column or conclusion that produces the discord is highlighted. This makes it possible to always immediately determine the location of the error and the very nature of it; in a word - all kinds of mistakes are opened easily and quickly.

According to the double system, one cannot predict either the place or the nature of the errors, and in order to find them, one has either to revise all the bookkeeping, or to look for mistakes in it at random.

3) Ease of control . The complete agreement of all the mentioned results guarantees the inerrancy of all accounting, and the conviction of such inerrancy is obtained in a short time, the necessary

only to find the said consent.

According to the double system, in order to obtain a belief in the loyalty of bookkeeping, it is necessary to resort to tedious and lengthy, and therefore open in turn for errors, verification of all component parts through.

4) Loss clarity. All cases that caused damage or loss to a trading house are highlighted in one column of loss, which is visible in all three parallels, and no such case can escape from the attentive eye.

5) Clarity of profits. In the same way, all happy occasions stand out in one prominent graph of profit - in such a way that the attentive eye can see in it the totality of all profits in their chronological, systematic and reporting manner.

In the forms of existing systems there are no special graphs for loss and profit, and therefore there is no place for designating the course of the increment or decline of merchant capital in historical order. Losses and profits are shown in them only at the year-long conclusion of books as a result - after deducting from the total amount of loss all private profits, and vice versa. Moreover, the sum of the total result of loss and profit varies arbitrarily due to the existing custom of taking inventory prices for inventory.

6) Ease of identifying capital figures. The difference between the results of income and expenditure in the capital books, in the cash department, indicates the state of cash, and the same in the department of values - the state of all values; their sum indicates the amount of net capital at a given time. Therefore, the sum of the latter can be found at any desired time, in a few minutes.

The same amount of net capital can be obtained in another way: the difference between the arrival and expense transport in the memorial department indicates the amount of capital invested in the trade, and the difference between the loss and profit graphs is the result of the trading turnovers; the figure of the first together with the result of profits or minus the amount of losses gives the figure of net capital.

Both of these conclusions serve one another.

None of the existing systems provide these results.

7) Ease of reviewing bookkeeping in its whole. The columns listed above give space to all the essential figures of all the turns and are distributed in them either privately or in general; Not a single figure or amount is hidden, unbalanced or obscured by another. Thus, the accounting of a new system presents, as it were, a photograph of all trading cases, either individually (each account), then in private groups (a book of detailed monthly totals, profits and balances), then in a general group (summary book of total monthly totals, profits and balances ) - in such a clear picture, from which, transferring the gaze from the general to the parts and to the particular, and vice versa, one can see everything that only the inquiring mind of a person is able to demand from the past trading turnarounds to discuss them and for considerations regarding further directions and development of bargaining.

Even the unfilled places remaining in the book of monthly totals of profits and balance sheets eloquently indicate scores for which there was no turnover at all during certain months of revolutions, and thereby warn the owner against the false direction of bargaining.

In the adopted systems, as already noted, there are no special columns for loss and profit, and therefore are not visible either in chronological or systematic order of development of commercial capital.

8) Reduction of labor. When trading at list prices, the time spent on keeping track of the new system can be reduced to a few minutes a day, or even a week, and then a few hours after the end of the month. This reduction in labor, which does not violate the accuracy of bookkeeping, is achieved by using accounts for interest capes.

This method of account management has not existed until now in any system.

9) Ease of work. In comparison with existing systems, the proposed offers the following significant reliefs.

a) All bookkeeping is limited to three forms: 1) For the capital book, 2) for systematic accounts and 3) for the summary book - therefore it does not burden the accountant with a variety of forms.

b) For each digit of the sums there is a special graph in the forms, which achieves the visibility of the forms.

c) All columns are arranged in the order of their mutual relationship, which facilitates their comparison.

d) Freedom is allowed in the compilation of the text - the accountant is not constrained by any conditional forms and terms.

e) Next to the text there are columns “memorial” and “revenue”, intended for placing figures quickly, so that with the rest of the more difficult work you can expect free time and execute it at your leisure when attention is not diverted by other matters.

In comparison with other systems, commented on the triple Russian accounting a lot, but very differently, as if the subject of attention of commentators were different methodologies. Those who are interested in the triple system can familiarize themselves with my interpretation - under the spoiler.

My opinion on triple bookkeeping is an excerpt from the reader An idea and insights into Russian bookkeeping

I have not seen a single, in my opinion, correct interpretation of the Yezersky triple system, although the author himself only asserted this. Commentators usually focus on signs of loyalty to the ternary system, i.e. ways of arithmetic verification of proposed books, or on the number of books, or on the accounting entries performed in the triple system, while its content, in my opinion, lies entirely differently.

The content of the triple system consists in putting the accounts of the financial results - conclusions, in Fyodor Venediktovich's expression - in a separate column, thus achieving the separation of property accounts from dummy used in traditional double-entry bookkeeping. “Increase or decrease in financial result is not the receipt or expenditure of property. These values cannot be placed in books together! ”- that, in our opinion, Fyodor Venediktovich tried to inform the city and the world.

Unfortunately, this thought was not F.V. Yezersky developed, otherwise his triple bookkeeping, taking into account the performance and penetration of its inventor, could get a fundamentally different form from double bookkeeping not only by name, but also by methodological essence - one can only guess which one. For example, shifting the triple bookkeeping column “Withdrawal”, denoting profit or loss (ie, equity), into the system of accounts while retaining the original names of the parties to the account “Lost” and “Profit” (better, of course, “Loss” and “ Profit ”), at the name of the parties to the property accounts“ Income ”and“ Expenditure ”, would give a completely different - it is possible, more accessible to understanding - accounting methodology.

Imagine that instead of the current medieval (or even earlier) “Debit” and “Loan”, the names of the parties for property accounts are “Income” and “Expenditure” (which corresponds to “Debit” and “Loan”), however : “Loss” and “Profit”.

F.V. Yezerskiy, in the spirit of his time, did not focus on receivables and payables (in the terminology of that time, personal accounts), although, of course, he was familiar with the problem. If the author of the triple bookkeeping found the strength to step further, it would inevitably come to the conclusion that the sides of personal accounts also mean not the receipt and expenditure of property, but something else, for which reason the parties to these accounts also need to be titled differently, for example “Borrowed” and “Debt repaid”.

In this case, the wiring would look different than now - for example:

1. Borrowed:

The arrival of "Money", 30-00

Borrowed "Face A". 30-00

2. Purchased goods:

Parish "Thing 1", 30-00

Consumption "Money." 30-00

3. Goods sold with deferred payment:

Borrowed "Face B", 40-00

Consumption "Thing 1", 30-00

Profit "Capital 1" 10-00

4. Received debt from the buyer:

The arrival of "Money", 40-00

Repaid debt "Face B". 40-00

5. The debt is returned to the creditor:

“Face A” debt repaid, 30-00

Consumption "Money." 30-00

These transactions demonstrate the development of the simplest trading operation: the farm takes 30 rubles, for which it buys the goods, and then sells it, with a deferred payment, for 40 rubles, after which it pays the creditor, remaining 10 rubles in gain.

Due to the fact that each action in relation to the four types of objects (property, receivables and payables, equity) is named in a special way, the accountant will not be confused what this or that entry means, as it is confused when all types of objects have two identical sides of the account : "Debit" and "Credit". In fact, what is “Debt - Credit Money” (which debt, receivables or payables? Why debit? - you need to think), it is much clearer: “The debt of the Individual is repaid - Expense Money” (the debt in the face is repaid, because the money is given) . The given technique naturally follows from the idea of F.V. Yezersky about the "clarity of profit and loss", although they are not described in this form. And if it had been stated, how to know if there was a triple in the place of modern double-entry bookkeeping?

The content of the triple system consists in putting the accounts of the financial results - conclusions, in Fyodor Venediktovich's expression - in a separate column, thus achieving the separation of property accounts from dummy used in traditional double-entry bookkeeping. “Increase or decrease in financial result is not the receipt or expenditure of property. These values cannot be placed in books together! ”- that, in our opinion, Fyodor Venediktovich tried to inform the city and the world.

Unfortunately, this thought was not F.V. Yezersky developed, otherwise his triple bookkeeping, taking into account the performance and penetration of its inventor, could get a fundamentally different form from double bookkeeping not only by name, but also by methodological essence - one can only guess which one. For example, shifting the triple bookkeeping column “Withdrawal”, denoting profit or loss (ie, equity), into the system of accounts while retaining the original names of the parties to the account “Lost” and “Profit” (better, of course, “Loss” and “ Profit ”), at the name of the parties to the property accounts“ Income ”and“ Expenditure ”, would give a completely different - it is possible, more accessible to understanding - accounting methodology.

Imagine that instead of the current medieval (or even earlier) “Debit” and “Loan”, the names of the parties for property accounts are “Income” and “Expenditure” (which corresponds to “Debit” and “Loan”), however : “Loss” and “Profit”.

F.V. Yezerskiy, in the spirit of his time, did not focus on receivables and payables (in the terminology of that time, personal accounts), although, of course, he was familiar with the problem. If the author of the triple bookkeeping found the strength to step further, it would inevitably come to the conclusion that the sides of personal accounts also mean not the receipt and expenditure of property, but something else, for which reason the parties to these accounts also need to be titled differently, for example “Borrowed” and “Debt repaid”.

In this case, the wiring would look different than now - for example:

1. Borrowed:

The arrival of "Money", 30-00

Borrowed "Face A". 30-00

2. Purchased goods:

Parish "Thing 1", 30-00

Consumption "Money." 30-00

3. Goods sold with deferred payment:

Borrowed "Face B", 40-00

Consumption "Thing 1", 30-00

Profit "Capital 1" 10-00

4. Received debt from the buyer:

The arrival of "Money", 40-00

Repaid debt "Face B". 40-00

5. The debt is returned to the creditor:

“Face A” debt repaid, 30-00

Consumption "Money." 30-00

These transactions demonstrate the development of the simplest trading operation: the farm takes 30 rubles, for which it buys the goods, and then sells it, with a deferred payment, for 40 rubles, after which it pays the creditor, remaining 10 rubles in gain.

Due to the fact that each action in relation to the four types of objects (property, receivables and payables, equity) is named in a special way, the accountant will not be confused what this or that entry means, as it is confused when all types of objects have two identical sides of the account : "Debit" and "Credit". In fact, what is “Debt - Credit Money” (which debt, receivables or payables? Why debit? - you need to think), it is much clearer: “The debt of the Individual is repaid - Expense Money” (the debt in the face is repaid, because the money is given) . The given technique naturally follows from the idea of F.V. Yezersky about the "clarity of profit and loss", although they are not described in this form. And if it had been stated, how to know if there was a triple in the place of modern double-entry bookkeeping?

For many years, the triple Russian accounting was in the center of public attention, it was actively discussed: many criticized it, and not without scandals - I would say, the discussion and promotion of F.V. Yezersky was one big scandal, because the author encroached on the main accounting shrine: a double entry. The scandalous ups and downs that accompanied the discussions do not cite and I don’t focus on them at all, because otherwise the short post will become completely unreadable.

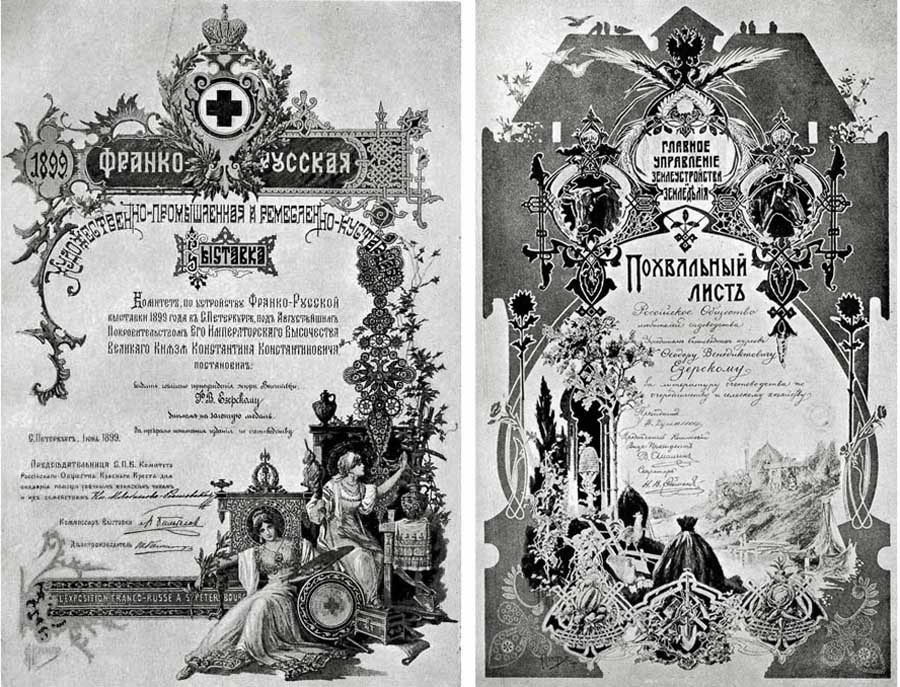

In addition to scandals, there was recognition, including at the international level - this is clearly shown by the diplomas, medals and commendations received by Yezersky. He himself did not produce them, after all!

Not all Yezersky awards: only some of them were copied. The rest is not mastered - as they say, "the hand of fighters stabbed tired."

4. Jezersky bills

Returning to the biography.

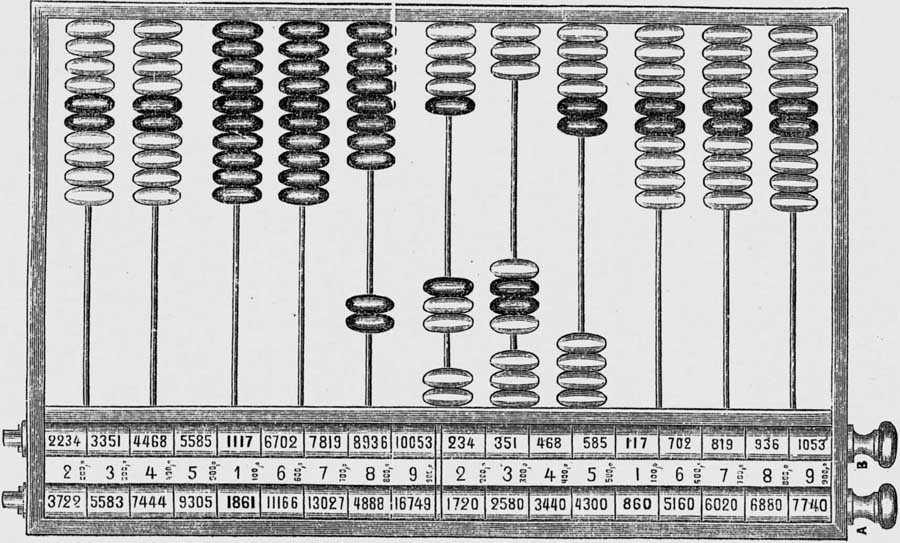

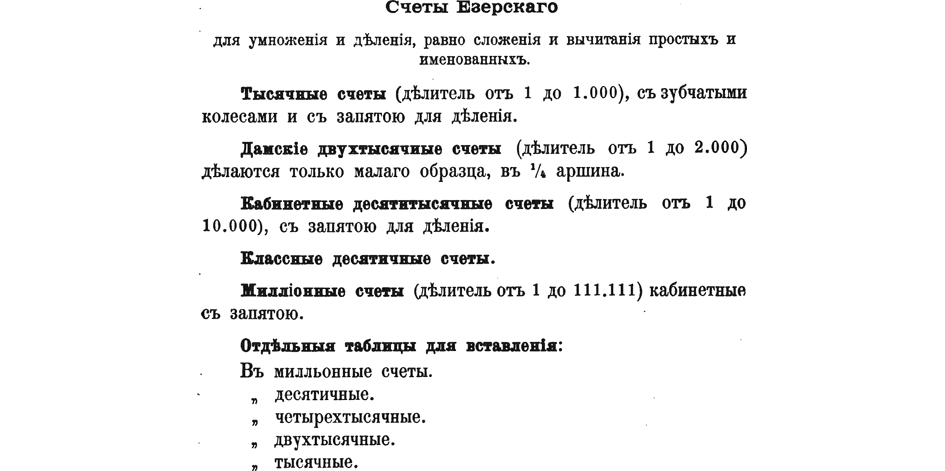

In 1872, Fedor Venediktovich improved Russian abacus, which is known to all who were interested in the history of this computing device. Here they are, the scores of Yezersky .

Two years later, the Department of Manufactures and Commerce issued to the collegiate assessor Fyodor Yezersky an official privilege on "a machine for multiplication and division." It is curious that it was possible to get a patent in the United States a year earlier. Those interested can familiarize themselves with the translation - is under the spoiler.

American patent for the jetsky abacus

Theodor Yezersky, St. Petersburg, Russia

Advanced Computing Device

This technical description is part of patent certificate No. 144523 of November 11, 1873, the application was filed on August 21, 1873.

Anyone who can touch:

I, Theodor Yezersky, St. Petersburg, Russia, improved the computing device, in which the following technical description is made.

In fig. 1 the device is shown on the front side, in fig. 2 (- line) - from the side.

The device allows you to easily and quickly carry out multiplication and division, and consists of a paper strip containing numerical rows, and two rollers, on which this paper strip is wound, also a fixed scoreboard.

Parallel rollers, labeled A and B in the figure, are made of wood or another suitable material and securely fastened. A strip of paper or cloth, denoted as D, is wound on the rollers, numerical rows are printed on the strip, the rollers rotate in opposite directions so that both the front and the wrong sides of the strip can be observed, as shown in fig. 2. The letter E denotes a plate, the ends of which are fixed in frame C and which shields the numerical rows on the paper strip D. The numbers from 1 to 9 are printed on the surface of the plate E, one or several times. The numbers correspond to the paper strip D in such a way that the numerical series on D, corresponding to the unit on E, are factors for other numbers in the corresponding rows D. The number 674, located above the edge of the plate E, is a factor of the numbers of the same horizontal row of the strip D. Thus, the number 1348 on D means that 2 x 674 = 1348; the number 2022 means that 3 x 674 = 2022, etc., actions in other rows are made in the same way. E , , .

, D E, , , . . , .

, , F, G.

.

B , D E, .

16 1872 .

.

:

, .

PS , . - , . 1874 .:

United States Patent Office

Theodor Yezersky, St. Petersburg, Russia

Advanced Computing Device

This technical description is part of patent certificate No. 144523 of November 11, 1873, the application was filed on August 21, 1873.

Anyone who can touch:

I, Theodor Yezersky, St. Petersburg, Russia, improved the computing device, in which the following technical description is made.

In fig. 1 the device is shown on the front side, in fig. 2 (- line) - from the side.

The device allows you to easily and quickly carry out multiplication and division, and consists of a paper strip containing numerical rows, and two rollers, on which this paper strip is wound, also a fixed scoreboard.

Parallel rollers, labeled A and B in the figure, are made of wood or another suitable material and securely fastened. A strip of paper or cloth, denoted as D, is wound on the rollers, numerical rows are printed on the strip, the rollers rotate in opposite directions so that both the front and the wrong sides of the strip can be observed, as shown in fig. 2. The letter E denotes a plate, the ends of which are fixed in frame C and which shields the numerical rows on the paper strip D. The numbers from 1 to 9 are printed on the surface of the plate E, one or several times. The numbers correspond to the paper strip D in such a way that the numerical series on D, corresponding to the unit on E, are factors for other numbers in the corresponding rows D. The number 674, located above the edge of the plate E, is a factor of the numbers of the same horizontal row of the strip D. Thus, the number 1348 on D means that 2 x 674 = 1348; the number 2022 means that 3 x 674 = 2022, etc., actions in other rows are made in the same way. E , , .

, D E, , , . . , .

, , F, G.

.

B , D E, .

16 1872 .

.

:

, .

PS , . - , . 1874 .:

Yezersky's bills were made for sale, and in different versions.

This counting device could not achieve wide success with users, so it remained in the history of computing technology.

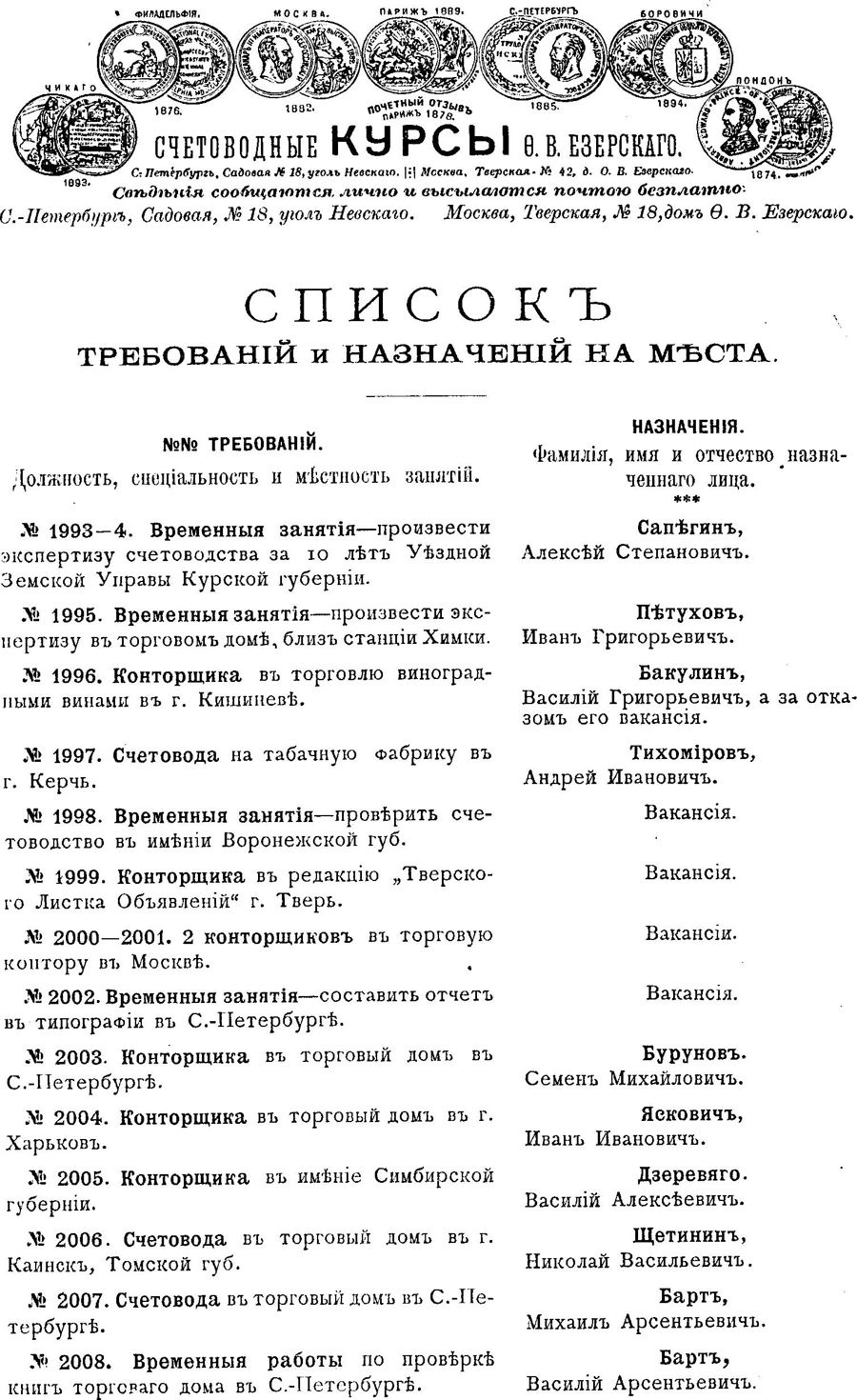

5. Counting courses

In 1874, Fyodor Venediktovich founded bookkeeping courses . This ambitious person was not interested in the work of a desk scientist, he was an entrepreneur to the core, aiming at using his labors to make money. Initially, courses opened in St. Petersburg, and since 1887 in Moscow and in several other cities of the Russian Empire. Not the first and not the largest accounting courses in Russia, at the same time one of the first and one of the largest.

Building accounting courses Ezerskogo in Moscow (Tverskaya str., House Khomyakov):

Another building in Moscow. It is not clear whether there is a mistake or whether the Moscow branch of the Yezersky course had two buildings. Generally, in the ads of Yezersky and his firms from various years, buildings on Tverskaya number 16, 18 and 42 appear.

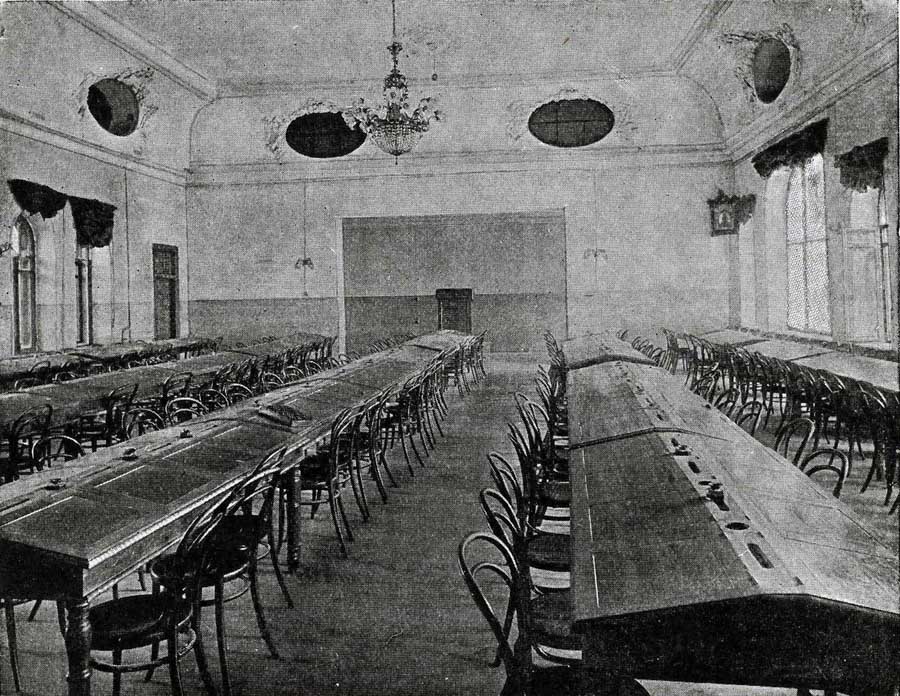

Auditoriums accounting courses Ezerskogo:

Library reading book-accounting courses Ezerskogo:

Statistical data on courses:

Accounting courses F.V. Yezersky not only earned money on training, but also employed graduates.

Advertisements:

6. Literary activity

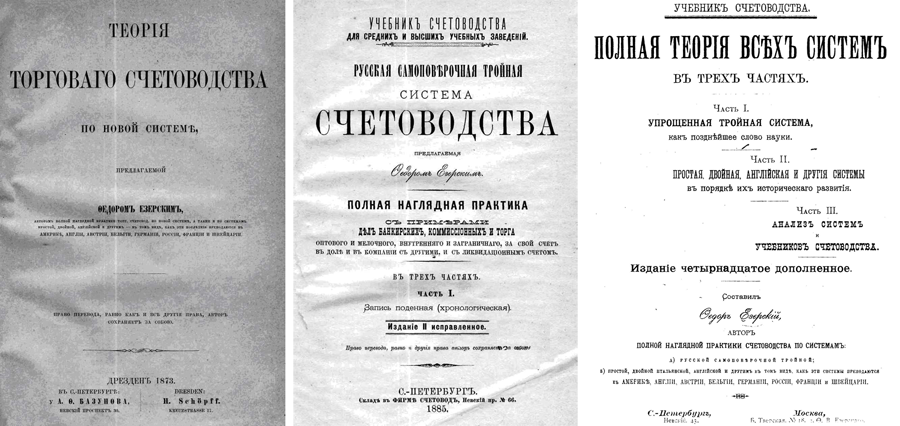

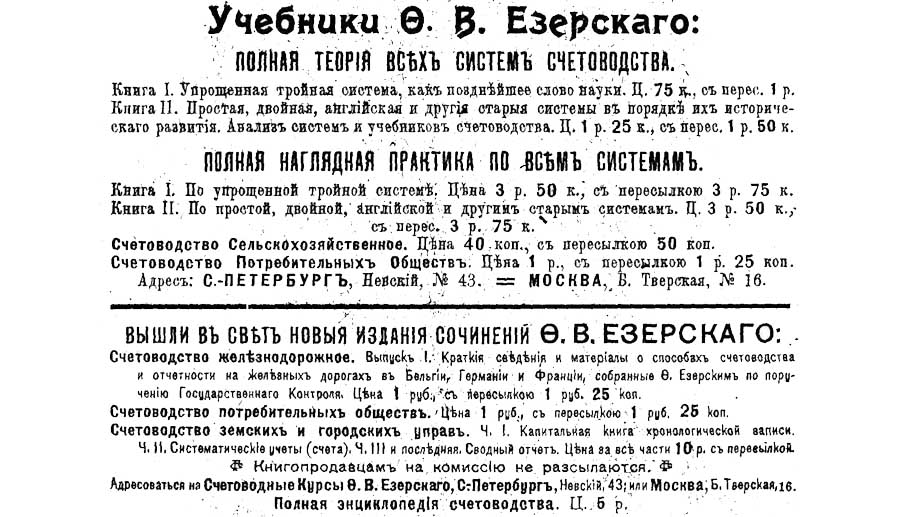

As you can see, accounting courses also published educational literature - for the most part their founder. It must be said that Fedor Venediktovich Yezersky had his own printing press and his own book-selling points, which partly explains the instructive fact that, until today, this author has the most extensive bibliography of all Russian accountants. What he just did not write - mainly in accounting, of course. The recipe for preparing books on triple bookkeeping was uncomplicated and not much different from modern ones: its own Russian triple system was taken as a basis, some industry specific taste was added to it, as well as statistical and advertising data on the author's achievements. And - the new textbook was published, there was no need to turn to anyone for help: the author was a typographer,and a bookseller in one person.

Advertising books F.V. Yezersky:

Product title pages:

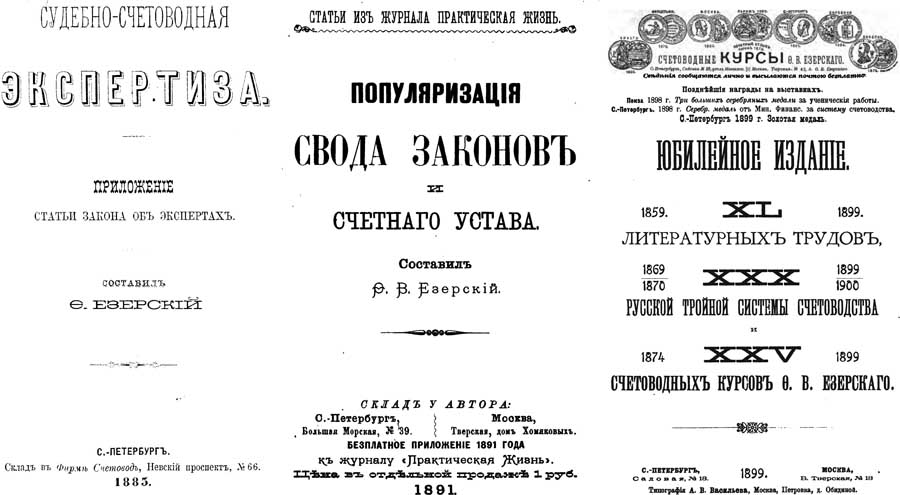

By the way, Yezersky received letters of commendation not only for the accounting system, but also for his literary activity:

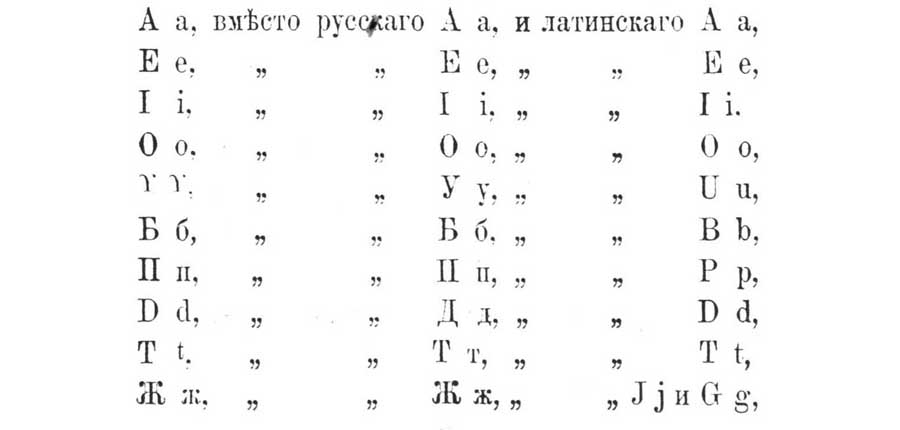

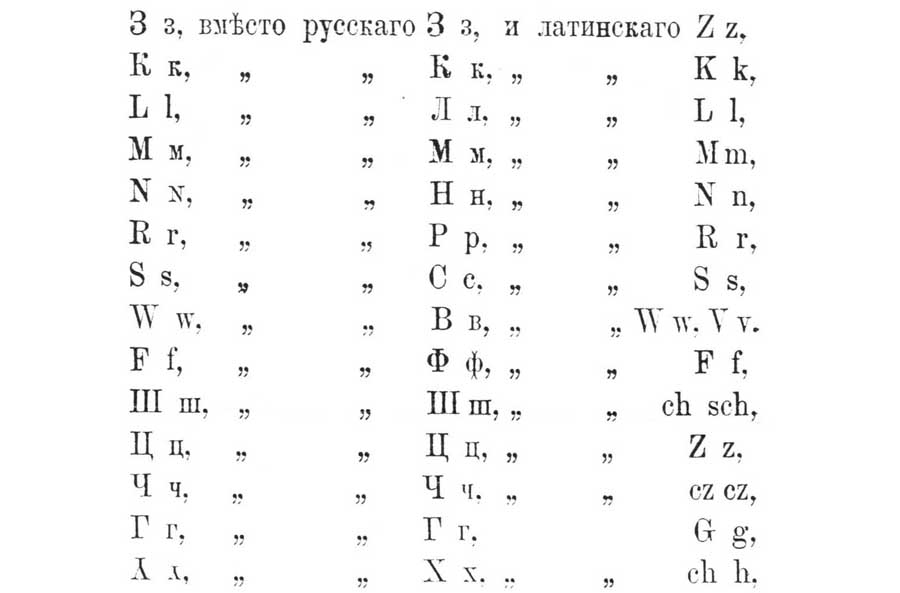

7. International Alphabet

Fyodor Venediktovich was a versatile person: in addition to accounting, he was interested in other areas, for example, in 1885, he invented an international alphabet . In my opinion, rubbish is rare, but I do not understand anything in linguistics - let the habravchane make their own opinion how difficult it is to invent such a multilingual alphabet.

8. Edition of magazines

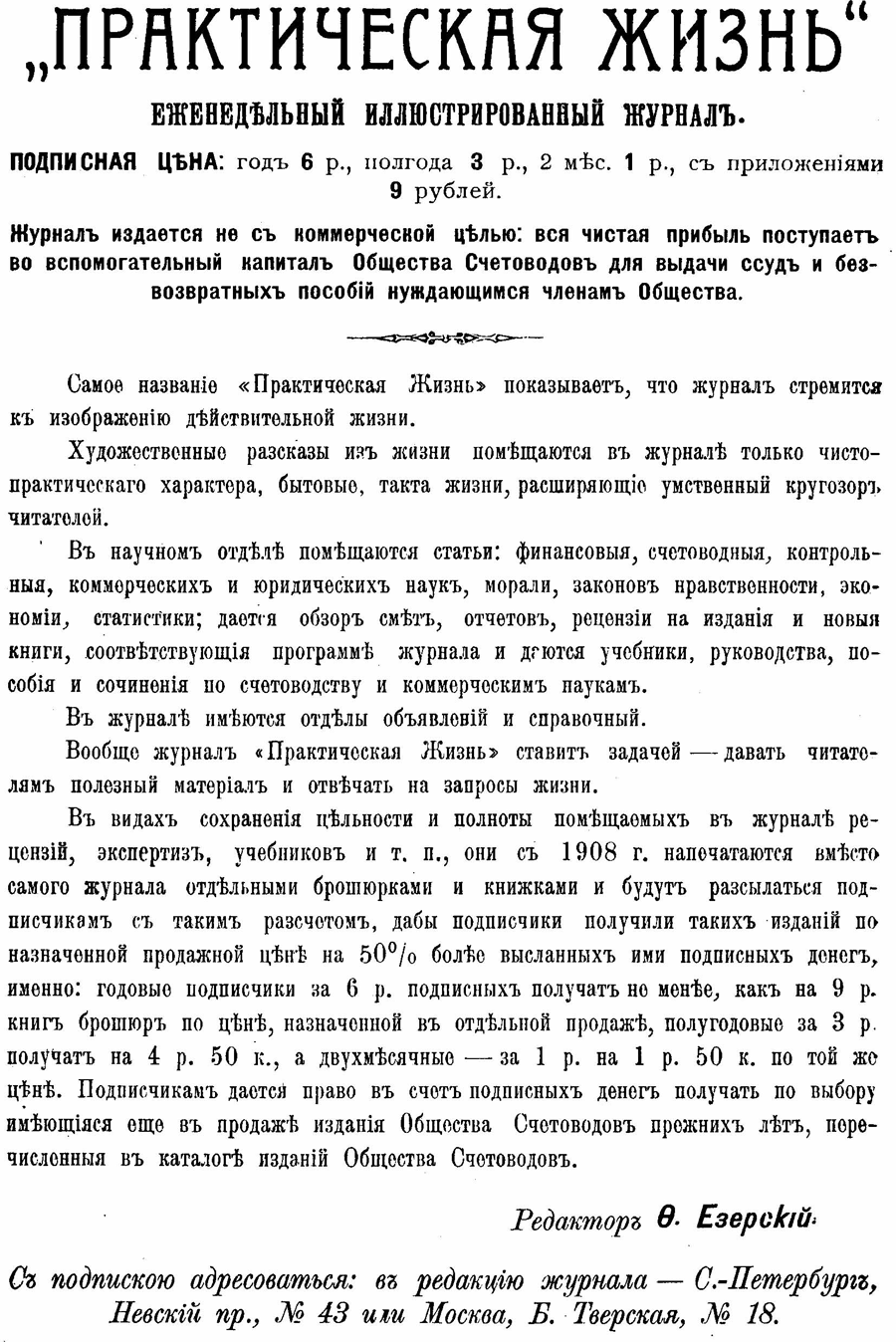

In 1889 (again not the first in Russia, it should be noted) Yezersky founded the illustrated accounting journal Practical Life . In addition to accounting, absolutely non-accounting materials were published in Practical Life - the calculation was made to attract a non-accounting public.

Advertising for Practical Life magazine:

Picture from the cover of Practical Life magazine:

With a short break (in 1911), the magazine, which soon became weekly, existed until 1914. The editor was, of course, Fedor Venediktovich, who later connected to the editorial activities of his son Nikolai Fedorovich .

9. First All-Russian Congress of Accountants

However, I rode forward a little, I propose to restore the chronology.

In December 1891 - January 1882, a book-keeping exhibition was arranged at its Moscow courses of Yezersky. At the exhibition (and not vice versa!) The First All-Russian Congress of Accountants was heldfor which a special permit was obtained from the Ministry of the Interior. Here Fyodor Venediktovich managed to outstrip his compatriots, although later they tried to challenge his merit by finding the first accounting congress organized by other people and held later. There was some reason for this, since there is no doubt: not the most prominent colleagues, but the protege of the organizer or his students took part in the Yezerskiy congress. For reference, I will inform you that by that time the international congresses of accountants were held at least three times: in 1879 in Rome, in 1884 in Florence and in 1890 in Bologna.

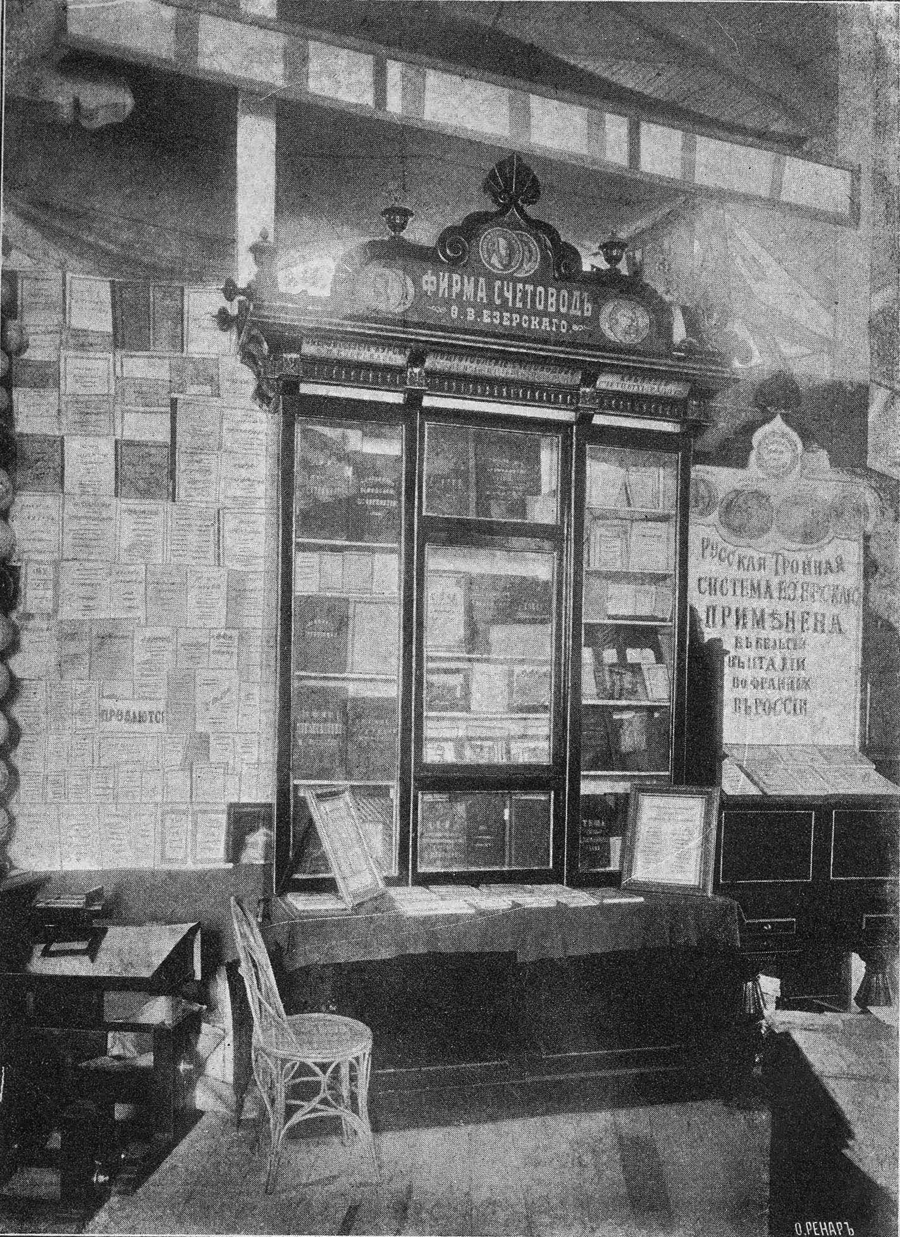

Stand firm F.V. Yezersky at the exhibition in 1882:

Pay attention to the company name: "Accountant". This is natural, since Fyodor Venediktovich thought to be the accountants of specialists who adhered to his triple system, while the others were for him despicable accountants.

10. Society of accountants

It is not surprising that in 1892 F.V. Yezersky founded a society with the same name.

On February 17, 1892, a meeting of the founders of the Company of Accountants was held , at which they adopted the draft Charter.

Four months later, on June 26, 1892, the Charter was approved. In particular, it stated:

Ҥ 1. The Accountants Society is established in Moscow to bring together people interested in accounting, economic and financial issues and to assist in the comprehensive development of various issues in accounting, statistics, economy and finance, and also for the delivery of funds to the members of the Society of Accountants and their families for a pleasant passing of time in their environment and for obtaining seats.

§ 2. To achieve its goal, the Society of Accountants:

a) opens its own special, permanent, or rents temporary premises;

b) arranges conversations and public readings on issues related to the field of economic and financial;

c) arranges a special library and reading room, where members of the Society could receive the necessary certificates and materials,

d) instructs its members to collect economic and statistical information;

e) publishes various special essays, prints reports on meetings in time-based publications and separate prints, and also publishes reports on its activities in its own body. ”

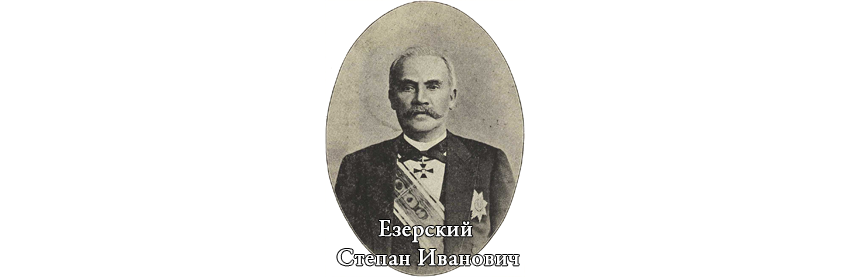

The Council was called upon to direct the activities of the company, which, in addition to the indispensable founder, included S.D. Yezersky, A.F. Lomovissky, I.M. Nesterov, N.N. Artakov . Later Artakova replacedV.M. Gribovsky . PP was elected Secretary of the Council . Kurzin Here they are, to a single, in the order named:

Noticed how another Yezersky flashed on the horizon? Not the last, by the way. Stepan Ivanovich Yezersky and his spouse Adel Karlovna Yezerskaya were also directly involved in the companies and organizations of Fedor Venediktovich . So all the relatives were employed.

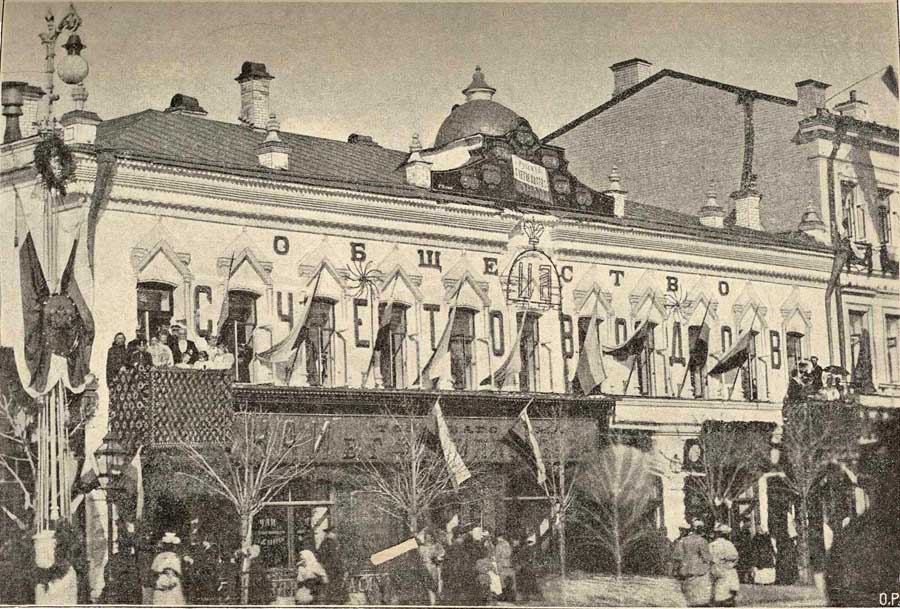

On October 2, 1892, the grand opening of the Company of Accountants took place:

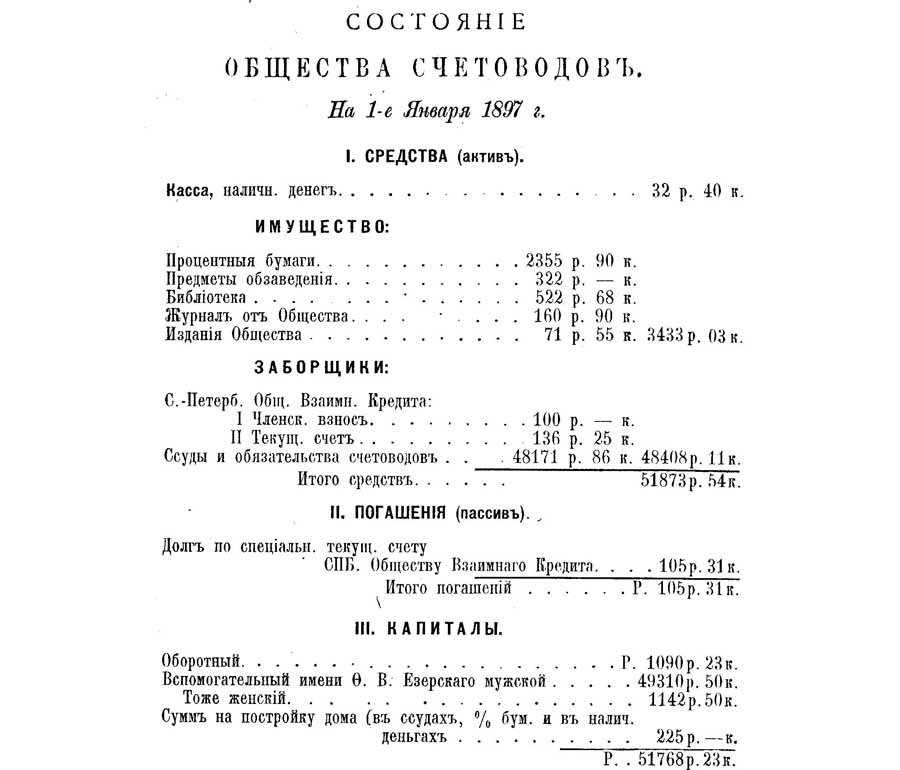

Report of the Company of Accountants as of January 1, 1897. A

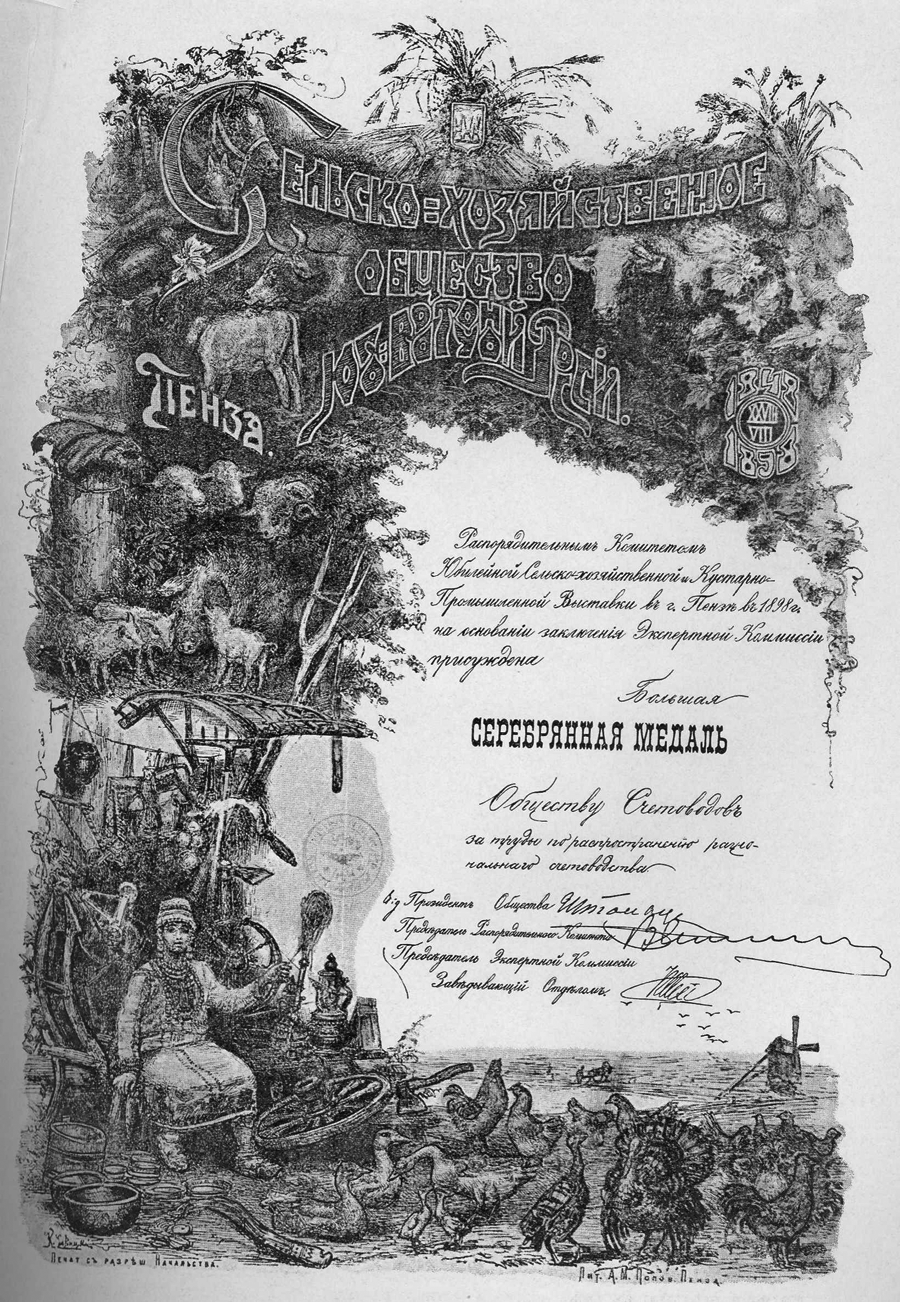

diploma obtained by the Company of Accountants in 1898 at an exhibition in Penza:

Advertising of the Company of Accountants and commemorative publication a decade later:

11. Other journals published by F.V. Yezersky

With the formation of the Society of Accountants, Practical Life magazine was transferred to its ownership. In 1896, instead of Practical Life, the Journal of the Society of Accountants began to be published , later both journals existed simultaneously. The editor of the Journal of the Society of Accountants was F.V. Yezersky, the publisher - the Society of Accountants itself.

As you can imagine, something in the publication of periodicals did not satisfy Fyodor Venediktovich, and in 1911 he founded the magazine "Accountant" .

The editor, along with the indispensable founder, was A.A. Shovsky .

In 1914, the magazine "Accountant" and "Practical Life" united.

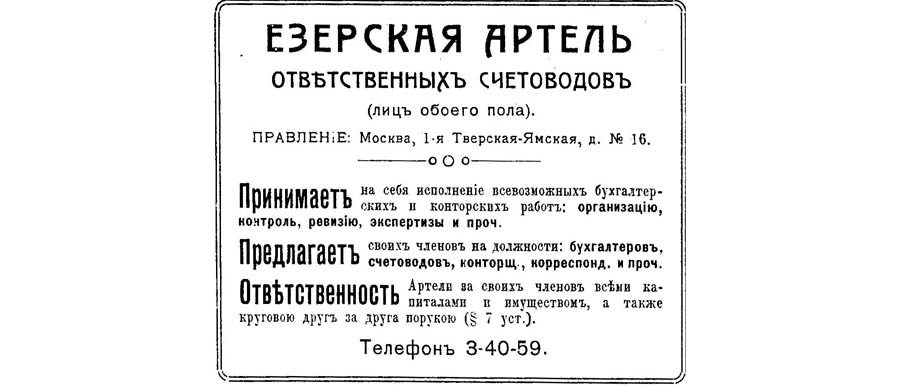

12. The Yezerskaya Artel of Responsible Accountants

Again, I inadvertently ran ahead - going back a couple of years to the past.

In 1912 the Yezerskaya artel of responsible accountants was created . The founders, in addition to Fedor Venediktovich himself, were his spouse AK Yezerskaya, mentioned above A.A. Shovsky and A.F. Lomovissky, as well as Ivan Khristoforovich Ozerov, is a famous economist, by the way.

The activities of the Ezerskoy Artel focused on the same things that other institutions F.V. Yezerskogo: advertising founder and the resulting commerce.

That's all, actually.

13. On the threshold of eternity

Fyodor Venediktovich Yezersky died on April 22, 1915. After his death, triple bookkeeping suddenly passed away, and it turned out that there was no one to support and feed him, despite the efforts made during his lifetime.

Widow Adel Karlovna tried to continue the work of her late husband and in 1916 she began to publish the bookkeeper and cooperative business, which was conceived by Fedor Venediktovich , but in vain. The times were not the same, bad times, muddy, fratricidal.

The son of the deceased, Nikolai Fyodorovich, participated in the white movement, emigrated to Yugoslavia, then to France, eventually accepted the priesthood and didn’t manifest himself in the public arena, at least in accounting.

After the October Revolution, triple bookkeeping was forgotten: resolutions were passed that ordered the bookkeeping to be carried out according to a double system. After this, the number of supporters of triple bookkeeping F.V. Yezerskogo rapidly decreased and soon decreased to zero. Somewhere in the beginning of 1920, the All-Russian Society of Accountants named after F.V. Yezersky , but, apart from the only mention in the press, the organization didn’t leave any traces, even if it existed in reality, and is not a typo.

So the human effort goes to naught. There was a man - and there is none, and what else to say about Fedor Venediktovich?

He was, as far as can be judged, a man with a difficult character: he did not tolerate the slightest disagreement, as a result of which not equal partners gathered around him, but at best students or even silent hangers-on. THEIR. Ozerov, co-founder of the Ezerskoy Artel, was not noticed in support of the triple bookkeeping. From the inner circle of F.V. Yezersky after the Revolution lit two:

- A.F. Lomovissky produced textbooks on commercial computing, which he did in the pre-revolutionary years,

- previously not mentioned P.N. Khudyakov, the younger co-author of Fyodor Venediktovich on one of the textbooks, taught accounting disciplines at the military academy for many years and died already in 1967.

I would like to know what these people thought about triple bookkeeping in the Soviet years!

But back to Fedor Venediktovich.

Besides the fact that he had an authoritarian character, Yezersky was an ardent nationalist: in 1900 he even published a brochure entitled “The Russification of the Accounting Language” , in which he proposed to abandon foreign accounting terms.

The saddest thing is that Fedor Venediktovich Yezersky was not the most talented of his contemporaries: there were more gifted ones. However, the images of most of them did not survive, biographical data are scarce, while the author of the triple bookkeeping knows where much, he took care of. The poet Mayakovsky was right, stating: say only good things about yourself, your comrades will tell about you bad things.

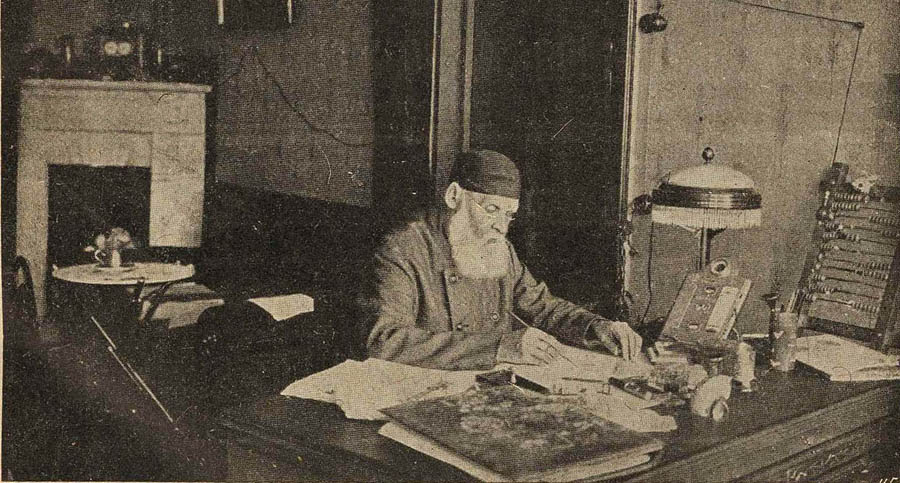

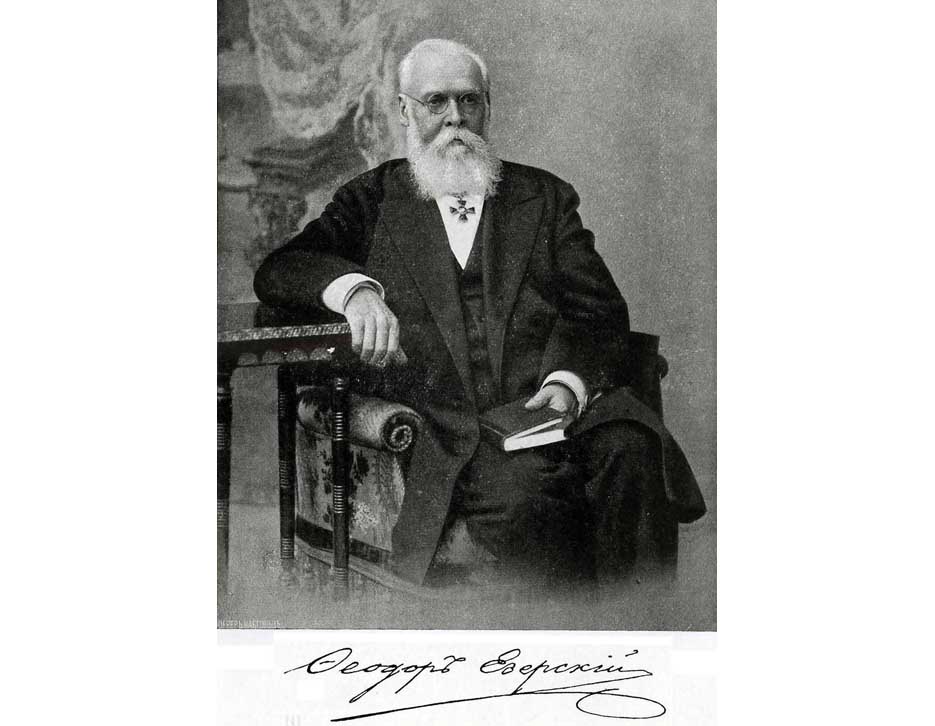

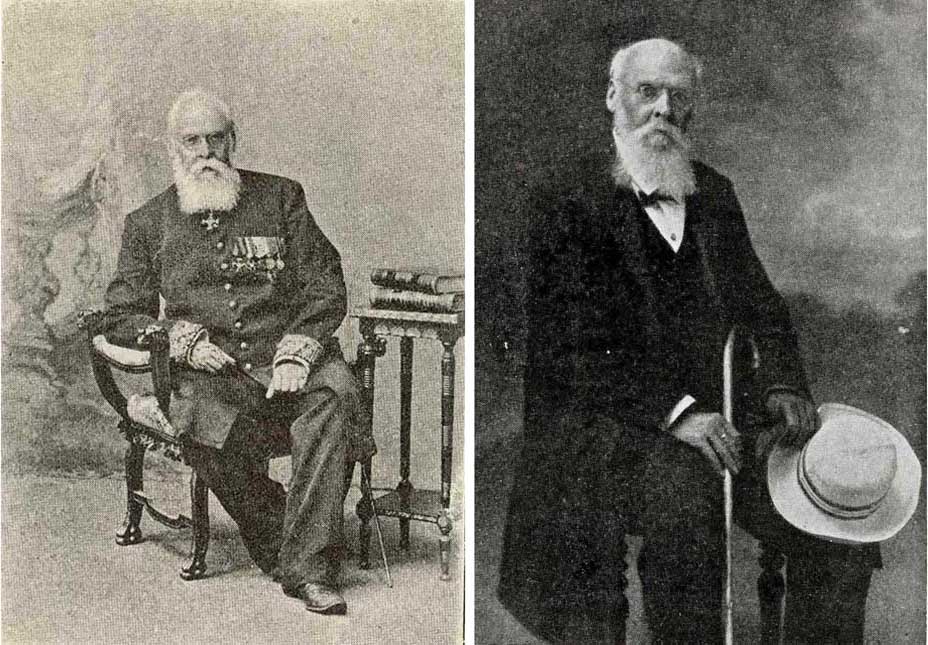

Other photos from the later ones (however, they are all late - in the youth of Fedor Venediktovich with cameras it was problematic):

This time is really all. Thank you for your interest in the story.

Source: https://habr.com/ru/post/192894/

All Articles