“Others” column: about budget smartphones and local brands

Older acquaintances often call me (young people usually know what they want) and ask to advise a mobile phone. Like, I'm standing in a store, is there such and that to choose? So a couple of years ago they usually said something like this: there is a good Nokia and there is a good Samsung, tell me what to prefer. In 2013, the situation changed radically. Already several times they called and asked for help in choosing between local Russian brands. At the same time, the models of “first-tier” manufacturers were not considered in principle. Just in case, I asked my comrades - what about Samsung, but what about Sony? They answered something like this: “And we have a budget of 200 bucks. The hand does not rise to pay for the 200-dollar Sony, when there is a model of the X brand next to it, and its screen is one and a half times larger. ”

Indeed, I don’t recall adequate options from A-brands with a value of 6-7-8 thousand rubles. World-class companies focus on more expensive models - and invest in them, as they say, their whole soul. Naturally, some people with enviable persistence plan to climb into the "initial" segment, but these attempts can not be called any successful. For example, just yesterday I dealt with the model LG Optimus L5 II Dual for 7 thousand rubles. (I will write a review a little later, you only need to beg for use for at least a week.) The device itself is not bad - though you don’t remember that the analogues from B-brands cost almost two times less. And in terms of iron, they also win: so, in this very L5 II Dual there is a rather old “stone” MediaTek MT6575, and in some Highscreen Spark for 3,500 (also “two-part”, also 4-inch and also 5 megapixel) - dual-core Qualcomm.

LG Optimus L5 II Dual

')

Actually, the fact that LG EXTREMELY used the budget platform MediaTek in its low-cost model (it is 20 percent cheaper to buy counterparts from Qualcomm), says the following: the Korean company tried to reduce the price of its product in order to compete with small brands in markets like Russia . The attempt, however, is not counted: the price is still too high. (Although lower than that of the Optimus L5 Dual at one time - in the middle of the life cycle, it cost about 8.5 thousand.)

According to some reports, several other first-tier manufacturers will soon try to follow a similar path. For example, if you believe the rumors, Sony intends to give the development of low-cost models to the side (however, there is nothing new here - this was practiced by Sony Ericsson). In the meantime, the Japanese vendor is selling in China a Xperia C smartphone with two SIM cards and a MediaTek MT6589 chipset. There is no other way: in China, the situation with local brands is even “worse” than in Russia. If you don’t make an inexpensive product even cheaper, they will trample it.

Sony Xperia C

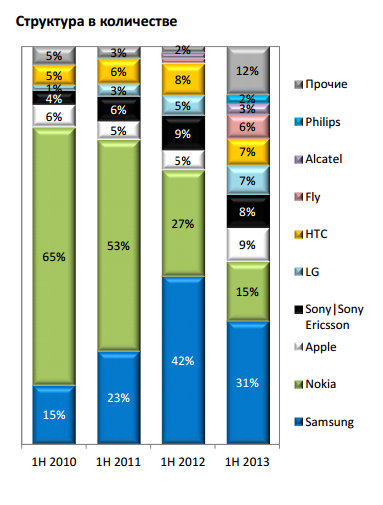

In Russia, the process of “trampling down” the market with domestic brands has also started. Just look at this chart, published by the Euroset analytical department:

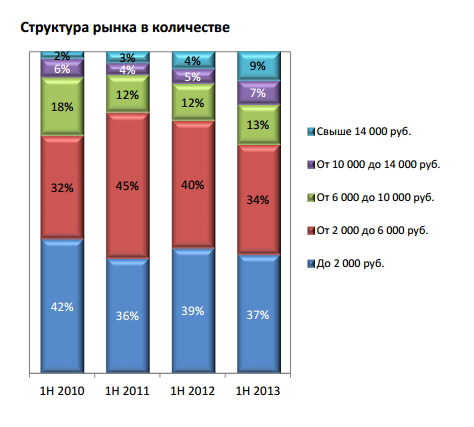

Who grew up in the first half of 2013 compared with the first half of 2012? First of all, the point “Others” is striking: these are the very local brands that increase supplies, reduce prices and thereby reduce the shares of first-tier brands. In particular, the shares of Samsung and Nokia have noticeably “lost”. Meanwhile, Fly, Alcatel and Philips — in terms of the technical level of the products and the approach to pricing, they practically do not differ from all the same local B-brands — they have noticeably grown. And it is precisely due to budget decisions costing up to 10 thousand rubles, as evidenced by the following Euroset schedule and data on sales of phones and smartphones in the first half of 2013. During this period, about 17.3 million cellular devices were sold in Russia, which is 7% less than in the first half of 2012.

Pay attention to the segments "from 2 to 6 thousand" and "from 6 to 10 thousand." The sales volumes in them have changed not too seriously (a drop from 40% to 34% in the “from 2 to 6 thousand” area is explained primarily by the extinction as a class of touch phones - NON-smartphones). And if earlier only A-brands ruled there, now they are being squeezed out by second-tier brands (12% vs. 2% - see the first diagram). "First tier" remains to be saved in the segments "from 10 to 14" and "from 14 and above", investing in advertising and marketing of the respective models. Actually, the major manufacturers are busy with this, due to which growth in the two indicated segments in the first half of 2013 was demonstrated.

However, let me assume that in some of the first half of 2014, the share of the total share of “Others” or “Others” will grow again, including due to the segment “from 10 to 14 thousand”. Because In-brands today, taking a strong position in the lower segments, are aimed specifically at him. Naturally, here they will have much more difficult: the buyer of a smartphone for 12-14 thousand is much more demanding than the buyer of a smartphone for 7 thousand. The first one would like to see the latest version of Android with the mandatory updates, a really high-quality camera, some soft chips and so on, and the second is ready to put up with some technical backwardness of the device due to its low price.

However, it’s the beginning: the V-brands offer in the “from 10 to 14 thousand” segment such chips that the first-tier manufacturers cannot provide for comparable money. So, in Highscreen Alpha R for 13 thousand screen is installed with a resolution of 1920 x 1080 pixels, that is, Full HD. And at the end of August Alcatel One Touch Idol X (and again a model from the B-brand) for 14 thousand will appear in Russia. According to the Alik's characteristics, the Alpha is somewhat weaker (there is no memory card slot, one 2,000 mAh battery versus two for 2,000 and 4,000, and so on), and yet A-brands are still powerless against such options. Yes, there is a very niche 5.5-inch "shovel» Lenovo IdeaPhone K900 with Intel Atom for 17 thousand (which, however, is already much more expensive), and prices for other devices with Full HD-displays start at 18-19 thousand . For the money you can buy Sony Xperia ZL, and, apparently, "gray".

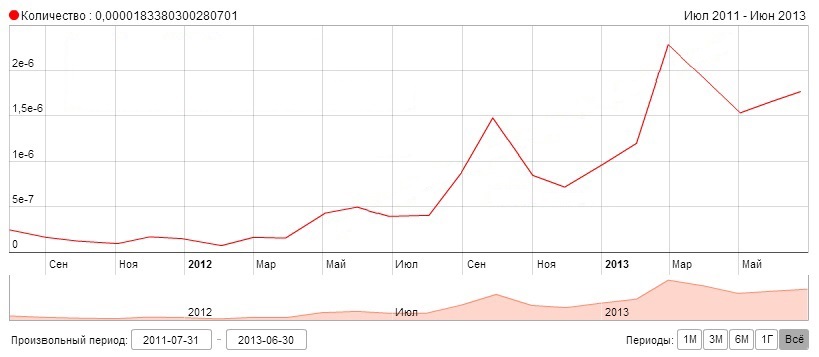

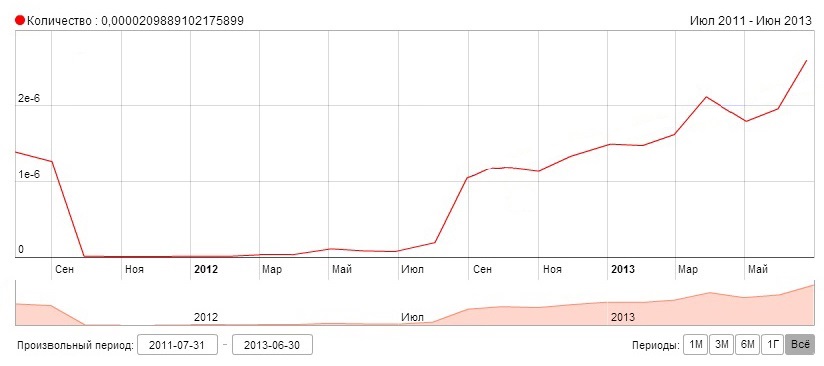

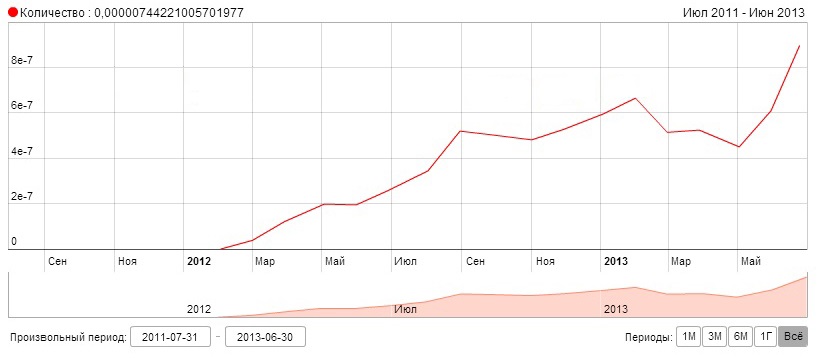

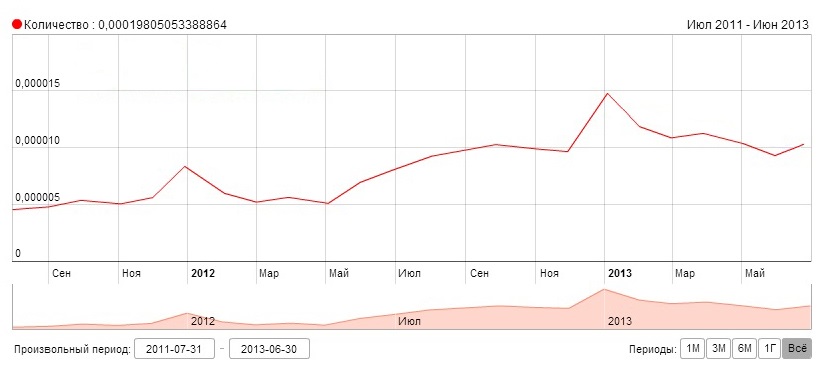

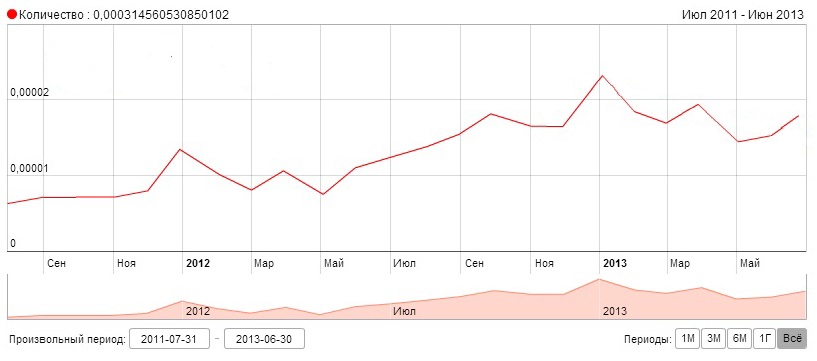

Fits perfectly into such a picture, and this is a small study conducted with the help of Yandex. It assesses the growth in the number of requests for the phrase “smartphones [substitute brand]”.

To begin with, we present charts for several second-tier brands.

Highscreen:

Explay:

teXet:

And now - a couple of brands first.

HTC:

Samsung:

Sony:

I don’t want to say at all that users show no interest in HTC, Samsung or Sony smartphones. Show up. I just want to note that this very interest is of a very calm nature - the number of requests is not explosively growing, on the contrary, in the case of HTC and Samsung, the graph is completely descending. Meanwhile, the growing interest in B-brand smartphones has been replaced with the naked eye.

It is clear that the "first echelon" is not so easy to surrender. It will be interesting to see what the respected grandees will undertake in the struggle for non-operator markets. That is, for those countries where successfully trade smartphones under their own brand, roughly speaking, anyone can - with some experience, connections in Asia and start-up capital. There are enough such comrades in Russia. Back in 2011, local brands involved in smartphones could be counted on the fingers of one hand. Today, a couple of dozen. And these same dozens gladly “bite” the Big Serious Manufacturers with the World Name.

Indeed, I don’t recall adequate options from A-brands with a value of 6-7-8 thousand rubles. World-class companies focus on more expensive models - and invest in them, as they say, their whole soul. Naturally, some people with enviable persistence plan to climb into the "initial" segment, but these attempts can not be called any successful. For example, just yesterday I dealt with the model LG Optimus L5 II Dual for 7 thousand rubles. (I will write a review a little later, you only need to beg for use for at least a week.) The device itself is not bad - though you don’t remember that the analogues from B-brands cost almost two times less. And in terms of iron, they also win: so, in this very L5 II Dual there is a rather old “stone” MediaTek MT6575, and in some Highscreen Spark for 3,500 (also “two-part”, also 4-inch and also 5 megapixel) - dual-core Qualcomm.

LG Optimus L5 II Dual

')

Actually, the fact that LG EXTREMELY used the budget platform MediaTek in its low-cost model (it is 20 percent cheaper to buy counterparts from Qualcomm), says the following: the Korean company tried to reduce the price of its product in order to compete with small brands in markets like Russia . The attempt, however, is not counted: the price is still too high. (Although lower than that of the Optimus L5 Dual at one time - in the middle of the life cycle, it cost about 8.5 thousand.)

According to some reports, several other first-tier manufacturers will soon try to follow a similar path. For example, if you believe the rumors, Sony intends to give the development of low-cost models to the side (however, there is nothing new here - this was practiced by Sony Ericsson). In the meantime, the Japanese vendor is selling in China a Xperia C smartphone with two SIM cards and a MediaTek MT6589 chipset. There is no other way: in China, the situation with local brands is even “worse” than in Russia. If you don’t make an inexpensive product even cheaper, they will trample it.

Sony Xperia C

In Russia, the process of “trampling down” the market with domestic brands has also started. Just look at this chart, published by the Euroset analytical department:

Who grew up in the first half of 2013 compared with the first half of 2012? First of all, the point “Others” is striking: these are the very local brands that increase supplies, reduce prices and thereby reduce the shares of first-tier brands. In particular, the shares of Samsung and Nokia have noticeably “lost”. Meanwhile, Fly, Alcatel and Philips — in terms of the technical level of the products and the approach to pricing, they practically do not differ from all the same local B-brands — they have noticeably grown. And it is precisely due to budget decisions costing up to 10 thousand rubles, as evidenced by the following Euroset schedule and data on sales of phones and smartphones in the first half of 2013. During this period, about 17.3 million cellular devices were sold in Russia, which is 7% less than in the first half of 2012.

Pay attention to the segments "from 2 to 6 thousand" and "from 6 to 10 thousand." The sales volumes in them have changed not too seriously (a drop from 40% to 34% in the “from 2 to 6 thousand” area is explained primarily by the extinction as a class of touch phones - NON-smartphones). And if earlier only A-brands ruled there, now they are being squeezed out by second-tier brands (12% vs. 2% - see the first diagram). "First tier" remains to be saved in the segments "from 10 to 14" and "from 14 and above", investing in advertising and marketing of the respective models. Actually, the major manufacturers are busy with this, due to which growth in the two indicated segments in the first half of 2013 was demonstrated.

However, let me assume that in some of the first half of 2014, the share of the total share of “Others” or “Others” will grow again, including due to the segment “from 10 to 14 thousand”. Because In-brands today, taking a strong position in the lower segments, are aimed specifically at him. Naturally, here they will have much more difficult: the buyer of a smartphone for 12-14 thousand is much more demanding than the buyer of a smartphone for 7 thousand. The first one would like to see the latest version of Android with the mandatory updates, a really high-quality camera, some soft chips and so on, and the second is ready to put up with some technical backwardness of the device due to its low price.

However, it’s the beginning: the V-brands offer in the “from 10 to 14 thousand” segment such chips that the first-tier manufacturers cannot provide for comparable money. So, in Highscreen Alpha R for 13 thousand screen is installed with a resolution of 1920 x 1080 pixels, that is, Full HD. And at the end of August Alcatel One Touch Idol X (and again a model from the B-brand) for 14 thousand will appear in Russia. According to the Alik's characteristics, the Alpha is somewhat weaker (there is no memory card slot, one 2,000 mAh battery versus two for 2,000 and 4,000, and so on), and yet A-brands are still powerless against such options. Yes, there is a very niche 5.5-inch "shovel» Lenovo IdeaPhone K900 with Intel Atom for 17 thousand (which, however, is already much more expensive), and prices for other devices with Full HD-displays start at 18-19 thousand . For the money you can buy Sony Xperia ZL, and, apparently, "gray".

Fits perfectly into such a picture, and this is a small study conducted with the help of Yandex. It assesses the growth in the number of requests for the phrase “smartphones [substitute brand]”.

To begin with, we present charts for several second-tier brands.

Highscreen:

Explay:

teXet:

And now - a couple of brands first.

HTC:

Samsung:

Sony:

I don’t want to say at all that users show no interest in HTC, Samsung or Sony smartphones. Show up. I just want to note that this very interest is of a very calm nature - the number of requests is not explosively growing, on the contrary, in the case of HTC and Samsung, the graph is completely descending. Meanwhile, the growing interest in B-brand smartphones has been replaced with the naked eye.

It is clear that the "first echelon" is not so easy to surrender. It will be interesting to see what the respected grandees will undertake in the struggle for non-operator markets. That is, for those countries where successfully trade smartphones under their own brand, roughly speaking, anyone can - with some experience, connections in Asia and start-up capital. There are enough such comrades in Russia. Back in 2011, local brands involved in smartphones could be counted on the fingers of one hand. Today, a couple of dozen. And these same dozens gladly “bite” the Big Serious Manufacturers with the World Name.

Source: https://habr.com/ru/post/190534/

All Articles