Experience of implementing 1C UAT at a distribution center

Foreword

Everything is mixed up in company X. The costs of the transportation department are growing and no one understands anything. The director does not understand what the funds are going to. The CEO does not understand why, instead of a new Toyota for his little son, he should buy caps on gazels for a million dollars apiece. The head of the transport said, “I understand you,” and went to buy the bushings of the half-springs. There comes a critical moment, the financial director throws the cap to the ground and says: “We need profitability!”. “Profitability! ..” - exhale at once those present and translate views on the head of the information department. “Arrange” - he says and buys a yellow box with 1: Motor Vehicle Management. A working group is being formed, implementation begins.

What we want to get in the end

The staff of accountants in the transport department carries fuel and spare parts. Drivers no longer fall on the bones for each liter of the burnout - the consumption is calculated exactly. Trip, travel, repair sheets are created on time and correctly. Automated salary calculation for drivers: all sorts of surcharges are taken into account, deductibles are deducted. Information exchange between the existing ICs is automated: the requirement-consignment notes are formed from the repair sheets in 1C Accounting and spare parts are accounted for exactly 10.5. Physical persons are unloaded from ZUP in due time. But the main thing - all analytics is done in a couple of clicks! The head of the transport department can report on every liter of diesel fuel, every battery, every ruble spent on repairs. He can get data on the status of any machine at any time. Thus, everyone is happy: transport records are easy to maintain, accounting does not interfere with the process and only controls the correctness of unloading, the financial department receives relevant data on profitability. This is a picture of an ideal accounting, which, with the right approach, can be realized on the basis of 1C UAT.

What we have now

The chief of the transport keeps records in pencil in a notebook, and the computer last turned on accidentally, having touched the heel. The dispatcher drives data on the flow of income to the Excel, where the estimated flow is calculated using very simple formulas (of course, the minimum of parameters is taken into account). At the end of the month, drivers fought for every liter of burned down, convincing the dispatcher that he was standing in a traffic jam in the Upper Matyuk and had to make a detour in the Lower Navels due to the repair of the road. No one knows the actual route and fuel consumption. To get the parts in the accounting department, the primary organization is transferred with notes, and the local girls drive in the nomenclature as they like, because they have a vague concept of what the rim pulley and brake disc differ from. Because of this, transport and accounting are often confused in the transmitted data. Payroll makes the script on VBA in the same Excel. Cars have their own names - Gazelle Shabby and Peterbilt Green, there is no fixed list of vehicles. At the end of the month, when documents come from the processing centers of fuel suppliers, the accountants in the transport department manually reconcile the totals, and in case of inconsistencies they mingle in the proceedings with the drivers.

How will we implement

As practice shows, it is extremely difficult to break the accounting methods proven over the years in a large enterprise (however wild they may be). Full-scale implementation is challenging for several reasons:

- increase in the need for labor resources. A large amount of information will need to be entered into the UAT for generating reports and gaining profitability;

- data must be entered by a state of qualified accountants. The approach “our girls will understand” is guaranteed to lead to failure;

- Integration with existing enterprise IP is required. In the case of a wholesale distribution base, this is integration with the warehouse accounting system (WMS) and accounting software;

- high coordination of work of all involved divisions at all stages is necessary. This is primarily a transport, information, accounting, warehouse;

- changes in business processes. If the company has a quality manager, then it interacts with the heads of departments and describes new regulations;

- technical complexity. In the information department, a person is needed who for several months will be engaged only in implementation. This is the development of information exchange tools at the preparatory stage and “file completion” until everything is settled down.

- minimal retraining costs;

- minimum maintenance costs;

- relatively short deadlines (1-2 months);

')

Key point: travel sheets and fuel consumption

To begin with, I took up the automation of metering fuel consumption - this was the main task of accountants in the transport department. The existing method implies a minimum of input information - run there, run back, load there, load back. With gazelles, in which the cargo was not taken into account, it was even simpler: only the distance traveled and the type of fuel - either LPG or gasoline. At a detailed examination of the Excel file, elementary formulas for calculating the flow rate were singled out; they used several coefficients adjusted by years of trial and error.

In UAT calculation of fuel consumption is implemented much more difficult. I will describe a few points with which questions arose.

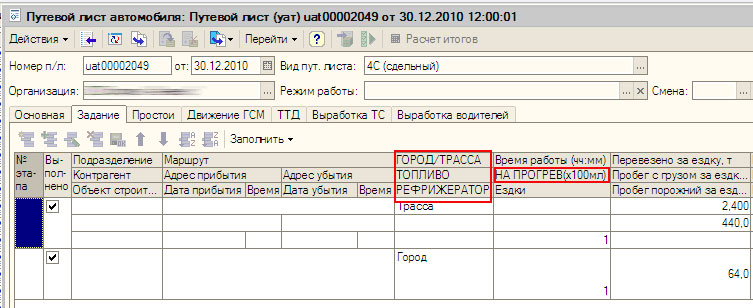

- itinerary. When forming a waybill, a route is formed on a “point-to-point” basis. This means that if the car travels from point A to point B through point C, then in the directory of routes there should be “A – C” and “C – B”. Moreover, if from A to C the car was traveling along the highway, and from C to B - within the city, then the flow will be different, and these two segments need to be driven in with different operating conditions (highway and city, respectively). Thus, for the formation of the job in the waybill, the accountant needs to know exactly the route and road conditions. And if truckers have five such points? Ten? Even after careful filling of the waybill, the difference between it and the calculation in the Excel reached tens of liters, and this despite the fact that all the factors were hammered in (corrections for road conditions, a refrigerator, trailer weight, equipment weight, warming up, season, etc.). It turns out an interesting relationship: the more the accountant enters information about the route, the more accurately the expense will be derived. It seems to me that the system is ideally suited to the ATP, where buses run strictly on schedule and on fixed routes. But automating the calculation on the flights of the delivery service, when the driver does not know how much he travels around the city, transporting the goods to points, and then may make a “detour” because of a traffic jam, turned out to be an unsolvable task. It was necessary to add a module to the configuration, which calculates the flow according to the formulas from Excel and add crutches to the form of the document;

- concept “model-TS”. The UAT has reference books “Models of TS” and “Fixed assets”. The operating system moves the “Initial information about the vehicle” information register, where all parameters of the vehicle, such as license number, tank volume, weight and other, are stored. There can be one model (GAZ-33023), and there can be ten cars of this model. Consumption rates - a property of the model. Consequently, all ten Gazelles of the same model will have uniform consumption rates, however, each of them can introduce a correction factor by which the model rates will be multiplied. But if one Gazelle, after the repair of gas equipment, has to drive only gasoline for a week, while the rest are driving gas, then it has to create a new model GAZ-33023-Gasoline. In addition, after a week you need to remember to refill it back. If you suddenly need to recast all the travel sheets created this week, then the standards, of course, will be taken already CURRENT and travel, which were introduced later, become incorrect! In short, I came to the conclusion that it is better for each machine to create its own model. Since the norms are tied to dates, they are flexibly configured and affect only one car (here, too, was not without revisions);

- fuel cost accounting. In UAT, there are two ways to introduce cost. The first: in the document “Refueling GSM” to which the waybill is attached. If there was a refueling in the flight, the accountant can immediately form a document in the corresponding tab of the waybill and indicate the cost based on the data from the checks. Second, the cost is downloaded at the end of the accounting period on the basis of documents received from the processing centers of the suppliers. Documents “Refueling GSM” and “Track List” are re-passed. In this embodiment, you need to specify 4 parameters: date, gas station, fuel type and cost. Thus, if the cost of fuel changed every 3 days (quite realistic situation), there are three types of fuel (LPG, gasoline, diesel fuel), 4 suppliers, then the accountant needs to do 10 * 3 * 4 = 120 loadings. Obviously, the first option is preferable. Entering the cost of fuel at each filling it is advisable to impose the duties of an accountant. It would not be superfluous to modify the Refueling Draft document so that it is not carried out without the cost of refilling;

- Reclassification / recalculation of waybills for an arbitrary period. If the accountant is mistaken, then all subsequent waybills turn out to be incorrect, since the final remainder of the previous one is the initial remainder of the next one. Write processing is easy, it will save a lot of time accountant.

What did you get

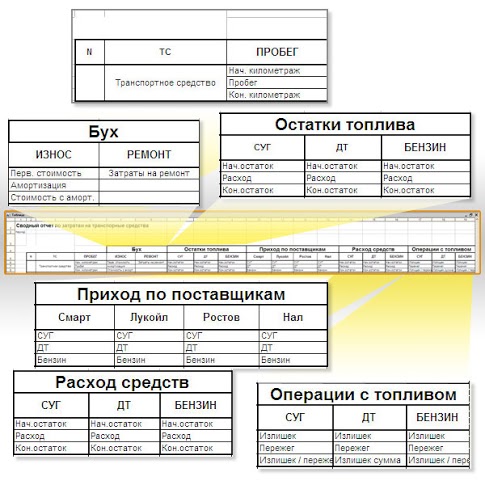

By automating the registration of waybills and entering into the configuration of the UAT additional requisites for communication with 1C Accounting for fixed assets, we get (for each of the vehicles):

- consumption for each type of fuel in the context of plastic cards, suppliers;

- the total cost of refueling for each type of fuel in the context of plastic cards, suppliers;

- total mileage;

- total transported cargo;

- initial cost, depreciation, depreciated value;

- total costs for parts.

To obtain an exhaustive picture of not enough costs for repairs, insurance, MOT, taxes and consumables. However, at the lowest cost, we obtained most of the indicators. This can be considered a success.

findings

- 1C UAT is a powerful system for managing profitability of transportation. This is a full-fledged accounting, only with a bias in the motor transport. Accordingly, the account in it must be maintained by a qualified staff of accountants;

- mastering the system during implementation is a notorious path to failure;

- The system is best suited to ATP with fixed routes and flight schedules. The system, unfortunately, is not suitable for those cases when the exact route of the flight is unknown. As an option, equip transport with “black boxes” and build information exchange with the UAT.

- the keys to success are the coordinated work of all the departments involved and a thorough study of the nuances of the fuel movement. The latter will relieve the frantic search of the missing thousands at gunpoint of the accountant.

Source: https://habr.com/ru/post/112294/

All Articles