tma - total management accounting

In the near future, we expect new big changes. The technique reveals to us and promises us unprecedented changes, unheard of possibilities. But it is necessary that we should be ready for all these changes and opportunities.

In the near future, we expect new big changes. The technique reveals to us and promises us unprecedented changes, unheard of possibilities. But it is necessary that we should be ready for all these changes and opportunities.Ya. V. Sokolov (Doctor of Economics, Professor, Member of the Methodological Council for Accounting at the Ministry of Finance of Russia)

With these words of the great historian of accounting, I want to begin a series of articles where I will tell you how you can break reinforced concrete stereotypes of financiers and accountants with the help of zeroes and ones. Accountants and financiers are not yet ready for these changes and opportunities, but IT specialists who are fully aware of these opportunities should help them. To do this, they need to look at the grounds on which these stereotypes are built.

The first article is devoted to tma (general management accounting) - a concept designed to lead all these changes in the future.

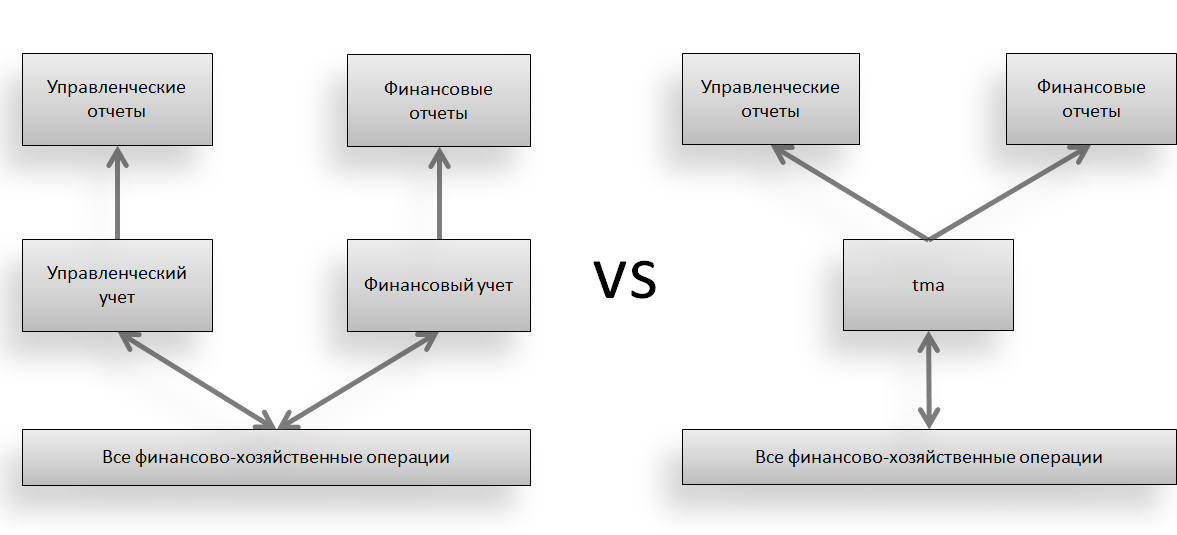

IT technologies allowed us to combine two different functional areas into account in a single system:

- Financial Accounting.

- Management Accounting.

The result is a system of general management accounting or tma-system.

')

What is financial accounting?

The result of financial accounting are financial statements (a triad of financial statements ). Consumers of financial accounting are usually external parties, including business owners. The task of financial accounting is to present a general picture of the state of the business and the results of its activities so that external financial stakeholders can make their decisions:

- To sell or not to sell a business.

- Invest in business extra money.

- To give or not credit money or commodity.

- Is it worth working for this company?

- ....

Usually, an enterprise works for a period (year, half year, quarter, month), and then it reports in the form of a triad of financial reports to its stakeholders .

Using these financial statements, you can control the business in the overall picture of its success, but you cannot get detailed information.

Note that throughout the civilized world financial statements are one for various direct and indirect stakeholders. In our country, financial reports submitted to the state are not suitable, for example, for business, and this is a fact. Therefore, accounting for the creation of financial (accounting) reports for the state, we will call, as we are accustomed to, namely, accounting.

In our country, the culture of financial accounting is just emerging. Many are engaged in the transformation of data and the formation of financial statements on the principles of IFRS or US GAAP. In any case, financial accounting is a complex and expensive pleasure that rather large companies with good incomes can afford.

In the generally accepted basis of the procedure of financial accounting is bookkeeping (maintenance of accounting records) on the principle of double entry. Therefore, financial accounting is carried out in terms of a single accounting (reference) currency. That is, all accounting units are converted to the accounting currency before they are recorded in the accounting accounts. Thus, financial statements are considered only in terms of accounting currency. To transfer them to another currency, you must overwrite all accounts in the expression of another currency.

The accounting procedure moved almost unchanged from the paper to the computer, but without a system data record this would no longer be financial accounting.

What is management accounting

By definition, this is accounting for management purposes. Well, or more formally, to support management decision making.

Since financial accounting provides us with the resulting data only once in the reporting period, it is not suitable for business management purposes.

Thus, the main property of management accounting is everyday life, which financial accounting cannot boast of.

The result of management accounting are various management reports. Their form is not regulated anywhere outside the business. Management accounting is the internal kitchen of an enterprise, for internal parties (management at various levels).

The management report can not show the overall picture of business success, but the details - as much as necessary.

Unlike financial accounting, in management there is no rigid procedure for recording data and tight binding to the accounting currency. We can have management reports of different forms and in kind, units of accounting (in the number of units of accounting).

Professor V.P. Savchuk. Compares the one-stop start of financial and management accounting with an iceberg, where the visible small part is financial accounting, and the large invisible part under water is management accounting. So all our companies are icebergs that float in various oceans of industries :).

Professor V.P. Savchuk. Compares the one-stop start of financial and management accounting with an iceberg, where the visible small part is financial accounting, and the large invisible part under water is management accounting. So all our companies are icebergs that float in various oceans of industries :).For clarity, we will summarize all of the above in a simple table (with red points highlighted):

| Management Accounting | Financial Accounting | General Management Accounting tma |

| Data is presented at any time. | Data is presented only at the end of the reporting period. | Data can be submitted at any time. |

| Cannot summarize holistic state and results. | Summarizes the holistic state and results | Summarizes the holistic state and results |

| Gives detailed data | Can not give detailed data | Gives detailed data |

| Unsystematic data recording | System data record | System data record |

| Conducted in any expression of accounting units | In terms of currency only | Conducted in any expression of accounting units |

| Reports can be presented in any expression of currency or unit of account. | Reports can only be presented in terms of a single accounting currency. | Reports can be presented in any expression of currency or unit of account. |

| For internal use | For external financial stakeholders | For external and internal use |

The table clearly shows that in order to achieve certain tasks one had to sacrifice something else. Thus, two functional accounting systems emerged: financial and management accounting. At the same time, the shortcomings of financial accounting are critical and unacceptable for management purposes and vice versa, the deficiencies of management accounting do not allow using its results for the purposes of general control and analysis of business from above.

According to the table, you can easily characterize tma - general management accounting.

Accounting, the results of which can be suitable for both external and internal consumers, since it is possible both to monitor and analyze the overall picture of the success of the enterprise, and to analyze the data in detail. In both cases - at any time. Data is systematically and balanced recorded in in-kind units of accounting. Both management and financial reports can be presented in any expression of currency or accounting units.

The root of the solution to the problem of combining the functions of management and financial accounting lies in the system of recording data in the database of accounting records. Unfortunately, I can not yet reveal the essence of the method of recording data, in which such a union was possible, since it is a commercial secret. But in the near future, this information will be in the public domain.

Thanks to a new electronic form of bookkeeping and a new way of recording data into it, general management accounting is kept in physical terms of accounting units, and financial reports can be presented in any currency. The concept of accounting currency is simply absent.

For now, one can simply accept that such a method exists and is implemented in applied solutions that can be used in practice, and talk about what opportunities are revealed to us thanks to this.

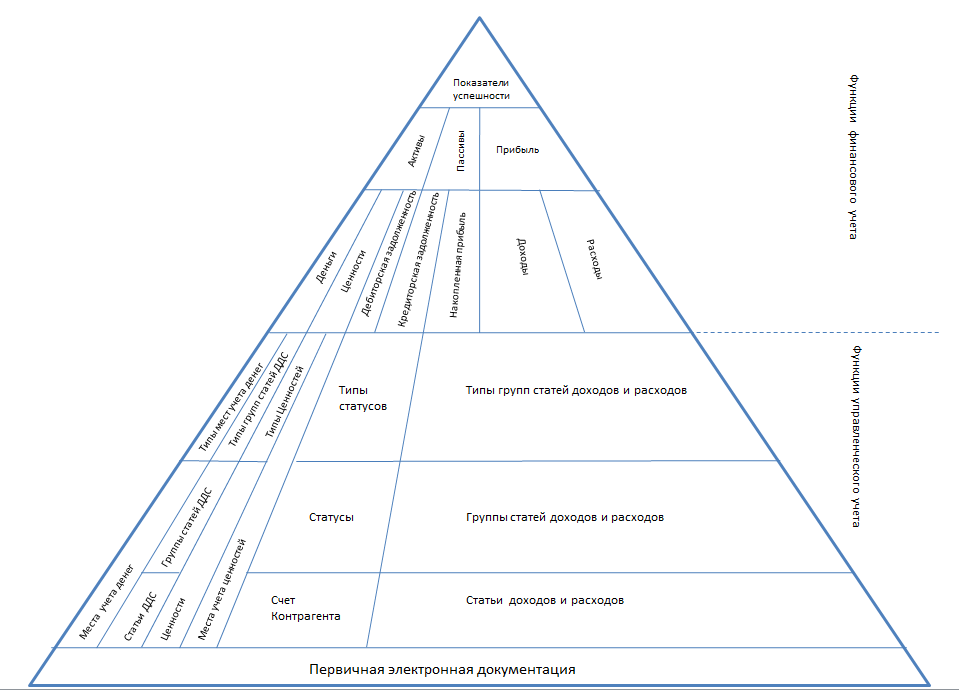

Data on financial and economic operations from the primary electronic documents form at a single level of management and financial accounting a single holistic system.

Such a system can be represented in the form of a pyramid, where all electronic source documents are at the base, and to the top all these data are summarized in the indicators of the success of the enterprise. In various horizontal sections, data form information on the level of managerial or financial accounting.

As an example of such a pyramid:

The integrity and interconnection of all information, general and detailed, is well visualized. Due to this relationship, any financial statement data can be decomposed (detailed) to any level of management accounting and compared with each other. In this case, the overall picture of the success of the enterprise can be formed at any time.

In the next article I will explain how you can generate daily financial reports, ways to analyze them and automate the monitoring of key indicators of business success.

Source: https://habr.com/ru/post/134019/

All Articles